Summary

In an uncertain market environment, fixed income is once again taking centre stage. With inflation expectations, policy paths and regional divergences shifting rapidly, investors are increasingly looking for solutions that can deliver both stability and income. In this context, an active fixed income approach can offer a compelling answer: one that combines discipline, flexibility and the ability to respond quickly to changing market conditions.

The European fixed income spectrum offers a broad range of opportunities. We take a tour of the European fixed income universe to see the different contributions to portfolio construction and the vital role of fixed income in strengthening European autonomy.

Structural changes in the Euro sovereign market

Anne Beaudu, Senior Portfolio Manager, Euro & Global Aggregate strategies

After many years of disinflation, zero to negative interest rates and quantitative easing (QE), bond markets have experienced dramatic shifts since the Covid pandemic. To face the post-Covid inflation surge, amplified by rising commodity prices following the Ukraine war, central banks were forced to rapidly tighten their monetary policies, just as fiscal policies were expanded dramatically to cushion any economy shock. This led to an abrupt rise in yields, with curves first flattening, and even inverting, before steepening again as central banks were able to normalize back down towards neutral as inflation slowly drifted down.

The steepening was amplified by a renewed market focus on fiscal policies and debt paths, as fiscal dominance became a theme and term premium normalized after years of compression due to QE policies.

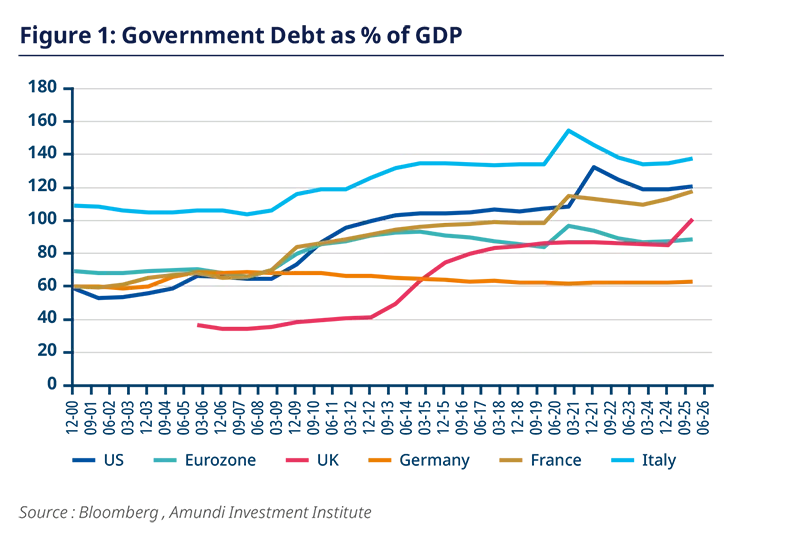

In the meantime, eurozone debt to GDP ratio went from 85% in 2019 to 97% in 2021, but drifted back down towards 88% in 2025 (Figure 1). It is now expected to rise again as German fiscal plan kicks in. Overall, the debt path of the whole Eurozone seems more reasonable than big economies like the US (126% in 2020), UK (112% in 2020) or Japan (215% in 2020). But great dispersion between countries remains and the margin of manoeuvre is very limited for some. Germany was able to announce a much needed fiscal plan in 2025, triggering a sharp move at the long end of the curve and a relative repricing of all other European assets vs Germany.

The eurozone faces many challenges in the years ahead: higher defence spending, much needed investments to increase productivity and tackle climate transition, and rising social spending in a deteriorating demographic context. The required investment will add more pressure on sovereign debt in a time of higher yields. As the geopolitical situation becomes ever more complex, with tangible negative impacts on growth prospects, pressure on fiscal deficits and the long end of the curve will remain elevated.

Pension reform is one issue that could have a big impact on the European bond market (see also “Europe's pension transition: from retirement challenge to capital market opportunity ”). Pay-as-you-go pension plans divert a large share of savings to finance current pension expenditures. This limits the build-up of assets invested in the real economy. Furthermore, existing funds have limited exposure to equities. These funds are governed by prudential rules and capital guarantees, forcing managers to adopt very conservative profiles. As a result, European households’ financial assets are not invested to their full efficiency, despite a very high saving rate.

For this reason, the Dutch pension fund reform, shifting from defined benefit to defined contribution was closely monitored as it entered its first major phase in January 2026. Dutch pension funds, which account for half of euro area pension fund assets, have primarily been invested in bonds, mainly domestic, German and French issues, and especially long dated maturities (>30 years). The shift is expected to trigger a radical change in their investment strategy with a structural reduction in the demand for long term government bonds, implying some 10Y-30Y steepening, especially on the swap curve. These changes had been largely anticipated and the cohort of pension funds due to transition in January 2026, finished 2025 with higher funding and hedging ratios, while some widening of swap spreads on 30Y maturities was visible during the second part of 2025. No big flows were observed in the first two months of 2026, while March was entirely dominated by the reaction to the Iran conflict.

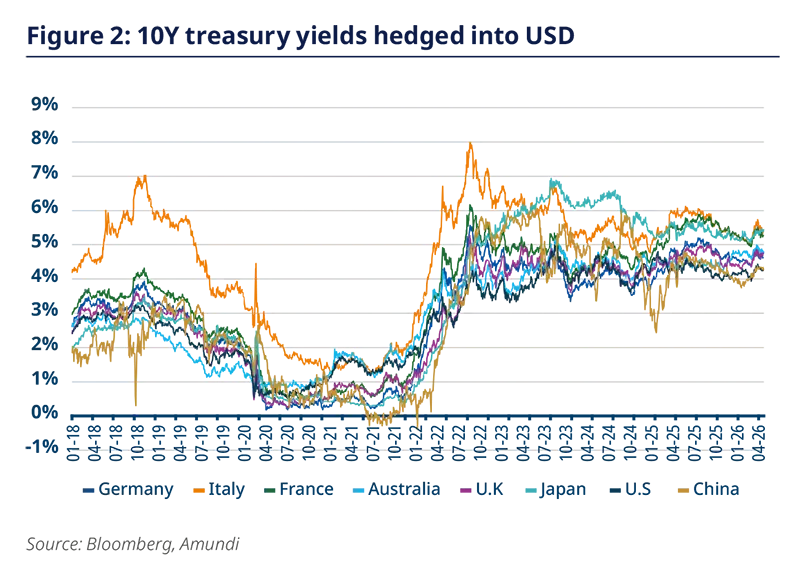

In this volatile and fast changing world, the European Bond market is the largest alternative to the US Treasury market, at a time when diversification trades out of USD are expected to continue. Once hedged into USD (Figure 2), German 10y yields are equivalent to US 10y yields1 and higher than Australia, Norway and some EM local 10y yields like China, Colombia or India. French 10y bonds yield 65 basis points above US Treasuries, above UK, Canada, South Korea or Indonesia, and Italy 10y yields are equivalent to Japanese 10 yields.

As inflation regimes, geopolitical events and more structural forces can trigger dramatic changes in curve shape and correlations, actively managing risk exposure is essential. Where duration risk is placed on the curve, or between countries, can significantly change the performance of a euro sovereign fund. But this environment also opens up many interesting opportunities for actively managed strategies.

Strong Supply & Demand in the Euro Credit market

Anne Nguyen, Senior Portfolio Manager, Euro Credit Investment Grade

Since the withdrawal of central banks from markets and the end of the QE era, interest rates have become more volatile and increasingly responsive to macroeconomic developments. As a result, fixed income markets have returned to more traditional dynamics. European companies have demonstrated their ability to adapt across different phases of the economic cycle. Corporate balance sheets are generally well-managed, with debt maturities well distributed over long horizons.

Within the euro credit index2, approximately one third of the market is composed of financial institutions. In a higher-rate environment, margins have improved, supporting stronger returns on equity. Moreover, bank balance sheets have been significantly strengthened over the past decade. From a relative fundamental perspective, while public debt sustainability remains a concern given rising fiscal pressure, corporates—particularly investment grade issuers—appear more disciplined and, in some cases, more robust than sovereigns. Rating trends reinforce this view, with upgrades outpacing downgrades since the Covid-19 pandemic.

This improvement in fundamentals, combined with higher yields, has led to the emergence of the target maturity fund market. These funds have gained rapid traction by offering attractive yields while maintaining diversified exposure to high-quality issuers. This search for yield has, in turn, contributed to the stabilization of credit spreads during periods of market volatility. Although spreads remain tight by historical standards—leading some investors to question the attractiveness of credit risk—the picture is more compelling when viewed through the lens of absolute yield. Current yield levels continue to provide adequate compensation for the underlying credit risk in European corporates.

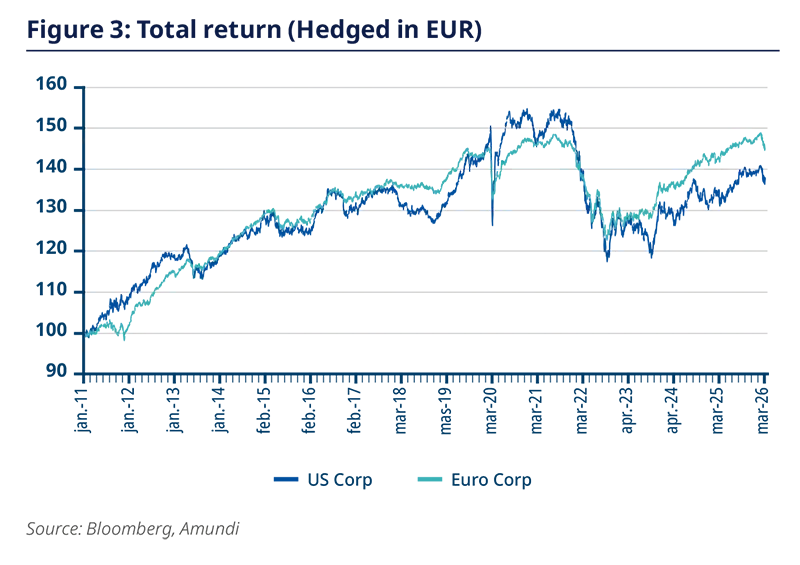

This emphasis on absolute yield is not new: it has long shaped investor behaviour in the US credit market, where investors have traditionally been driven more by yield than spread. In this respect, the EUR and USD investment-grade markets are broadly comparable, although they differ in structure. The EUR IG market offers attractive diversification benefits due to its distinct sector composition, shorter maturities, and valuation opportunities. After accounting for hedging costs, EUR IG and USD IG have delivered very similar performance over the past 15 years, with cumulative returns of around 80% since 2010 (Figure 3). This supports EUR IG as a credible diversification option for USD-centric fixed income portfolios.

Investors are increasingly turning back to active management to enhance returns in credit markets. In an environment characterised by heightened geopolitical uncertainty and rapidly evolving new flows, technical factors and investor positioning have become key drivers of valuation. Market demand is often neither fully rational nor immune to behavioural biases, creating inefficiencies. These dislocations present opportunities for long-term investors to generate alpha.

Furthermore, active management enables a more granular allocation across risk factors—such as duration, credit quality, and subordination—allowing investors to adjust exposures dynamically in response to changing market conditions. Even traditionally stable relationships, such as the correlation between interest rates and credit spreads, can shift over time, offering additional opportunities to express tactical views, hedge risk, or enhance returns.

Why Europe needs its high yield market more than ever

Thierry Lebaupain, Senior Portfolio Manager, Euro High Yield

The sovereignty debate in Europe tends to begin with defence budgets and end with public borrowing. That leaves out a critical link: corporate finance. Europe’s next phase will not be funded by sovereigns alone. The European Commission estimates additional investment needs at €750bn-€800bn a year by 2030, before any extra defence allowance. Yet market-based finance still accounts for only 13% of EU corporate funding, (vs ~30% in the US). This gap matters because the companies that keep the continent moving, connected and supplied do not all sit in the sovereign or investment-grade universe. Many sit below it, and always will. Telecom and fibre platforms, transport operators, industrial suppliers, healthcare services, environmental infrastructure and a large part of Europe’s mid-cap corporate base live naturally in leveraged structures. If Europe wants greater autonomy in infrastructure, industry and strategic capacity, it needs a deeper market for borrowers too.

The backdrop has become more compelling, or at least more pressing. Germany’s €500bn infrastructure fund marks a genuine fiscal turn after years of restraint. The ECB’s latest bank lending survey shows euro-area banks tightening credit standards for companies again. Dutch pension reform is also beginning to unsettle one of European fixed income’s old certainties: the structural bid for ultra-long bonds and swaps. None of this means money will simply wash into high yield bonds. It does mean, however, that Europe has better reasons than before to value deep domestic credit markets that can finance real companies and real assets, instead of heavy dependence on banks, foreign capital and the public sector. This is all the more true – and healthy – at a time when public debt burdens are already high, and sovereign stress is no longer a theoretical risk.

This is where European high yield comes in. The case for the asset class is not ideological; it is practical. A functioning high yield market gives access to capital to businesses that are too leveraged for investment grade but still central to the economy’s plumbing. Financing these companies allows essential improvement to freight corridors, telecom networks and sovereign communications capacity.

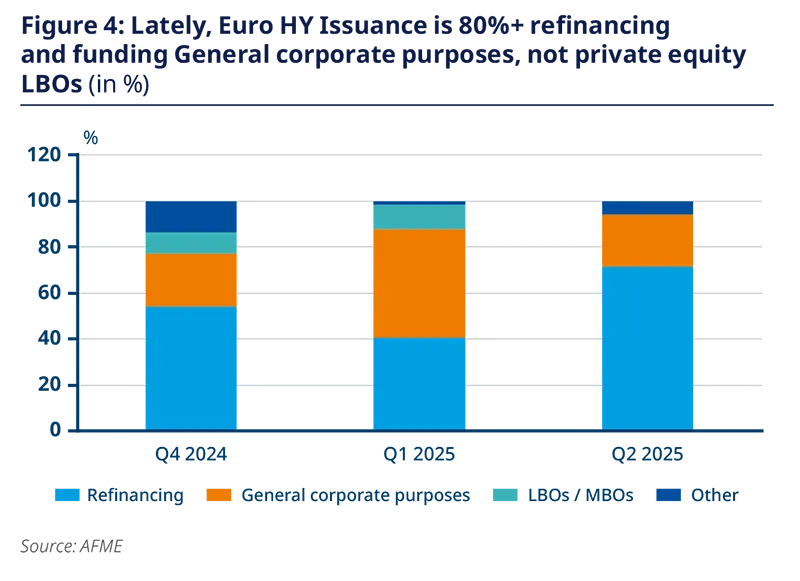

European high yield does not merely finance discretionary consumption or private-equity churn (Figure 4). It also finances the less glamorous but more consequential layers of the economy — suppliers, networks and service operators without which Europe’s ambitions in reindustrialization, resilience and infrastructure renewal remain largely rhetorical.

For pension investors, the appeal is straightforward. European high yield offers carry and, in the right hands, a compelling riskreward profile; but it is more than a riskier cousin of investment grade. It is one of the few listed, liquid and transparent fixed income markets that gives exposure to the productive middle of the European economy: companies below the blue-chip layer, but still important to how the continent builds, moves, powers and adapts. That matters in a Europe where savings exist but routing remains weak: around 70% of EU household savings, roughly €10tn, still sit in bank deposits.

This is also why active management is essential. The goal for European high yield is not to fund everything with a European flag attached; it is to fund viable, productive businesses while allotting capital away from weak structures, poor incentives and bad management. In high yield, deep analysis and selection are not optional. Documentation, refinancing risk, sponsor behaviour, asset quality and strategic relevance all matter. A strong active high yield strategy therefore does more than seek performance, it imposes discipline on capital allocation itself.

So the investor case is twofold. European high yield can offer attractive income and differentiated spread exposure, while also giving long-term capital access to a part of the European corporate landscape that other fixed income segments often miss. A Europe that is serious about financing its own priorities cannot rely only on states, banks and national champions. It also needs a robust market of active investors for the companies in between.

Boosting the European securitisation market- a path to growth

Hubert Vannier, Head of Securitized Assets

The USA is moving from the Pax Americana regime to America First foreign policy. The motive is economic dominance, with the USA choosing protectionism, racing to seize natural resources in Venezuela, and potentially in Iran and even Greenland. Amid these geopolitical uncertainties, European economic weaknesses come under the spotlight. Insufficient investments in technology, notably AI, in energy transition, or more recently, in defence are acute. Financing these investments is one of the main challenges of European policy makers. Regulation changes to support the financing of the economy are already happening. European institutions have adopted Solvency 2 improvements and are in a trilogue process for banking and securitisation regulations.

Securitizations externalizes risk from the asset seller’s balance sheet, potentially providing not only funding but capital relief as well, allowing the seller to lend again, in a virtuous cycle. Because they support financing autonomy and directly rely on European assets, securitizations are viewed as a key instrument for economical sovereignty.

Currently the largest securitizations, representing half of the market, are not sold to investors but retained by sellers and used as collateral with central banks. In our view, this means the market could double its size should economic conditions be met, i.e. should spreads tighten.

Securitization markets have followed the same pattern during the various crisis of the last 15 years, but the recent widening of securitization spreads has been much smaller than expected considering their pre-crisis absolute levels. This moderate widening can be explained by three main factors, which make the European securitisation market especially resilient:

– First the credit risk of collateral is limited, and the structures have been designed to absorb such shocks. ABS and RMBS rely on loans to households. They are not directly affected by sovereign, financial or corporate risks but are more sensitive to unemployment. CLOs are more sensitive, especially high yield tranches, but benefit from reinforced structures. High yield mezzanine tranches spreads have significantly widened but there is no downgrade trend or default.

– Securitization spreads benefit from a widening investor base as regulation changes allow insurance companies and banks to access the asset class.

– Finally, the nature of market participants is key: weak hands no longer invest in securitizations since the global financial crisis and there are no forced sales of securitizations.

European securitizations spreads react moderately to market shocks, and the recent regulation changes are expected to provide long-term support. This rare asymmetry, with a reduced sensitivity to crises and the benefit of spread tightening in times of normalization should attract investors interest. Other assets with higher beta may provide higher returns, should a favourable scenario occur, but such investments incur significantly higher geopolitical or macro risk, particularly as a stagflation scenario becomes more probable. Securitizations, as floating rate notes are not exposed to interest rate volatility. They provide investors with moderate credit exposure, which has a low correlation with other fixed income assets and benefit from higher spreads.

Blended Finance & Credit Continuum: A Structuring Solution for European Strategic Autonomy

Adnane Lekhel, Head of Institutional Structuring

Beyond the individual merit of each fixed income segment discussed in this article, the most compelling opportunity for pension funds committed to European Strategic Autonomy may lie in a cross-spectrum, structurally engineered approach that deliberately mobilises the full credit continuum, from sovereign and supranational paper through investment-grade corporate credit, high yield, and structured finance, within a single, coherently managed framework. The rationale is not diversification for its own sake, but rather the recognition that European strategic assets do not map neatly onto a single rating bucket or instrument type: a critical infrastructure project may carry quasi-sovereign characteristics in its senior tranche while its subordinated layers exhibit high-yield risk profiles; a defence supply chain SME aggregation vehicle may be most efficiently accessed through ABS mechanics; a transitioning industrial champion requires the flexibility of a covenant-rich high-yield structure with embedded sustainability step-ups. A fund architecture spanning the full credit spectrum, with active allocation across sovereign bonds, investment-grade corporate credit, high yield, and securitization, is therefore not a compromise between asset classes but the structurally appropriate response to the heterogeneity of the underlying strategic investment universe. Crucially, this framework allows the portfolio manager to position capital dynamically along the green credit continuum, from fully taxonomy-aligned senior instruments to transitioning assets carrying binding KPIs, ensuring that ESG integrity is maintained without artificially restricting the investable universe to only the greenest quartile of European strategic needs.

The blended finance3 dimension adds a further layer of precision to this architecture. By incorporating catalytic capital (i.e. public and/or philanthropy first-loss layer), the structure can present pension fund investors with a senior fixed income exposure that is credit and yield-enhanced, investment-grade rated, and aligned with Solvency II capital efficiency requirements and IORP II, while still financing assets that would not otherwise reach institutional capital markets unaided. This is structuring as a policy instrument: the role of the portfolio manager and structurer here is not simply to select securities but to design the risk transfer architecture that makes European strategic priorities financeable at scale. For a pension fund already considering allocations across high yield, ABS, sovereign bonds, and euro credit as discrete building blocks, the integrated blended finance solution offers something qualitatively different, not a fifth bucket, but a unifying investment framework that deploys all four instruments with strategic intentionality, concessional risk mitigation, and a measurable contribution to European autonomy embedded in its mandate from inception.

Conclusion

Today’s fixed income environment rewards selectivity, discipline and flexibility. With yields back at more compelling levels and market conditions becoming increasingly differentiated, investors have a wider set of tools than ever to build portfolios that combine income generation with risk management.

In a world where uncertainty is likely to persist, fixed income remains a powerful allocation for investors seeking both resilience and performance. A high-quality, actively managed approach can help navigate volatility, adapt to shifting inflation and policy dynamics, and capture opportunities created by regional and idiosyncratic divergences.

In this new backdrop, fixed income is not just about preserving capital — it is about using active management to turn dispersion and volatility into a source of opportunity for Europe.

1. As of 03/04/2026

2. Benchmark : Bloomberg Euro Aggregate Corporate (E)

3. https://www.amundi.com/institutional/article/framework-structuring-blen…

https://www.amundi.com/institutional/article/scaling-blended-finance-cr…

https://research-center.amundi.com/article/blended-finance-scaling-capi…

Authors