Summary

Europe’s pension systems are undergoing a structural change. Demographic ageing, tighter public finances and the evolution of retirement provision are reshaping the way pensions are financed and how savings are allocated. What is emerging is not only a pension challenge, but also a significant opportunity: as Europe adapts its retirement systems, it can mobilise more long-term capital to support investment, productivity and competitiveness.

For pension funds and institutional investors, this transition matters on several levels. It affects the sustainability of retirement systems, the adequacy of future retirement income and, increasingly, the structure of European capital markets themselves.

Setting the scene: Europe’s retirement challenge

Three structural forces are driving the change.

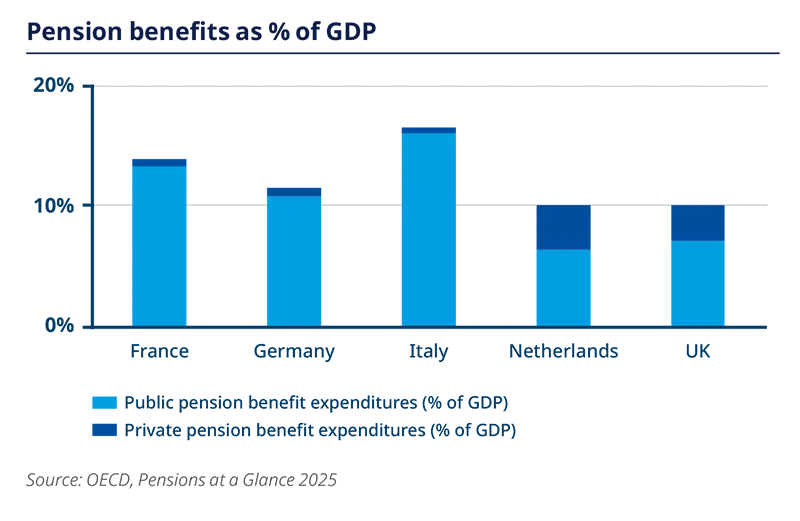

First, demographics. Europe is ageing, and the ratio of workers to retirees is declining in many countries. Lower birth rates and longer life expectancy mean more people are drawing retirement income for longer, while fewer active workers are contributing to the system. In several large European countries, pension expenditure already represents a double-digit share of GDP and is expected to rise further (Figure 1). OECD projections suggest that combined public spending on pensions, health and long-term care could increase by around five percentage points of GDP between 2021 and 2060 in median terms, with meaningful variation across countries.

Second, fiscal constraints. Public debt remains elevated across much of Europe, and higher interest rates have made that debt more expensive to service. This reduces governments’ ability to absorb demographic pressure through higher transfers or more generous public pensions.

Third, the changing structure of retirement provision. Traditional defined benefit (DB) arrangements continue to play an important role in many markets, while defined contribution (DC) schemes and individual savings are taking on greater importance in others. At the same time, retirement systems are increasingly expected not only to accumulate assets, but also to provide reliable income throughout retirement. This shifts attention toward decumulation, longevity protection and income generation.

Taken together, these forces are encouraging a gradual move toward more funded retirement provision and a stronger role for long-term capital.

Europe’s broader macro context

The pension issue cannot be separated from Europe’s wider macroeconomic backdrop. Higher debt burdens and higher yields reduce fiscal flexibility precisely then ageing societies require continued spending on health, pensions, defence and social protection.

At the same time, Europe faces a clear need for stronger productivity and capital formation. This makes the way savings are organised increasingly important. Pensions are not only a social policy mechanism; they are also one of the main channels through which long-term savings can be channelled into the economy and markets.

Productivity, investment and the Draghi report

The Draghi report4 has helped sharpen the debate by highlighting Europe’s productivity challenge and the scale of investment required to address it. Europe continues to require substantial investment in infrastructure, digitalisation, energy transition and industrial renewal. Yet the euro area’s gross investment rate remains around 2% of GDP, well below the roughly 3.5% observed in the United States. Productivity growth has also lagged: between Q4 2019 and Q2 2024, labour productivity per hour worked rose by only 0.9% in the euro area, compared with 6.7% in the US5.

In that context, the structure of pension systems matters: if too many savings are absorbed by low-risk or immediately consumptive channels, less capital is available for innovation oriented investment. The Draghi report estimates that Europe needs around €800 billion of additional annual investment, or roughly 4.5% of GDP, to close the gap and support the twin transition to a digital and decarbonised economy. Given the intensifying geopolitical instability, more recent estimates have increased this to €1.2 trillion6.

For pension funds, this is a relevant backdrop. Europe’s investment requirements are large and long-term, while pension liabilities are also long-term. That natural match is one reason pension capital is likely to become more important in Europe’s financing model.

Common denominators of pension reform

In this context, pension reform is crucial in addressing Europe’s fiscal and productivity-related challenges. Although execution remains national, several common themes are emerging.

Broader participation. Policies such as auto-enrolment are powerful because they make saving for retirement the default option. Experience in the UK, the US and Australia shows that automatic participation can materially expand coverage and assets under management. In Europe, the Irish and Italian push towards auto-enrolment further embodies this trend.

A gradual evolution in retirement provision. Across markets, there is a broad trend toward greater reliance on funded arrangements, while preserving the important role that existing defined benefit schemes continue to play. We see this clearly in the pension reforms currently taking place in the Netherlands, shifting from DB to funded arrangement in the pillar 2 system. In many cases, the question is less about replacing one model with another than about building systems that can better balance collective promises, individual savings and long-term sustainability.

Greater scale and consolidation. Larger pension pools can invest more efficiently, access private markets more easily and build stronger governance and risk-management frameworks.

A stronger focus on decumulation. As pension systems mature, the question becomes not only how to save, but how to convert savings into durable income in retirement. This increases demand for annuities, drawdown solutions, longevity-aware products and income-oriented portfolios.

These are not identical reforms, but they point in the same direction: pension systems are being redesigned to be more resilient, more strongly funded and better adapted to longer lifespans.

What an increase in pension assets means for European capital markets

As pension reforms increase the overall pool of retirement assets, the implications for capital markets become clearer. A larger funded pension base should support more persistent flows of long-term capital into retirement vehicles. Automatic enrolment and broader participation typically generate stable inflows, which are well-suited to long-horizon investment strategies.

It should also contribute to deeper capital markets and financialisation of the economy. For example, a stark contrast exists when comparing Europe to the US. Where the capitalization of EU companies represented 65% of GDP in the EU, this represents 177% of GDP in the US. A larger, domestic institutional investor base broadens the demand for market assets and improves the capacity of European markets to finance growth. Over time, this can support liquidity and capital formation.

Just as importantly, more pension assets should increase demand for long-duration and income-generating assets. Pension funds are natural holders of equities, infrastructure, private credit, mortgages and selected real assets, particularly where these assets can deliver stable cash flows and inflation sensitivity.

For pension funds, this has two implications. First, the opportunity set may broaden over time. Second, the role of pension capital in market development may become more visible, especially where domestic savings are increasingly channelled into long-term investment vehicles.

Specific reforms and their impact on asset allocation

Some reforms are designed not only to increase the size of pension assets, but also to change how those assets are invested.

One example is the move toward generational or age-based investment structures, which shift younger savers toward higher risk assets and reduce risk gradually as retirement approaches. Over time, this can materially influence aggregate demand for equities and other risk premia.

Another example is the transition toward collective DC models or more flexible DC frameworks, which may increase the use of credit, mortgages and income assets while reducing the emphasis on very long-dated hedging instruments.

The important point is that pension reform changes not only the quantity of capital, but also its composition and deployment.

Key opportunities for Europe

Europe’s pension transition can support a more sustainable retirement framework and a more dynamic investment environment at the same time. If pension reform succeeds, it can help Europe improve retirement adequacy, strengthen fiscal sustainability and deepen capital markets.

For pension funds, the direction of travel is clear. Europe’s retirement systems are moving toward a more funded and more market based model, even if reform remains uneven across countries. This transition is likely to be gradual, but durable, and it will increasingly shape the way long-term savings are organized and invested. At Amundi, we see this as a central strategic theme: better pension design can improve retirement outcomes and reinforce Europe’s capital markets at the same time.

4. The future of European competitiveness: Report by Mario Draghi, November 2024 https://commission.europa.eu/topics/competitiveness/draghi-report_en

5. Amundi, December 2025

6. European Commission, July 2025

Authors