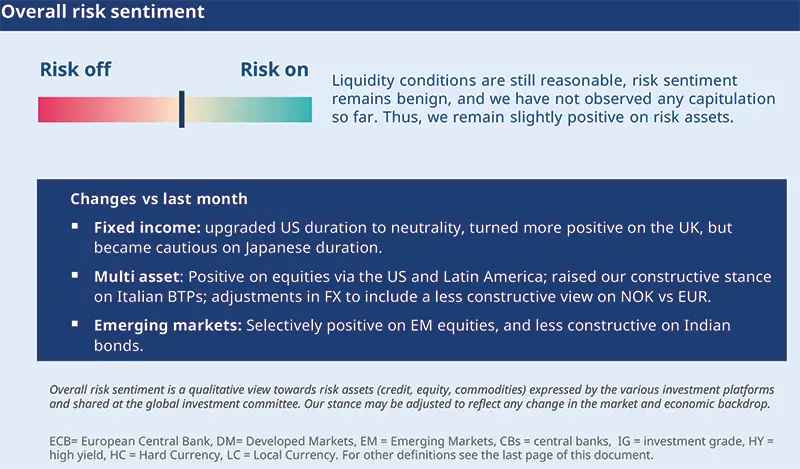

Summary

Shifting near-term narratives

Over the past few weeks, markets have been driven by higher inflation expectations, shifting central bank outlooks and contrasting news flow, all within a matter of days. This resulted in upward pressure on rates and downward pressure on risk assets in the initial part of the conflict. Most equities, including those in the US, Europe and emerging markets, have now returned close to their pre-war levels.

Efforts at ending the war and a fragile ceasefire have supported risk assets, but gains have been repeatedly tempered by a lack of resolution to the conflict and by the prospect of rates staying higher for longer. Market moves may be summarised by how the narrative has shifted between ceasefire or no ceasefire, risk-on or risk-off, and inflation and growth concerns. Looking ahead, we think:

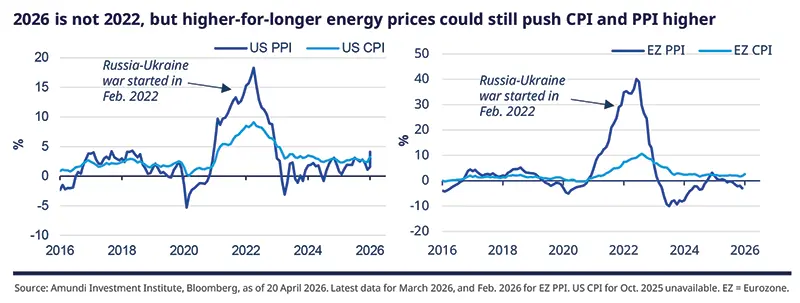

The main risk is the pass-through of headline inflation into core. Economies already experiencing high inflation may see convergence to target interrupted, while economies already at target face a non-negligible risk of expectations becoming de-anchored.

The growth outlook is weaker (not recessionary), depending on the persistence and propagation of this shock to the economy, and the length of time energy prices remain high. The positive momentum expected in early 2026 has given way to more subdued growth, due to the squeeze on real incomes and falling business confidence.

The developed market fiscal outlook was already strained before this crisis, and as a result we do not expect fiscal support to be broad-based in most parts of the world, including the US, Eurozone (EZ) and UK. It would be targeted, with selective relief for households and strategic sectors. Even in emerging markets (EM), responses will be country-specific.

Monica DEFEND

Central banks are vigilant, credible and flexible: anchored in inflation, alert to shocks and determined neither to overreact nor to fall behind.

The sequencing we had in mind with respect to economic growth, energy, transport, shipping, insurance and investor/consumer confidence has been confirmed.

Usually, the hit to economic growth comes with a lag, driven by weaker real income, margin pressures, softer demand and reduced policy flexibility. Secondly, we are seeing more visible trends in the form of regional asymmetry across Europe, the US and emerging markets. Third, central banks have behaved as expected so far, and they will be cautious, reactive and not pre-emptive.

With respect to the above, what has changed over the past month?

While our base case of slow economic growth has not changed, the probability associated to it has decreased, as we now see higher downside risks. In March, our framework was still one of targeted macro adjustments including energy shock, limited change to economic growth and cautious policy response. We’d like to reiterate that the persistence of the energy shock will matter more than the initial shock itself.

We now think of this event not as a one-off shock or a black swan event, but as an ongoing, longer reality that could eventually turn out to be a macro-financial shock. In March, the main focus was Hormuz, oil transit and the immediate consequences of disruption. Today, the interpretation is broader and may be longer-lasting.

Policy asymmetry has become more apparent. Last month, our view of central bank policy was that central bankers would remain cautious before hiking and might ignore a temporary inflation spike. Now we think, central banks would maintain “disciplined optionality”: protecting credibility, keeping inflation expectations anchored, watching second-round effects closely (very important!), and retaining enough flexibility to respond to shocks without tightening mechanically into fragility. This explains why, for now, we keep the Fed and ECB on hold and have postponed cuts to 2027.

What factors are we closely monitoring for us to change our views?

A longer period of disruption in the supply of oil, gas and other commodities from the Gulf would lead to second-round effects in the economy.

This means a pass-through of the crisis to energy, transport and other parts of the economy will affect prices in general. But if a pass-through to consumer prices is not possible, then corporate margins will be affected, implying a change in our views. Europe, in particular, is vulnerable to this shock.

Any hawkish shift in central banks’ response will be extremely important. If the Fed or ECB shows renewed hawkish tendencies, our call on duration, particularly for the front end, would change.

Revisions in earnings per share (EPS), as a consequence of a more persistent crisis.

Liquidity and credit transmission are supportive for risk assets at present. Equity volatility is low, and we do not see outflows in fixed income credit; technicals are also reasonable. Any change here would affect our views.

We believe this is an environment where portfolio construction matters more than directional convictions, underscoring the importance of selectivity.

This is a time to lean on long-term convictions and, if risk assets offer an opportunity, explore areas where earnings and fundamentals are robust, while maintaining safeguards.

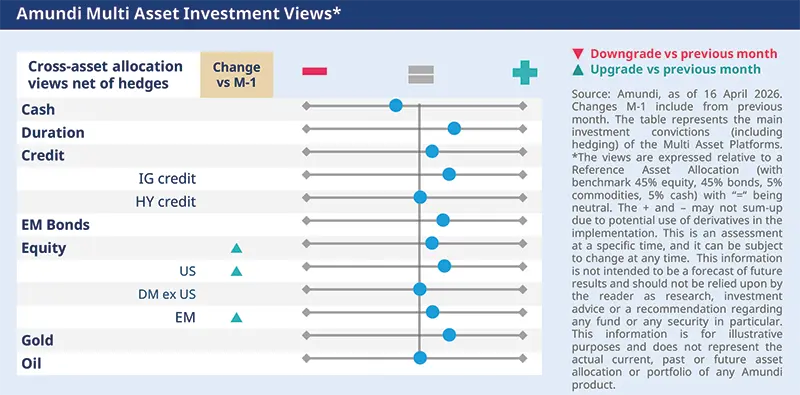

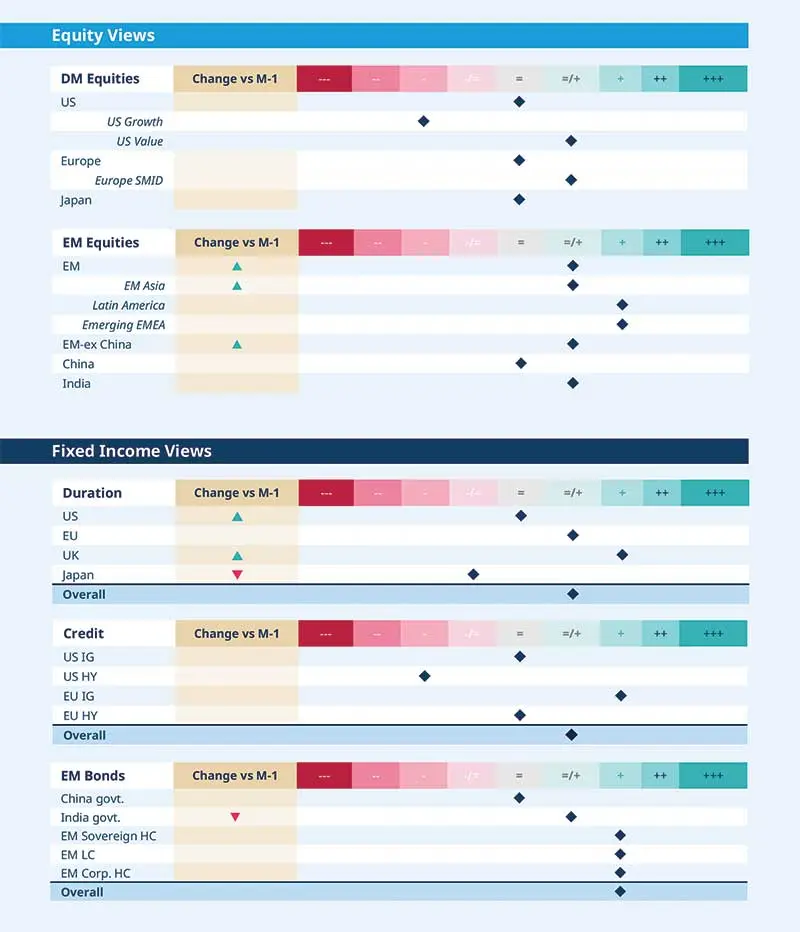

In fixed income, we are not calling for a directional bet on duration but rather for a focus on different yield curves and relative value. The front end of the curve remains sensitive to hawkish repricing, while weaker economic growth should, over time, limit the long end. This calls for a more nuanced investment approach. On duration, we upgraded the UK and are now neutral on the US. We are also selectively exploring corporate credit, and EM debt on which we remain positive, although we’ve tactically downgraded Indian bonds.

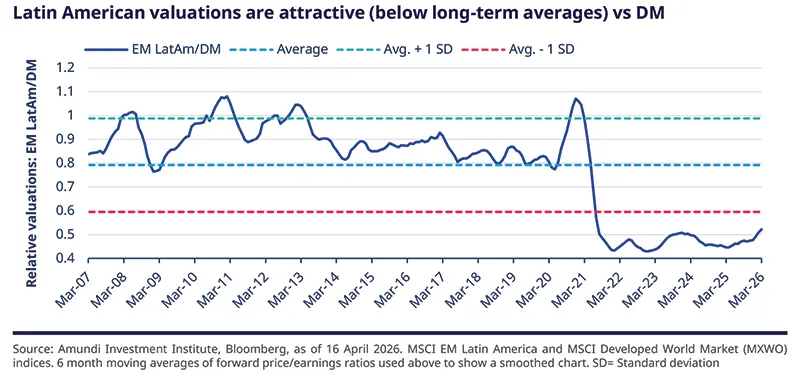

In equities, the recovery seen in April is indicative of markets’ view on a quick solution to the Middle East crisis. While the US is structurally the strongest region in equities, it’s also the most concentrated, and in some cases, is showing high valuations. Hence, we look for value in regions such as Europe, Japan and emerging markets like Latin America. Even though Europe may be less compelling as a pure beta play, it is more interesting through sector dispersion and selective themes such as industrial policy, infrastructure and defence.

In multi asset, the crisis is leading us to maintain a more nuanced stance across asset classes and regions. We aim to balance short-term opportunities with long-term convictions, staying slightly positive on risk and keeping a diversified stance. We also think that gold is not just a diversifier against geopolitical risks, but also a hedge against policy ambiguity from central banks.

FIXED INCOME

Duration: less directional, more granular

Amaury D’ORSAY |

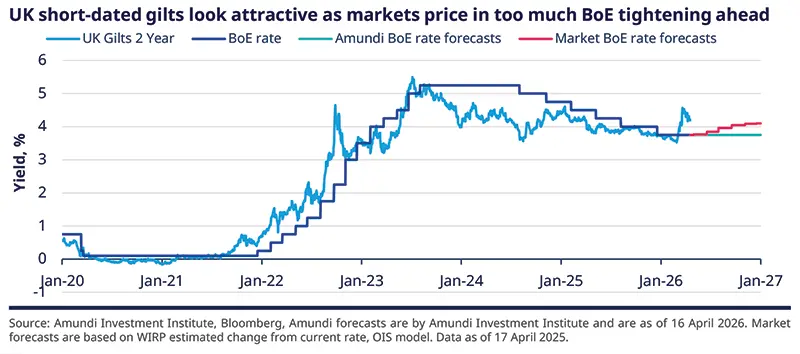

Market pricing of central bank policy decisions has changed from a slight rate cut (at the start of the war) to rate hikes now, particularly for the ECB and the BOE. While we acknowledge the concerns around inflation that have led to this repricing, we do not agree with the degree of this repricing for instance in the case of UK gilts. We also think government bonds in general could see ample supply and that could pressure yields.

Hence, instead of taking bold directional bets, we prefer to be selective across the curves and look for extra yields across corporate credit and EM. The latter has shown resilience in the face of geopolitical stress. It continues to offer strong carry, including in the high-yielding space, but one risk is of an extreme escalation in the Middle East (not our base case).

We remain constructive on duration overall. In the US, we upgraded US duration to neutral, mainly through short- and medium-dated maturities as fiscal risks weigh on rates. We are positive on linkers.

In the EMU, we favour 2Y–5Y versus 30Y steepeners and prefer the short end of the curve, while still seeing peripherals as relatively attractive, though less so at current levels.

In the UK, we have raised our stance on duration mainly at the short end, while we have downgraded Japan and continue to favour curve flattening.

We remain constructive IG credit overall. We are also selectively exploring the US and favour front‑end and belly maturities, with subordinated debt preferred over HY.

In Europe IG, we favour selective BBB/BB-rated credit and financials, keeping safeguards in place on credit and rates. We also maintain a preference for 2Y maturities.

We remain slightly cautious on HY, where valuations look fair and technicals are supportive, but selectivity remains key across sectors and ratings.

Regionally, we prefer LatAm. Countries such as Brazil, Argentina and Mexico are more resilient, given their oil and gas exposure and agricultural commodities.

In LC debt, we remain constructive, particularly on Brazil, South Africa and Hungary and are exploring opportunities where the sell-off has been excessive.

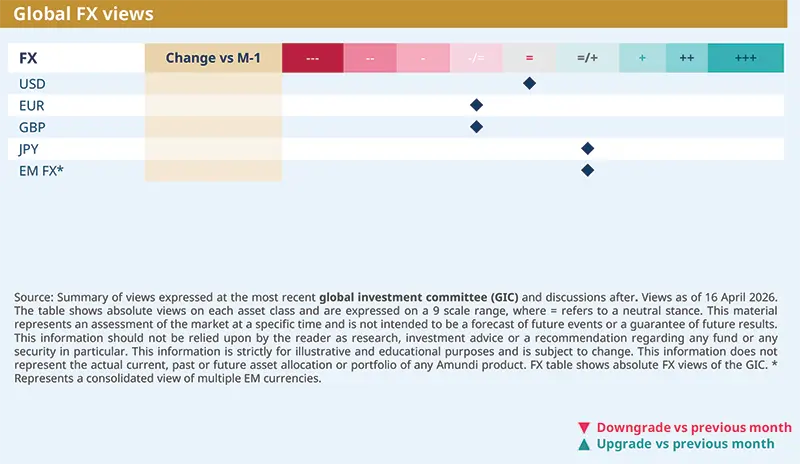

We like higher carry EM FX, such as Brazil, Mexico and South Africa, and selective Frontier countries.

In DM FX, we maintain our cautious structural view on the dollar, but tactically we are neutral.

EQUITIES

Markets calling for a swift resolution

Barry GLAVIN |

The massive change in behaviour of equities indicates optimism around a quick resolution of the crisis, but the actual path could be trickier, even if there is a temporary ceasefire. This crisis is not changing our structural convictions around Europe, Japan and EM (ie, Latin America, EM Asia), but we acknowledge the potential for near-term volatility. Additionally, this crisis is keeping us vigilant in exploring areas of resilience (where market moves have been excessive) around these long-term convictions.

Secondly, we now see a greater case for market dispersion rather than a single broad market direction. In Europe, we see second-round beneficiaries from the capex boost in the region and the push towards strategic autonomy. Finally, in the AI complex, markets are now rightly focused on the monetisation of investments, obsolescence risks, and EPS delivery.

We continue to focus on long-term opportunities, particularly in Europe, Japan and EMs, which remain attractive despite their sensitivity to oil prices. We favour banks with improving shareholder returns, industrials benefiting from exposure to energy efficiency, automation & AI capex (eg. data centres), and selected companies in consumer staples.

In Europe, the push to implement reforms, improve efficiency and accelerate electrification is gaining traction. We favour stocks benefiting from these trends, as well as select mid-caps on valuations near historic lows.

In Japan, the idiosyncratic drivers of our investment thesis (e.g., the corporate reform agenda) are becoming more attractive in the current environment.

More selective in EM and favour idiosyncratic risks. The sharp rebound in EM is an indicator of how quickly markets can change their views. We remain focused on fundamentals, valuations, the consumption story and external finances that are attractive in many regions including Latin America. On the other hand, the crisis has led us to reduce our stance on countries like the UAE, although we remain positive on South Africa.

Asia should benefit from a tech and semiconductor cycle. At a country level, select South Korean businesses will gain from the strong demand for memory chips, particularly from US and Chinese companies. In China, recent GDP growth data has shown resilience, and the country also holds large energy reserves. While we are neutral presently, we will be vigilant.

MULTI-ASSET

Active stance: exploit market dislocations

Francesco SANDRINI CIO Italy & Global Head of Multi-Asset | John O’TOOLE Global Head - CIO Solutions |

As the crisis continues to evolve, we are looking ahead with an eye on risks regarding the pass-through of higher raw material costs and supply disruptions to corporate margins or consumer inflation. Long-term inflation expectations have not re-priced in a 2022-like way, suggesting that the shock is more about growth and costs than a structural shift in the inflation regime. On the market front, this allows us to remain active and tactical, particularly in areas where valuations are not better than before, and where fundamentals remain robust. Hence, we have tactically raised our stance on equities. Given the persisting geopolitical and economic risks, we think it’s an opportune time to enhance safeguards and maintain a well-diversified stance.

In equities, following the sharp volatility over recent weeks, we have tactically upgraded our stance on the S&P 500 and LatAm. These markets offer a more compelling risk/reward profile, are supported by resilient earnings revisions and, in the case of LatAm, show continued foreign inflows. Secondly, they do not rely on imports for their energy needs.

Duration continues to offer value, particularly for US 5Y and German bonds. Importantly, we’ve raised our constructive view on the BTP-Bund spread, which has widened materially since the Iran-related escalation, making the carry it offers even more appealing. With the Italian referendum behind us and a stable Italian government, volatility should ease and spreads should stabilise. Additionally, we see limited concerns around Italy’s deficit compared with its European peers.

FX remains a key pillar of our multi asset views, wherein we remain cautious on the dollar from a long-term perspective. We’ve become less positive on the NOK vs the EUR following recent moves. The currency remains supported by Norway’s energy exposure, given the uncertain geopolitical environment. Additionally, we’ve rotated our positive view from EUR vs USD to AUD vs USD. Finally, we tactically downgraded EM FX to neutral.

We are separating strategic convictions from short-term movements. Hence, even though we are mildly constructive on risk we believe geopolitical uncertainty calls for ample safeguards in the near term.

VIEWS

Amundi views by asset classes

Definitions & Abbreviations

Currency abbreviations: USD – US dollar, BRL – Brazilian real, JPY – Japanese yen, GBP – British pound sterling, EUR – Euro, CAD – Canadian dollar, SEK – Swedish krona, NOK – Norwegian krone, CHF – Swiss Franc, NZD – New Zealand dollar, AUD – Australian dollar, CNY – Chinese Renminbi, CLP – Chilean Peso, MXN – Mexican Peso, IDR – Indonesian Rupiah, RUB – Russian Ruble, ZAR – South African Rand, TRY – Turkish lira, KRW – South Korean Won, THB – Thai Baht, HUF – Hungarian Forint.

Authors