Summary

Executive summary

Japanese equities traded at a discount

The Japanese equity market has underperformed for many years and has traded at a lower price-to-book (P/B) valuation than global peers. This discount has been warranted because return-on-equity (ROE) has been lower, reflecting an inflated denominator: balance sheets are overly large. Many companies have hoarded excess cash, held sizable stakes in other companies and built significant property portfolios. Those assets are not required for operations and represent poor uses of shareholder capital.

Corporate governance reform tackling Japan’s valuation discount

Over a decade ago, under Prime Minister Shinzo Abe, Japanese regulators pushed a corporate governance agenda to ensure businesses allocated capital more efficiently and acted in shareholders’ best interests. Since then, many companies have divested non core assets, reduced cash balances and returned excess capital to shareholders. These actions shrink the ROE denominator, lift ROE, support higher P/B multiples and increase earnings per share (EPS) as shares outstanding decline. Nevertheless, Japan Inc. still needs further balance-sheet reform and shareholders should benefit as value is unlocked over the coming years.

Economic backdrop provides additional tailwinds

Furthermore, this process has more recently been playing out against an increasingly favourable economic backdrop. The Japanese economy appears to be emerging from decades of secular deflation. Stronger nominal GDP growth and a more normal interest-rate regime provide a substantially healthier environment for corporate profitability.

Japan disciplined adaptation to a world of controlled disorder

We believe this time is different for Japanese equities. A political reset has enabled a disciplined, large-scale integration of fiscal activism, security, and technology policy. Japan has exited deflation both economically and psychologically, is building capacity rather than imposing austerity, and is repositioning as a strategic anchor in the Indo-Pacific. Social constraints are managed through technology, marking a structural—not cyclical—shift.

"While near‑term volatility in Japanese equities due to interest‑rate normalisation and political risk is possible, the structural story—driven by corporate governance reform—is creating opportunities. There is a strong case for Japan’s mid‑ and small‑cap universe, whose valuation discounts to large-cap peers should offer upside as those reforms take hold."

Vincent Mortier - Group CIO, Amundi

Monica Defend - Head of Amundi Investment Institute

Insights from the Tokyo Stock Exchange

Chad Cecere | Kengo Somei Manager, Global Equities Marketing - TSE |

An Amundi Investment Institute interview with Chad Cecere, Senior Manager, Global Equities Marketing and Kengo Somei, Manager, Global Equities Marketing from the TSE.

How did Abenomics, regulators and investors reshape Japan’s corporate governance?

Since 2013, Abenomics has put corporate governance centre stage as a way to kick start Japan’s economy. It has not been the effort of one agency alone: the TSE, the FSA, the Ministry of Economy, Trade and Industry (METI) and domestic asset owners have all worked together to push reforms across the market. The goal is straightforward — to encourage listed companies to boost productivity, improve returns on capital and reorganise so they can grow. Importantly, the focus is on durable, long term change rather than chasing quick wins or short term scorecards.

Think of the two codes as the two wheels of the same car: investors on one side, companies on the other — both pushing governance reform forward. They are updated regularly: the Stewardship Code was refreshed last year, and the Corporate Governance code is now being tightened to focus more on capital allocation and cash use. Alongside changes to the Companies Act (2006) and new METI guidance, it is now easier for companies to put these standards into practice1. Together, these shifts are pushing companies to use capital more efficiently and to prioritise long‑term value creation.

Why did the TSE engage in reform initiatives?

In 2023, the TSE was concerned that about half of Japan’s listed companies were trading below book value (price-to-book ratio ( PBR) < 1) and had ROEs under 8%. These findings were widely reported globally and served as a wake-up call for Japanese listed companies.

After the Japan Exchange Group restructured the market in 2022 into Prime, Standard and Growth segments, the TSE tightened listing rules and set up an expert panel to help companies lift their corporate value. It made “enhancing corporate value” a priority and asked companies to publish concrete plans that took the cost of capital and market valuations into account. Making those plans public improved investor understanding and sparked better dialogue.

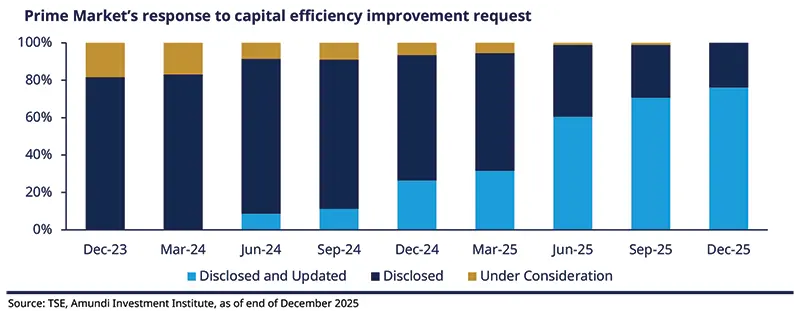

The TSE even put together a compliance list to apply a bit of peer pressure and it worked. By December 2025, more than 70% of Prime Market companies had disclosed and updated their plans, while investor engagement picked up noticeably.

What has the TSE’s reform agenda achieved so far?

We are in the “second inning” of governance reform and are already seeing results. Shareholder returns are up, valuation metrics are rising, and cross-shareholdings are beginning to unwind. Share buybacks have risen almost sixfold over the past decade, while more stable dividends have doubled. This trend is expected to continue as companies shrink their balance sheets to improve capital efficiency.

However, the work is not finished. While significant progress has been made on board structure and independence, the next challenge is ensuring governance is effective in practice. We believe the priority is the execution of the plans companies have disclosed to improve corporate value. Those changes take time, but we expect tangible progress through 2026 and beyond.

Which specific policy or regulatory changes would encourage international investors?

We expect the Corporate Governance Code to require companies to justify their resource allocation while the TSE may tighten rules on independent directors to strengthen board oversight and protect minority shareholders2. We have already seen the METI’s 2023 takeover (TOB) guidelines boost takeover bids and management-buyout (MBO) activity. The TSE’s engagement with companies continues. For example, the TSE president is visiting listed companies across Japan. Overall, the aim is to foster a growth-oriented mindset and offer plenty of investable opportunities across both small- and large-cap stocks.

Investors are positive about changes, but there are concerns about stock--based compensation, large cash reserves, conglomerate discounts and small/mid-cap liquidity where investor-company engagement is key.

From deflation’s drag to reflation’s lift: Japan’s economic reset

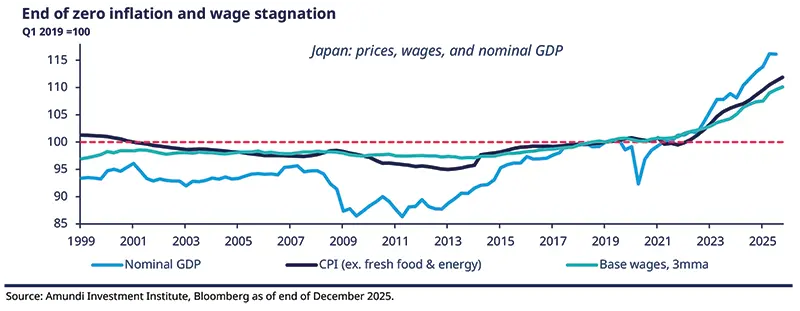

Japan has now entered its fourth consecutive year of meaningful inflation, with headline and core CPI (excluding fresh food and energy) averaging 3.1% from 2023 to 2025. While the Bank of Japan (BoJ) attributes the initial post-Covid rise to cost-push factors, and the more recent increase to rice prices, the broader picture suggests a deeper and more persistent shift in inflation dynamics.

Both new and traditional underlying inflation indicators have firmed at around 1.5% and are trending higher, while the inflation expectations across households, corporates and markets have become more persistent and broader‑based. Meanwhile, the Shuntō (the annual spring wage negotiations) delivered solid base pay rises for the third consecutive year in 2025, and wages are now up by more than 2% after two decades of near‑zero growth. Amid acute labour shortages, worker mobility has improved, signalling an early structural shift in the labour market.

Corporate Japan awakens to an inflationary reality

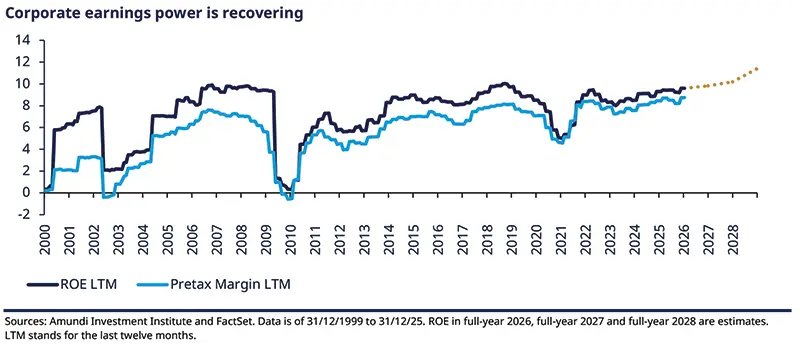

With households increasingly and persistently convinced that prices will rise, corporates have regained pricing power. In 2025, nominal GDP climbed strongly (+4.5%) and Japanese corporates delivered not only higher revenues but also margin expansion and meaningful earnings growth despite tariff shocks. Markets’ chief fear had been classic cost‑push inflation - rising input costs that squeeze margins even as sales rise - yet companies have generally been able to pass through higher prices, making inflation a net positive for profitability. Crucially, while the yen remains a volatile swing factor that can dent reported results episodically, the return of inflation has been a steadier, more persistent source of earnings growth over the medium-term.

Another distinctive feature of Japanese corporates is their oversized cash buffers, exposure to non-operating assets, pervasive cross shareholdings that have long depressed capital efficiency. In a deflationary era this behaviour made sense: cash preserved value and risk aversion was rational. Reflation alters that calculus. The return of inflation, higher rates, and severe labour constraints have forced firms to reassess returns, shutter unprofitable projects, and re engage in M&A. In short, inflation is accelerating capital reallocation, helping firms to repair balance sheet inefficiencies and rekindle corporate “animal spirits” after decades of caution.

Unlocking Japan’s dormant cash

In an environment of rising yields and BoJ rate hikes, investors often question the potential for financial tightening. However, Japan’s private sector is cash-loaded. Households hold assets worth 5.7 times their liabilities, with about half in cash, while non-financial corporates hold more than twice the cash balances of their peers in other developed economies. This substantial financial surplus shields the economy from the tightening impact of higher rates; rising yields may even support interest income for households and aid the normalisation of the financial sector. Japan’s challenge is less about financial tightening and more about reshaping private-sector behaviour under a new regime where inflation has returned.

Claire HUANG

Japan’s challenge is less about financial tightening and more about reshaping private-sector behaviour under a new regime where inflation has returned.

Takaichi’s fiscal push: reviving Japan’s growth engine

Prime Minister Sanae Takaichi’s landslide in the lower house has given her the political capital to pursue an ambitious, pro growth fiscal agenda - a boost for Japanese equities. Her plan is being implemented in two stages: first, an affordability drive to restore positive real wage growth; second, a supply side push to raise productivity through targeted investment. A high CPI base in 2025 (largely driven by rice) and near term affordability measures should push headline inflation below 2% in 2026, creating space for longer term investment initiatives. Government funds will act as seed capital for capex across 17 critical sectors, helping to secure Japan’s role in key supply chains and accelerate AI adoption and automation.

Markets have already started to price in some of this shift. The post-election flattening of the Japan Government Bond curve suggests investors are giving Takaichi credit for her pro-growth strategy. In our view, the expansionary fiscal policy is being adopted from a position of prudence: Japan’s primary balance was 1.1% of GDP in 2024 (estimated close to zero in 2025), the smallest among the G7. Meanwhile, the government’s overall financial deficit is at its lowest in three decades. Importantly, reflation can help the debt dynamics by growing nominal GDP, making it easier to reduce the deb- to-GDP ratio over time.

We expect Japan to grow at more than 3% in the medium-term under this mix of reflation, corporate reallocation and fiscal supports. This would allow a controlled widening of the primary deficit to about 2%, assuming debt service costs remain in the 2–3% range. After decades of stop start policy and occasional premature consolidations, a renewed, credible focus on strategic sectors and supply chain resilience is now more politically and internationally acceptable - not least in the wake of similar pivot in Europe. Takaichi therefore benefits from favourable timing, strategic position and solid public support; the conditions for a meaningful fiscal renaissance in Japan are unusually well aligned.

Yen in transition: valuation and flows support a stronger yen In contrast to the euro’s relative strength, the yen weakened through late 2025, largely as a victim of the fiscal dominance narrative rather than a fiscal renaissance. After Takaichi first became LDP leader in October, a fiscal risk premium persisted and markets ran a simple “Takaichi trade” – short Japanese Government Bonds (JGBs), short yen, long equities - while the yen’s safe haven role looked fragile without repatriation flows. Since her landslide in the legislative election in early February, the market response has grown more granular: post election moves partly unwound the initial “Takaichi trade”, the yield curve flattened, back end JGBs stabilised, and the yen has shown episodic strength as investors focus on fiscal sizing, timing and the BoJ’s operational independence rather than headlines. Our house view remains that 2026 is primarily a dollar weakening story. Broad dollar depreciation has gathered pace on fresh US political noise, and the US core disinflation is more advanced than commonly assumed. Beyond a weak dollar, support for the yen is rooted in valuation and flows: extreme cheapness on various metrics makes the yen sensitive to repatriation, carry unwind and intervention signals. Furthermore, the same policy dynamic that has supported a firmer euro could start to favour the yen if fiscal easing in Japan spurs domestic activity. Downside risks remain: a durable fiscal dominance outcome that forces BoJ monetisation, or an unchecked fiscal impulse larger than markets expect, would reopen yen depreciation pressures. |

Japan equity at a turning point: from value trap to structural win

Japanese equities has underperformed other developed markets

For decades, Japanese companies have prioritised building up cash reserves instead of investing to improve capital efficiency or acting in the interest of shareholders. That behaviour squandered opportunities to redeploy capital into higher-return projects. Payout ratios, share buybacks and M&A activity remained low as cross-shareholdings reduced the pressure on management to maximise shareholder value. Structurally, Japan’s market is underweight the mega‑cap technology winners that drove much of the US rally, a composition gap that materially depressed relative returns. Finally, the prolonged low‑rate environment, stagnant growth and compressed yields further undermined the case for sustained equity outperformance.

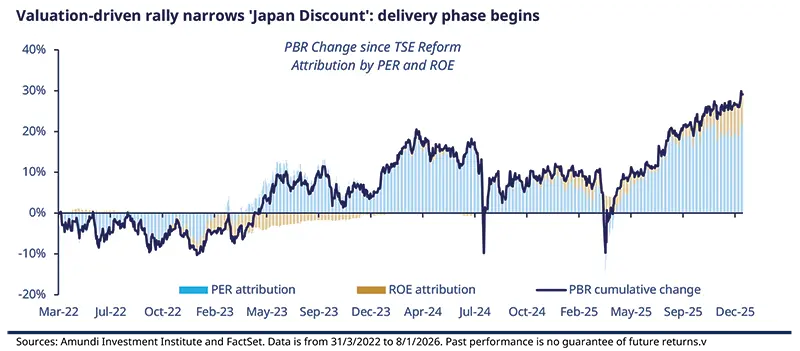

Multiples: The story so far

In recent years, Japanese equities staged a notable rally versus peers. That rally was driven by a mixture of the forward-looking policies of Sanaenomics and reforms reshaping companies’ priorities around balance-sheet discipline, shareholder returns and sustainable growth. So far, the rally has mostly been a multiples story. Investors have paid higher price-to-earnings (P/E) ratios for the same profits, rather than wait for earnings to rise. The long‑standing “Japan discount” is shrinking as companies enter a market‑driven, self‑sustaining phase of reform.

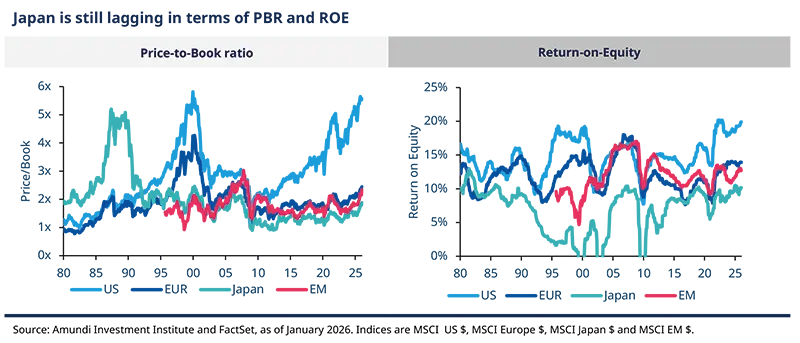

Evolution of Japan’s relative PBR and ROE

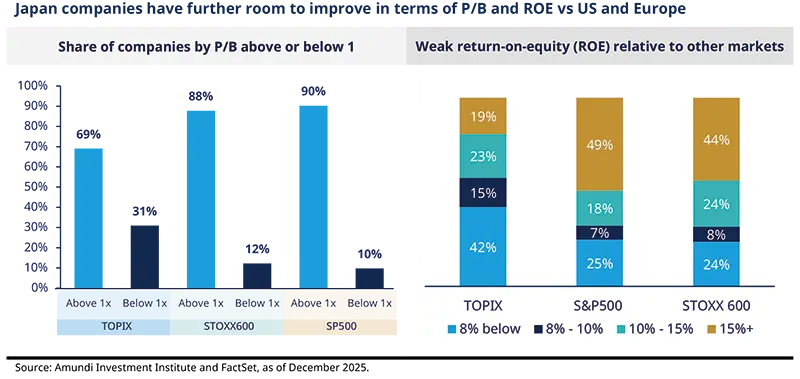

TOPIX has historically traded at materially lower PBRs than US indices, which have often traded at much higher PBRs during tech‑led rallies. Europe’s PBR typically falls between Japan and the US, while emerging markets (EMs) are mixed: some — particularly tech exporters and commodity producers — trade at higher PBRs than Japan, while others trade lower, reflecting country risk. On ROE, TOPIX has generally lagged the US and Europe—held down by large corporate cash balances that earn near-zero returns—while EMs’ ROEs vary and are often higher. A sustained rise in Japan’s ROE could trigger a significant rerating of the market.

In recent years, both metrics in Japan have improved. The TSE’s directive has urged companies to put more of that cash into wages, productive investment and shareholder returns. That push has already triggered meaningful change visible across sectors and market caps. However, a gap versus the US and some European markets remains.

Investor implications of Japan’s corporate reforms

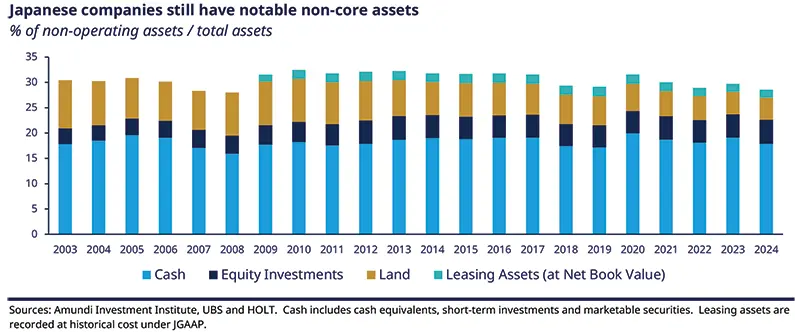

There is room for further change. Even though the reforms are largely taking hold, Japanese companies are still holding cash balances significantly larger than those of their global peers. Their non-operating assets amount to 28.6% of total assets, higher than US and European averages (mid-to-high teens). However, the governance reforms and macroeconomic changes are pushing Japanese companies to trim low-margin businesses and pursue M&A to expand higher‑return operations. Nevertheless, though many diversified groups still carry low-profit segments.

Share buybacks have accelerated, especially at cash-rich companies under growing pressure from shareholders, and dividend hikes have also been common. Shareholder distributions have therefore surged, with buybacks accounting for nearly 90% year‑on‑year increase in 2024 and they remained at a solid pace through 2025 despite global instability3. However, aggregate payout ratios still lag those of Western markets, suggesting that shareholder returns are likely to strengthen further.

Barry GLAVIN

There are two secular forces at play driving the improvement in Japanese earnings: reflation and enhanced capital productivity. These tailwinds are unique, and investors should benefit as the valuation discount progressively unwinds relative to other markets.

In summary, companies are allocating capital more efficiently, improving governance and raising dividends and buybacks. These changes are beginning to lift earnings. As a result, the market rally is increasingly backed by improving fundamentals, rather than sentiment alone, making it broader and more sustainable.

An equity perspective on structural reforms and reflation

Hiromi Ishihara | Paula Niall Investment Insights Specialist, Amundi Investment Institute |

Interview with Hiromi Ishihara, Head of Equity Japan, Amundi Japan by Paula Niall, Investment Insights Specialist at the Amundi Investment Institute.

Hiromi, which companies are likely to be re‑rated after corporate governance improvements?

We use a bottom-up, value-oriented approach. That means we look for financially healthy companies trading at meaningful discounts with clear catalysts to unlock value for shareholders. The catalysts we seek include notable selling of non‑core assets, stronger shareholder-return policies (dividends and share buybacks) and improved communication and governance. We invest where management can take concrete actions to materially lift valuations, and we are finding such opportunities within the SMID (small- and mid-cap) universe. From a sector perspective, the industrials and banks are particularly attractive.

Hiromi, how can governance reform create opportunities in the SMID universe?

Our strategy targets SMID companies trading below book value and sitting on substantial cash balances which have not been put to work. We look for stocks with clear catalysts to realise value and, crucially, with boards willing to change. Assessing management’s commitment to taking the necessary steps to create lasting corporate value is more important than ever. To avoid value traps, deep fundamental research and active engagement with management are central to our approach.

Why would Japanese banks benefit from reflation and governance reform?

Banks are clear beneficiaries of Japan’s reflation, governance reforms and rising interest rates. We expect further BoJ hikes to support domestic net interest margins (NIMs). In addition to these technical benefits, we have seen an increase in loan demand as economic activity picks up, which also strengthens banks’ fundamentals. With loan rates rising faster than deposit rates, expectations for higher ROEs and bigger shareholder payouts are growing. Many banks have strong capital buffers, so there’s room to lift dividends and step up share buybacks—especially as they unwind long‑standing cross‑shareholdings. A few have already begun, but most still need to act. If banks continue to tighten capital discipline, cut costs and improve governance, the sector should be well-placed for a sustained re‑rating. Regional banks, in particular, look attractive on both valuation and fundamentals.

Hiromi, which industrials will benefit most from the cabinet’s three‑year capex programme — and why?

Construction looks set to be a clear winner. Companies are responding to reform‑driven pressure by improving capital efficiency and shedding non‑core assets; many also have scope to boost shareholder returns and pursue M&A. Takaichi’s pro-growth policies including increased infrastructure capex, should benefit the sector and translate into larger order books for construction companies.

Hiromi ISHIHARA

The end of deflation and faster governance reform make balance-sheet repair essential. Companies should only back investments that offer clear returns and pricing power, and markets will reward such actions.

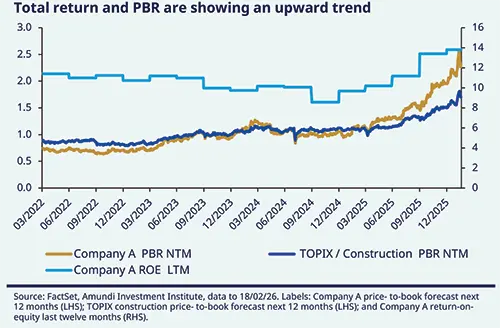

Case study: Reforms at work

This case study shows that TSE reform is not just rhetoric; it is changing how companies make decisions. We are still early in the process of these structural changes translating into higher corporate values and generating opportunities. Founded in 1840, the group is one of Japan’s leading general contractors. Historically strong in government civil works, it was an early developer of high rise construction, nuclear power plants and seismic technologies. Today, the group combines construction expertise with a growing property development business.

TSE reform shifted focus to growth, balance-sheet efficiency and shareholder‑returns The company announced a new mid-term business plan and capital strategy for FY2024 - FY20264.

Activities encouraged by reforms: Business portfolio reviews & governance discipline

|

Conclusions

After decades of underperformance driven by low ROE, oversized balance sheets and pervasive cross shareholdings, Japan appears to be at a structural inflection point. Coordinated governance reforms – at the TSE, METI and through stewardship and corporate governance updates) and policy support from Abenomics/Sanaenomics are forcing companies to shed non core assets, return excess capital and tighten capital allocation. At the same time, reflation, rising wages and higher rates are restoring pricing power and profitability.

Although the rally has so far been valuation led, rising ROEs, accelerating buybacks/dividends and improved capital discipline indicate that fundamentals are beginning to underpin a more durable rerating—notably among SMID stocks, banks and industrials. Execution risk remains, but if companies follow through on their plans, investors should see meaningful value unlocks over the coming years.

Investor demand for Japanese equities is rising. Foreign investor interest in Japanese equities strengthened markedly in 2025, with net purchases on the Tokyo and Nagoya cash exchanges totaling ¥5.4 trillion ($35 billion) — 35 times the 2024 level. Momentum accelerated further in early 2026, supported by Takaichi’s victory, with a record ¥3.9 trillion in net buying over just six weeks. We believe that demand will continue, as overall positioning in Japanese equities is still light. With USD on a structurally weaker trend and rising demand for global diversification amid high geopolitical uncertainty and extreme concentration risk in the US, Japan is emerging as a key opportunity for global investors.

Claudia BERTINO

Stock‑exchange governance reforms and the end of deflation have sparked renewed international interest in Japanese equities at a time when demand for diversification is high.

1. The METI guidance is a set of recommendations from Japan’s Ministry of Economy, Trade and Industry that complements the Stewardship Code and Corporate Governance Code. It translates the high level principles of those codes into concrete expectations for corporate behaviour — especially around capital allocation, use of cash, disclosures and board responsibilities — and signals what policymakers expect listed companies to do even though the guidance itself is not law.

2. https://www.fsa.go.jp/en/refer/councils/revision_corporategovernance/material/20251021/04.pdf

3. The 2025 figure for shareholder distributions is not available yet.

4. The fiscal year in Japan is April to March.

Authors