Summary

Emerging markets debt performance is ultimately driven by a combination of global and domestic forces. Global and domestic conditions set the backdrop against which capital flows, borrowing costs, and currency dynamics are determined, while domestic policy credibility and market structure decide whether countries can absorb external shocks or amplify them.

Global financial conditions are often the first pressure point for EM debt

Global financial conditions are shaped primarily by major central banks and key market variables such as core yields. When the Federal Reserve or other key central banks adopt or maintain restrictive policies, global liquidity tightens, financing costs rise, and risk appetite weakens. However, a tightening in financial conditions is not always the result of central bank action. A major macro-financial shock can also tighten global financial conditions. In such an environment, EM debt generally comes under pressure, with local yields rising and/or spreads widening. The impact is typically more acute in countries with large short-term external financing needs.

Domestic conditions determine whether a negative impact is temporary or more persistent

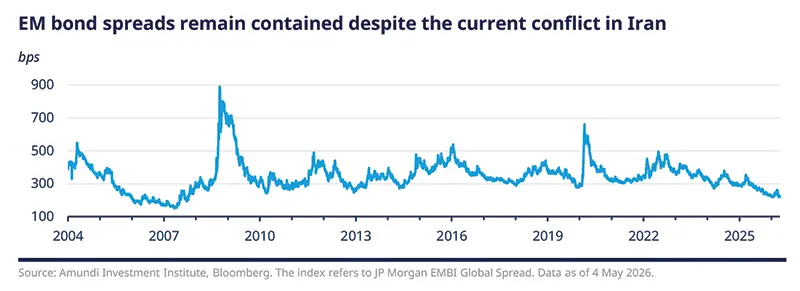

At present, the conflict in the Middle East has raised the risk of a stagflationary shock for the global economy. Despite the initial negative market reaction to the Iran conflict, EM bond spreads have demonstrated considerable resilience and have now returned to pre-war levels. However, the greatest impact is likely to fall on net energy and commodity importers, whose external and fiscal positions may deteriorate while inflation rises. Over time, investors will need to monitor how domestic authorities respond and whether monetary and fiscal policy remain credible. In recent years, through crises such as Covid and the commodity shock caused by the war in Ukraine, EM countries have shown that they are no longer defined by the stereotype of irresponsible policymakers. Many responded promptly and decisively to inflationary pressures, while also showing relative fiscal responsibility, particularly when compared with policymakers in advanced economies. The EM policy premium has clearly increased. This improvement in policy behaviour has become a structural anchor for EM debt resilience.

The US dollar remains a critical variable

A stronger dollar often tightens financial conditions for EM borrowers, particularly those with dollar-denominated debt or limited foreign exchange reserves. Weakening EM currencies can feed a vicious spiral, adding inflationary pressure to the picture. These pressures can lead to larger outflows and make refinancing more difficult. The current systemic risk has reinforced the dollar’s safe-haven status. While the world remains structurally net short dollars, over the years, dollar-denominated debt has declined across EM, and debt management offices have increasingly tapped domestic markets, supporting a gradual shift towards de-dollarisation.

EM debt benefits from growth and liquidity

Stronger EM GDP growth should support a better relative return profile for EM debt, with healthier fiscal dynamics and greater room for debt servicing. In addition, stronger growth relative to advanced economies can attract capital and support debt resilience, even when global conditions are less favourable.

Ample liquidity and positive risk sentiment can also support EM debt. EM debt is highly sensitive to global risk appetite. In periods of abundant liquidity and optimistic sentiment, investors search for yield and move into higher-beta assets, including EM sovereign and corporate debt. Over time, better policymaking and political reform have helped EM spreads tighten significantly.

Institutional creditors and bondholders have also become more successful in distress resolution and bond restructuring, while default rates remain well below the historical average seen since the late 1990s. The expansion of private debt has also helped sustain liquidity, although this resilience has yet to be fully tested in systemic bear markets.

Given the importance of global factors, markets can sell off sharply during periods of systemic stress regardless of country-specific fundamentals. This is why EM debt often trades as much on global positioning as on domestic fundamentals.

Domestic policy drives performance

Domestic policy soundness determines whether a country can benefit from favourable global conditions or remain vulnerable when the cycle turns. Fiscal orthodoxy is central. Countries that maintain credible budgets, avoid persistent primary deficits, and demonstrate a willingness to adjust spending when needed usually enjoy lower risk premia.

A broad and efficient tax base is equally important. Countries that rely on narrow or volatile revenue sources, as is often the case for commodity exporters, tend to face more unstable public finances unless they diversify their revenue base. A wider tax base improves resilience, reduces dependence on commodity cycles or one-off revenues, and gives governments more room to respond to shocks without undermining confidence. A credible fiscal rule can further reinforce discipline. Well-designed rules help anchor expectations, limit pro-cyclical spending, and signal commitment to debt sustainability. However, such rules must be backed by political will and institutional strength; otherwise, they risk becoming symbolic rather than binding.

Monetary policy credibility also plays a major role. Where central banks are independent, transparent, and focused on price stability, especially once they have adopted a credible inflation-targeting framework, investors are more willing to hold local debt and local currency instruments. Weak monetary policy frameworks, fiscal dominance, or repeated policy surprises tend to fuel inflation risk and raise borrowing costs across the curve. EM central banks are already changing their monetary policy stance amid fears of inflation de-anchoring.

The depth of the domestic financial market is another important source of resilience. Countries with a broad local investor base, developed bond markets, and active pension or insurance sectors are less dependent on volatile external funding. Deeper markets improve liquidity, support longer maturities, and reduce rollover risk. Shallow markets, by contrast, leave governments and corporates more exposed to sudden shifts in external sentiment.

The best EM stories combine growth and credibility

For EM debt investors, the key lesson is that external conditions and domestic policy quality interact. Favourable global liquidity can lift even weak credits for a time, but durable outperformance usually depends on sound institutions, fiscal discipline, credible monetary policy, and a sufficiently deep domestic investor base. In practice, the best EM debt stories are those where a decent growth premium is matched by strong policy credibility.

Key takeaways on EM fixed income from the desk

|

Authors