16/07/2025 Portfolio Strategy A brief history of US protectionism and global trade Understanding the historical dynamics of trade and protectionism provides insight into today's increasingly multipolar world.

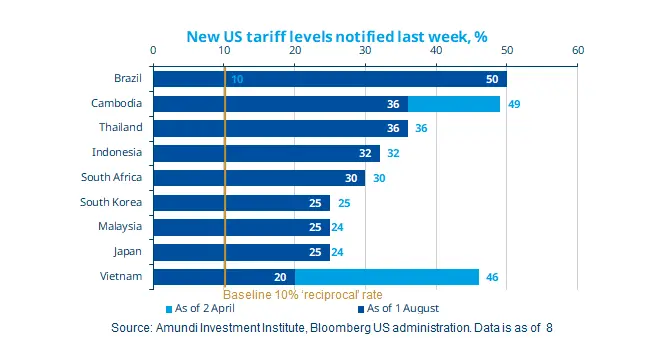

15/07/2025 US tariffs delayed to August While tariff implementation has been postponed, policymakers and central banks await clarity on the impact on the economy.