Invitation | 2026 Global Investment Outlook: Keep It Turning

Join Amundi on November 19 as our experts assess whether global markets can sustain their momentum over the year ahead — from macro trends and sector rotation to technology, fiscal policy, & regional growth signals.

India’s great transformation: opportunities for global investors

In this paper we examine the multi‑faceted transformation of India’s economy and financial markets and the implications for global investors.

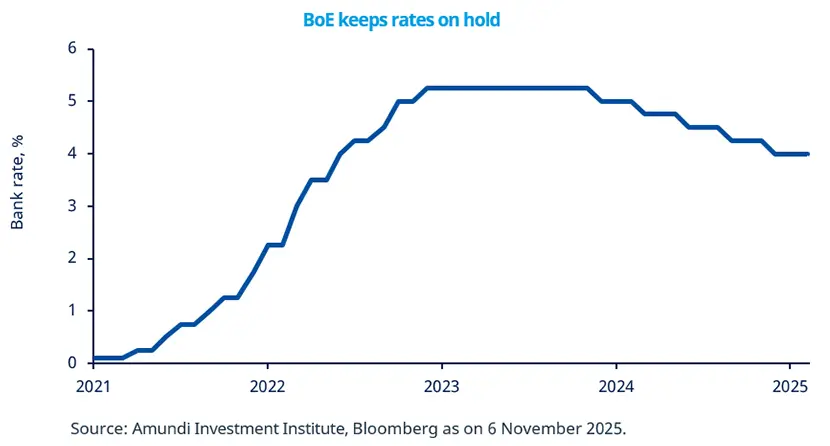

Global Investment Views - November 2025

The GIV elaborates on the latest views, convictions and outlook of our Global CIOs, Investment Platforms and the Amundi Investment Institute.

Resilient Emerging Markets in the Great Diversification

Emerging Markets outlook: opportunities and risks for investing in EM assets, and the case for broader diversification of global portfolios.

Cross Asset Investment Strategy - October 2025

Discover the latest edition of our monthly publication, exploring what's behind gold's record-breaking rally and what it signals for global markets.

Blended Finance: scaling capital for sustainable impact

Blended Finance (BF) is a strategic solution in accelerating emerging markets' progress towards reaching sustainable development goals (SDGs).