Summary

Oil price and equity movements over the past weeks suggest how quickly markets can shift from an overly pessimistic to an overly optimistic scenario and vice versa. This reinforces our view that investors should maintain long-term convictions and avoid areas of high concentration risks.

An uncertain and volatile environment around US-Iran negotiations is affecting oil prices. Any sign of subsiding war risks would obviously be positive for the markets.

What matters most for the economy is the flow of shipping traffic through the Strait of Hormuz.

We think investors should avoid being carried away by excessive euphoria and stay focused on long-term convictions and diversification*.

News flow relating to the Middle East crisis highlights how rapid progress — or derailment — in talks can quickly alter market sentiment. Initially, hopes that traffic through the Strait of Hormuz might reopen allowed oil prices to fall amid expectations of a resumption in supply. At the same time, a relief rally was seen across US, European and emerging-market equities. While the temporary ceasefire between the US and Iran was the obvious catalyst, the reality on the ground — particularly whether traffic through the Strait has returned to normal — may be different. This was also evident from the failure of the weekend talks between the US and Iran, which caused an expected spike in oil prices. We believe that if oil stabilises at lower levels, this would, of course, be positive for the economy. But the big question is how quickly energy production — not just oil — can return to normal levels, and this remains uncertain. As a result, it is unlikely that oil prices will settle close to pre-war levels in the near term.

* Diversification does not guarantee a profit or protect against a loss

This week at a glance

Equity markets rose in a turbulent week centred on the two-week ceasefire accord between the US and Iran, which also sent oil prices slumping. A key index of volatility in US equity markets declined sharply. US bond yields fell, as easing pressure on oil helped dampen hawkish expectations for central bank policies, whereas the picture was more mixed in Europe in terms of yields. Gold rose for the third consecutive week.

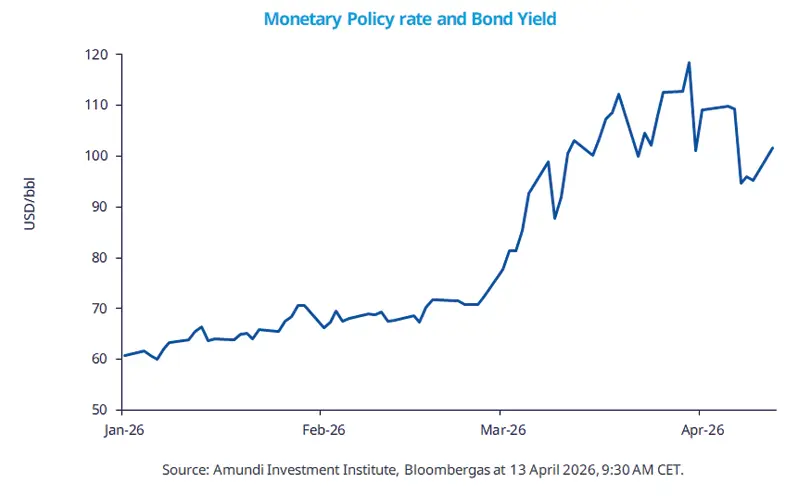

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

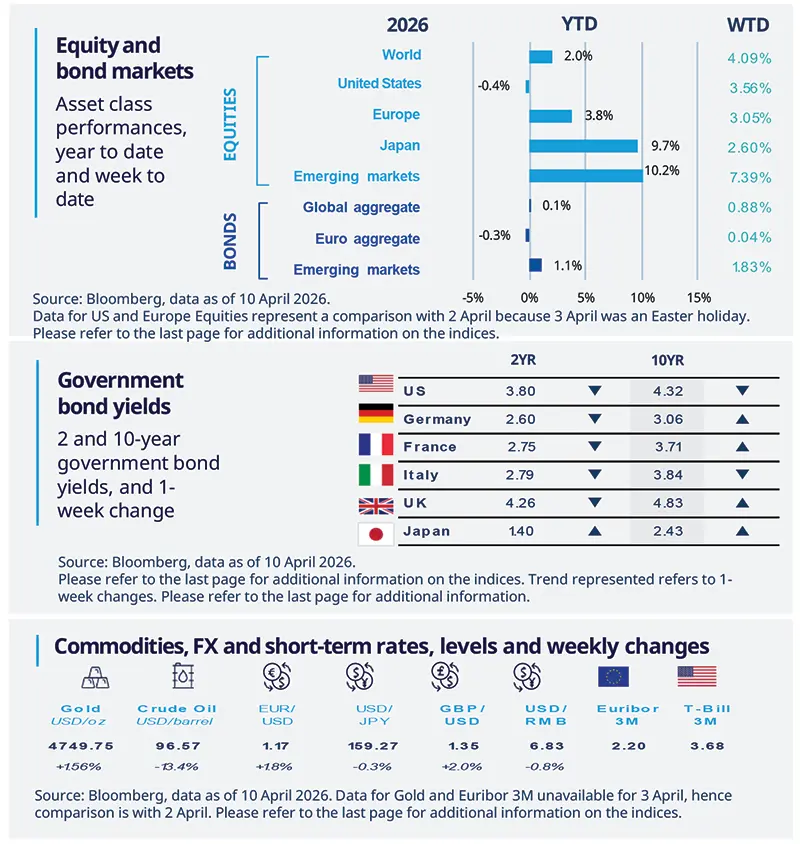

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 10 April 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US labor market shows resilience

Initial jobless claims rose modestly to 219,000 in the week to April 4, while continuing claims declined to 1,794,000. Both series remain near their 15-month lows, reinforcing the view that the labour market is broadly stable. Initial claims are also close to their lowest levels since 2017, indicating subdued inflows into unemployment and a persistent ‘low-fire, low-hire’ backdrop. Overall, the data continue to point to a labour market that is holding up well despite the energy shock, with no clear signs of deterioration.

Europe

Eurozone consumers remain cautious

EZ retail sales declined by just 0.2% MoM in February, with the weakness concentrated in food, drinks and tobacco, while non-food spending held up relatively well and fuel sales even edged higher. Retail sales rose, supported by non-food categories, suggesting that consumers remain prepared to buy beyond essentials. Overall, the picture remains reasonably constructive, though March could be softer if weaker confidence, linked to the Iran crisis, starts to feed through into spending.

Asia

China’s inflationary pressures at play

China’s CPI inflation edged up to 1% in March, from 0.8% on average in January and February, with fuel prices hikes the main contributor. This pushed non-food goods inflation to 1.8%, up from Jan-Feb. PPI inflation also turned positive for the first time since October 2022, in March. The Middle East conflict may remain an inflationary headwind for China. We expect CPI inflation may rise in 2026, but without a meaningful improvement in demand, inflation could soften again in 2027.

Key dates

US small business optimism, PPI |

EZ industrial production, US Fed beige book |

China GDP, UK Industrial production |

Authors