Summary

Keep it turning, faster

Since the start of the year, several of the key convictions we highlighted in our outlook have been playing out, and some trends have clearly accelerated. Markets have remained well supported, with significant rotations at country, sector and stock levels.

Geopolitical fragmentation and controlled disorder remain central themes, as the recent escalation in the Middle East has shown. The situation remains fluid and, for now, is best characterised as a military shock with uncertain political ramifications. Oil prices — the principal macro transmission channel — already appear to reflect a largely temporary geopolitical risk premium.

At Davos, we heard a narrative shift, a clear break in the international order. At the Munich Security Conference, and more recently in markets, we have seen steps towards policy action. President Lagarde’s reference in her speech to the ECB’s new repo facility signifies how policymakers view the growing importance of geo‑economics.

Clearly, we are moving into a more complex market equilibrium in which policy, geopolitics and capital allocation matter as much as the economic cycle. In a fast-changing world, it is a good time to reassess our main convictions:

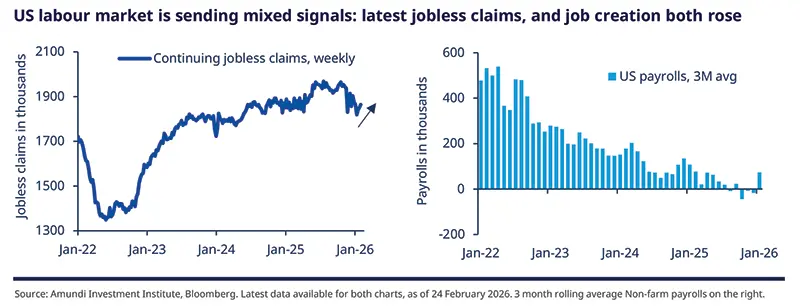

A transition with better momentum in the US and Europe, not a downturn. In the US, labour markets, which are showing mixed signals, consumption, wealth effects, and the AI-led capex boom are key factors that will drive economic activity.

Diversification in an era of controlled disorder is crucial to achieve sustainable returns across asset classes.

ECB President Lagarde’s announcement of a new euro liquidity facility at the Munich Security Conference indicates the growing connection between policy making and geoeconomics.

Think global in equities, beyond the tech race amid a more fragmented and selective global market environment.

Fiscal and monetary policies will drive investment opportunities.

Europe and emerging markets offer long-term potential.

Our convictions are based on some of the below macro views:

Consumption remains the mainstay of US growth, which we upgraded to 2.5% for this year. A mixed US labour market and robust consumption (supported by tax refunds etc.) have led us to upgrade our growth view. We are also assessing the latest changes around US tariffs. However, we would like to see more progress in areas such as jobless claims and job creation before concluding about labour markets with confidence. There are downside risks if companies lay off employees due to potential pressures on margins. In the eurozone (EZ), positive growth surprises at year-end (Italy, Spain) are welcome, and are creating a stronger carry over into 2026. We have raised this year’s projection to 1.2%.

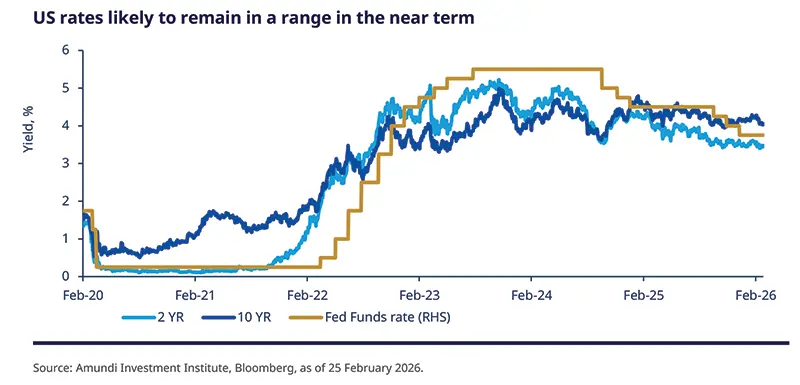

In the US, we believe disinflation will continue but inflation will remain the Federal Reserve’s target, implying there is not a lot of room for the central bank to cut rates beyond twice (25 bps mid-year and again in September). This call is based on the fragility of labour markets. We also believe that the bar for the next Fed Chair to reduce the balance sheet is high as the bank is keen to avoid stress in the repo market.

Policy making is getting intertwined with security and the broader realisation that Europe needs to build strategic autonomy, independent of the US. The ECB’s announcement of a new repo facility to improve euro liquidity for non-EU central banks is the latest signal. Regarding rate cuts, we believe the ECB will reduce rates once this year, in the third quarter. Domestic demand is improving, but wage growth is mixed.

An era of fiscal expansion confirmed in Japan, following the consolidation of power in the hands of the Prime Minister. Her policies centres on reducing inflation and boosting economic growth, both of which would have an impact on Japanese bonds and the yen. On the monetary side, we maintain our view of one rate hike, which is less than what the market expects, but in line with the recent subdued growth data for Q4.

Emerging markets such as India confirmed as a structural allocation. We might see phases of volatility, but overall the growth environment remains positive. We have upgraded this year’s GDP growth projections to 6.8%. The recent annual budget, deals such as the India-EU agreement, and any tariff relief on exports to the US are all supportive factors. Subsequently, we have removed our easing bias on the Reserve Bank of India and believe it would hold rates steady this year.

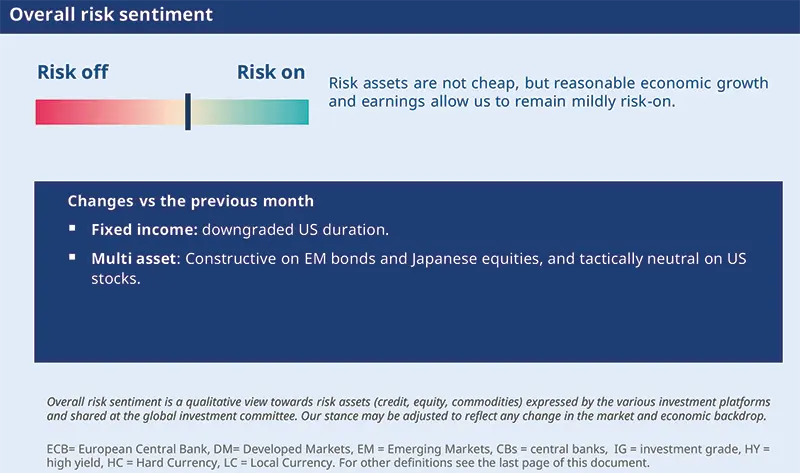

To summarise, we neither see an overheating of the economy nor a downturn this year, and maintain a moderate risk on stance. Hence, over the long term, diversification and selection look set to be better sources of returns rather than market cycles.

While volatility around US tariffs signals that trade tensions are far from over, economic momentum remains reasonably firm.

Our late-cycle environment allows us to keep a moderate risk-on stance, as outlined below:

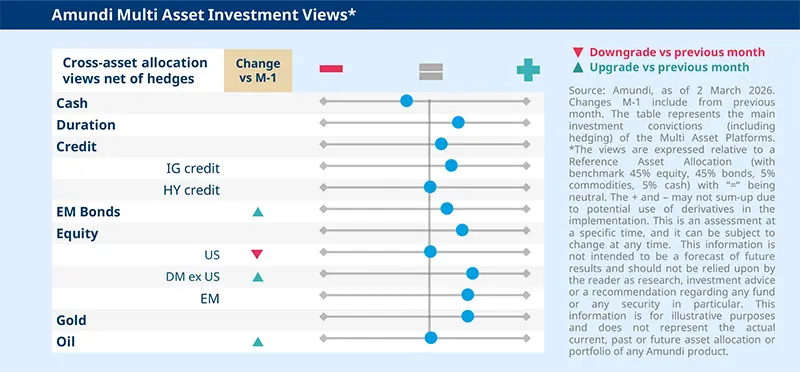

Fixed income: We are overall neutral on duration and have downgraded the US. In Japan, we have been witnessing many factors that could affect our stance. For now, we remain neutral on duration and believe the yield curve will flatten. On risk assets, we maintain a constructive view on corporate credit, and see emerging market bonds as a source of long-term returns and diversification.

Equities: We believe the volatility caused by advances in artificial intelligence is the market’s way of questioning businesses that will be disrupted by this technology. Our focus remains on identifying businesses (for instance those in the ‘real economy’) that will benefit amid this uncertainty. These include quality companies with strong balance sheets in the industrials and materials sector. We are also positive on consumer staples. Strong growth persists in emerging markets, although there are divergences across regions. We are positive on Latin America and Emerging Europe.

Multi asset: We keep a flexible approach across asset classes to identify areas of value, which we now also see in EM bonds due to their robust carry and diversification potential. Also, we are now optimistic on Japanese equities, due to strong earnings growth prospects, but neutral on US equities. Overall, we maintain a well-diversified stance.

FIXED INCOME

Rates to remain range bound

Amaury D’ORSAY |

We believe that, while disinflation will continue in the US, the overall inflation will remain between 2.5% and 3% this year, which is above the Fed target. Hence, in the very near future the Fed is likely to remain on hold. Around mid-year, when there is more visibility on inflation, the Fed may reduce rates.

At the same time, we don’t see Fed pivoting towards a rate hike, because labour markets are not giving any clear indication of improvement. Overall, rates will remain range-bound. In Asia, Japan is an outlier, and we are monitoring how the fiscal/monetary policies evolve. Overall, we stay balanced, with slightly positive views on corporate credit, EM bonds and a selective stance on duration across DM.

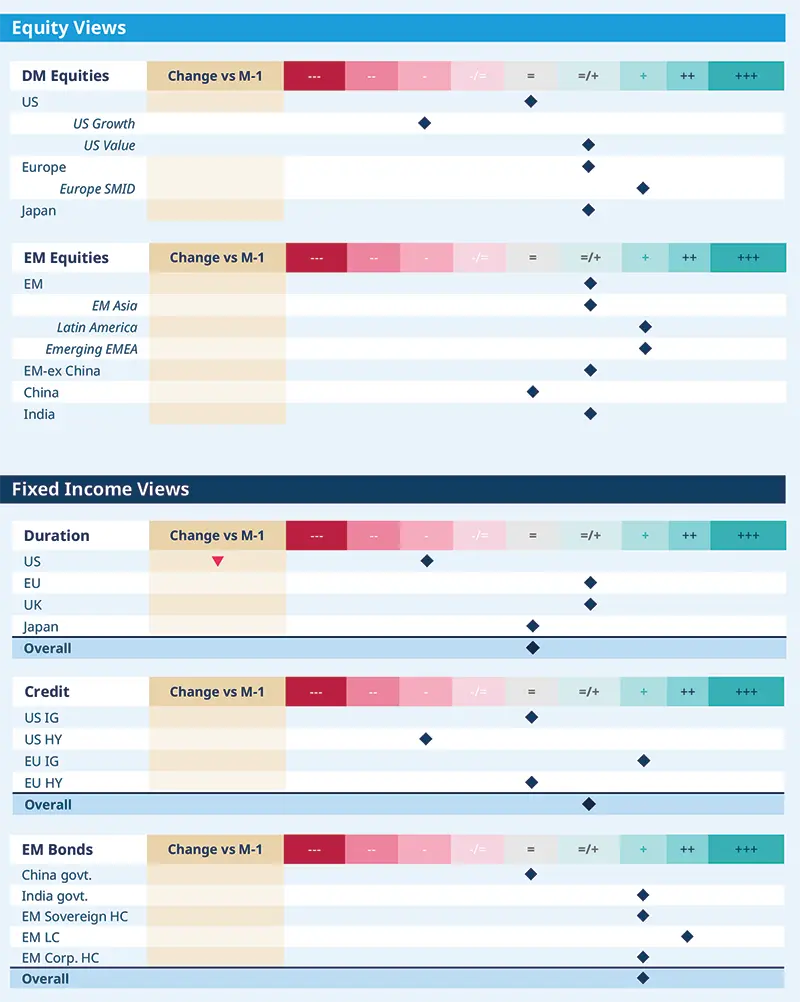

Overall neutral on duration, but turned more cautious on US – rate cuts are already priced in. We see a potential for curve steepening (5y30y).

On Japan, we are close to neutral and monitoring actively. Valuations, carry and political stability are positives, but any sign of fiscal imprudence could pressurise bonds. We also expect the yield curve to flatten (10y30y).

In the EU, we like peripheral debt and are positive on UK (mainly short end of the curve).

Corporate credit remains a source of high carry yield and high-quality credit.

From a global view, we confirm the preference for EU vs UK and US, with a constructive view on IG versus HY.

EM bonds offer good diversification opportunities and we do not see systemic risks. Uneven growth raises dispersion risk, so need is high for selection.

In particular, we like HC, sovereign, and corporate credit. But we have a bigger preference for LC debt.

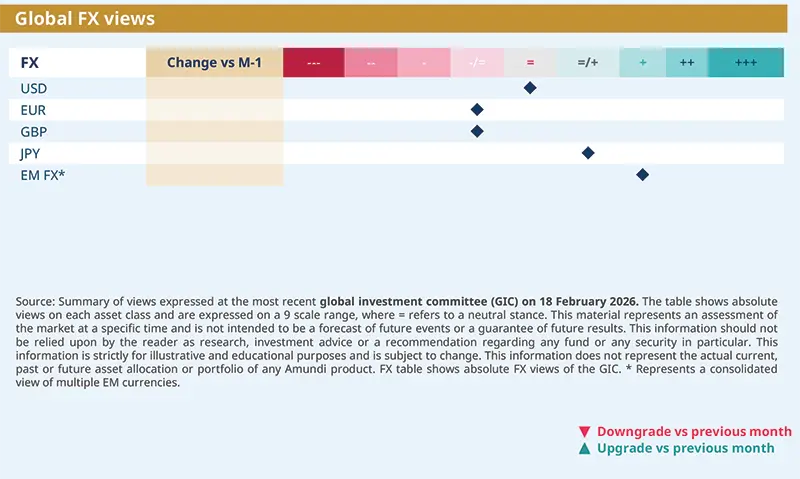

We stay neutral on the dollar. GDP growth should remain supported by the policy mix in the near term, but we see uncertainty and the declining allure of the currency as a safe-haven.

On GBP, our negative stance is maintained. The macro environment is weak and we expect rate cuts.

In EM FX, we remain positive but slightly adjusted our views in favour of Asian FX.

EQUITIES

AI disruption may support rotation

Barry GLAVIN |

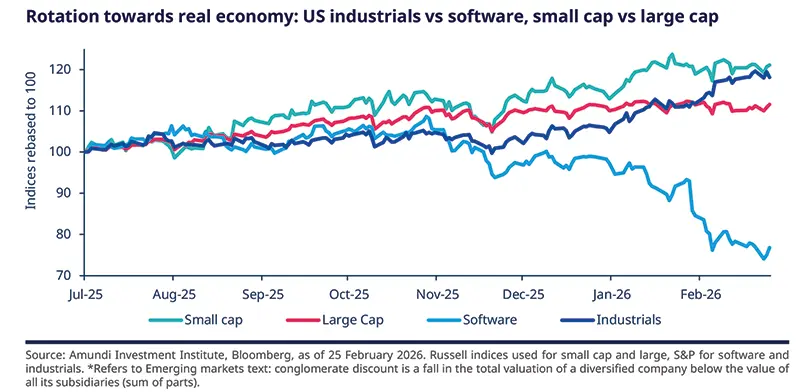

The global macro environment is decent, but tariffs have again created uncertainty in this world of controlled disorder. On the market front, volatility in equity markets, including in AI segments, is a reminder of the bona fide questions the market will ask about these companies' competitive moats and their earnings potential. Any progress on this – for example, the development of a new AI model – could result in increased volatility for companies whose business models are at risk of disruption.

We could witness a general trend favouring high-quality companies in industrials versus losers in the technology segments. Our focus remains on building a fundamental view on businesses that could sustain this rotation, and may even benefit from it, particularly in Europe, Japan and EM.

We continue to favour a globally diversified approach amid elevated concentration risks in the US.

We are positive on Japan, which should benefit from both fiscal spending and corporate reforms. The story in Japan is supported by the rising ROE and increased buybacks. In Europe, lower rates, falling energy costs, and German stimulus are supportive of earnings.

Sector-wise, we favour industrials, healthcare, banks (selection is critical). We expect industrials to benefit from the next wave of AI capex, which is likely to spread beyond data centres to areas like batteries, electric motors, sensors and drones. As a result, B2B companies like industrials are likely to enjoy stronger revenue growth and higher returns.

EM equities are supported by strong fundamentals, economic growth, and a weakening USD. Uncertainty caused by Trump’s policy in DM is another factor boosting EM equities recently.

We remain positive on Emerging Europe LatAm and UAE.

In Asia, we are positive on India from a structural perspective. But we are monitoring valuations and some companies where a conglomerate discount has been priced in.* In China, where we are neutral, we think the government’s anti-involution policies are unlikely to boost corporate margins in the short term.

Although we are cautious on energy and technology sectors, we are positive on businesses in the memory chips sector, for instance in South Korea.

MULTI-ASSET

Explore the carry potential in EM

Francesco SANDRINI CIO Italy & Global Head of Multi-Asset | John O’TOOLE Global Head - CIO Solutions |

The growth momentum is stronger than expected in the US and Europe, with irregular progress towards the inflation target that could lead the Fed and ECB to stay on hold in the near term. In Japan, PM Sanae Takaichi’s victory gives an additional push to her “Sanaenomics” agenda that could revamp Japan’s growth potential. Elsewhere, EM show improving financial conditions that could improve their economic pattern. In this context, we have recalibrated our stance to explore carry in EM, maintaining a modestly pro-risk stance.

While we remain positive on equities through Europe and UK, we have tactically adopted a neutral stance on the US. Concentration risk in the tech sector remains elevated, and there is rising demand for diversification beyond crowded trades. Secondly, we upgraded Japan due to expectations of strong earnings growth and an improvement in return on equity. We remain constructive on emerging markets in general and specifically on LatAm.

On FI, we have become positive on EM spreads, which should benefit from a risk-on sentiment. Although geopolitical risks persist and valuations are tight, EM spreads are supported by ample liquidity, positive macro momentum and attractive carry. In DM, we stay positive on EU IG. On govt. bonds, we are overall constructive on the US and EU. But now we prefer to express our view on the EU through German bunds, rather than EMU swaps. Bund valuations vs swaps are attractive and should gain from potential dovishness from the ECB and provide a safeguard in a risk-off scenario. We also remain positive on Italian BTPs.

We turned positive on a basket of EM FX (TRY, BRL, HUF etc. against the USD), as it provides a diversified EM exposure and should benefit from positive EM growth and a weaker dollar. In commodities, we are constructive on gold, but cautious on oil. In addition, owing to the recent equities rally and persistent geopolitical risks, we think it’s essential to strengthen safeguards, particularly on US equities.

We aim to diversify and explore markets that stand to benefit from a supportive macro backdrop, attractive structural growth prospects, and earnings potential.

VIEWS

Amundi views by asset classes

Definitions & Abbreviations

Currency abbreviations: USD – US dollar, BRL – Brazilian real, JPY – Japanese yen, GBP – British pound sterling, EUR – Euro, CAD – Canadian dollar, SEK – Swedish krona, NOK – Norwegian krone, CHF – Swiss Franc, NZD – New Zealand dollar, AUD – Australian dollar, CNY – Chinese Renminbi, CLP – Chilean Peso, MXN – Mexican Peso, IDR – Indonesian Rupiah, RUB – Russian Ruble, ZAR – South African Rand, TRY – Turkish lira, KRW – South Korean Won, THB – Thai Baht, HUF – Hungarian Forint.

Authors