Summary

While markets are rightly focusing on price pressures in the US, the impact on consumption should not be underestimated. The Fed would prefer to manage this double whammy by keeping inflation expectations anchored and by refraining from rate hikes if the economic outlook deteriorates.

- US input price inflation accelerated in April, coming in significantly above market expectations.

- Bond yields, particularly short-dated ones, are moving higher owing to higher near-term inflation expectations. Additionally, a recent auction of 30-year USTs was completed at yields close to 5%, for the first time since 2007.

We think the Fed would like to balance the need to control inflation with any potential fragilities in the economy.

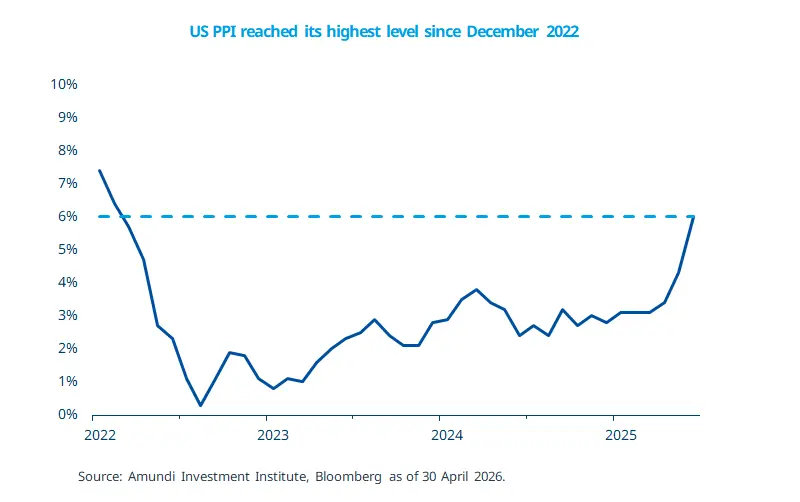

US PPI, a measure of inflation at the producer level, rose to 6% year on year in April, the highest since December 2022 and well above market expectations. Energy price inflation also rose sharply since March. The data suggest that the war in the Middle East is beginning to feed into the real economy through higher input costs for companies, raising the risk that these costs may be passed on to consumers. In markets, 2-year Treasury yields, which are highly sensitive to inflation and monetary policy expectations, have moved above 4.0% — their highest level since June 2025 — on concerns about price pressures. We believe the key driver will be how long energy prices remain elevated, which in turn depends on the duration of the conflict and disruptions through the Strait of Hormuz. On monetary policy, we expect the Fed to remain in wait-and-see mode this year, although some FOMC members are becoming alert to inflation risks. While we believe the new Fed Chair, Kevin Warsh, may take a reasonably balanced, wait-and-see approach, we are monitoring any potential political pressure on the central bank.

This week at a glance

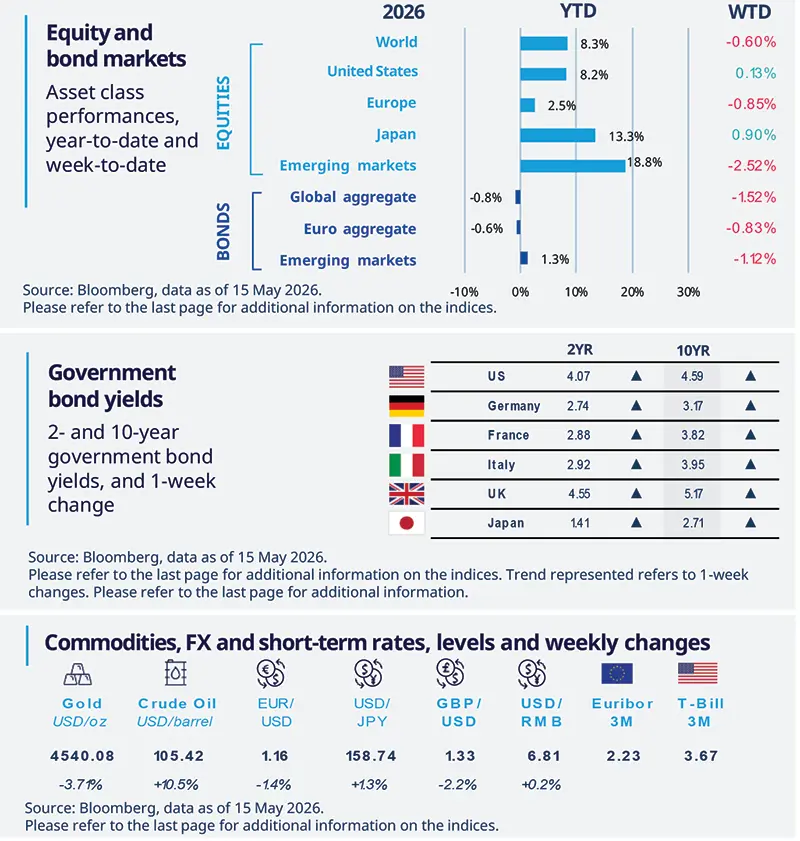

Global stocks were mixed over the week, weighed down by higher oil prices and rising yields. The S&P 500 touched new all-time highs but lost some momentum towards the end of the week. Meanwhile, US yields climbed to their highest levels since mid-2025, mainly following the release of the PPI report. In FX, the dollar confirmed its strength amid a repricing of the Fed’s policy path. Oil extended its gains, given the lack of progress on the reopening of the Strait of Hormuz.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 15 May 2026. The chart shows the price of gold.

* Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US price pressures increased

April inflation rose sharply to 3.8% YoY, with core inflation, excluding food and energy, increasing to 2.8%, The increase was driven by a one-off catch-up in shelter and strength in food and energy costs. Tariff-exposed categories such as apparel showed easing pressures, suggesting that tariff-related inflation may have peaked. Energy cost pass-through also remained visible, particularly in airfares and lodging, while inflation in AI-related tech goods accelerated. Given the uneven pace of disinflation, Fed rate cuts are likely to be delayed, with no cuts expected this year unless clearer disinflation signals emerge.

Europe

Eurozone outlook weakened by the energy shock

Eurozone data were mixed. GDP growth in Q1 was confirmed at a modest +0.1% QoQ, while employment rose slightly. Additionally, industrial production edged up by +0.2% MoM in March, showing resilience despite rising energy prices and geopolitical tensions. Early effects from the energy shock have been limited, partly due to pre-emptive demand ahead of price hikes. However, productivity growth stalled, and the outlook points to slower GDP growth in Q2 and Q3. Prolonged energy supply disruptions would increase the risk of stagnating growth.

Asia

India inflation softens, but pressures remain ahead

India’s April inflation surprised on the downside at 3.5% YoY, mainly due to softer-than-expected food inflation. However, the government raised petrol and diesel prices effective from 15 May, marking the first increase in pump prices since April 2022. The hike is relatively modest and only partially offsets elevated input costs for state-owned energy companies. Looking ahead, inflation is expected to gradually edge higher over the rest of the year as fuel pass-through and other cost pressures gradually feed through into prices.

Key dates

Japan GDP 1Q, UK unemployment rate, South Africa CPI |

Eurozone CPI. UK CPI and PPI, FOMC Minutes |

Japan CPI, Germany IFO, US University of Michigan Consumer confidence |

Authors