Summary

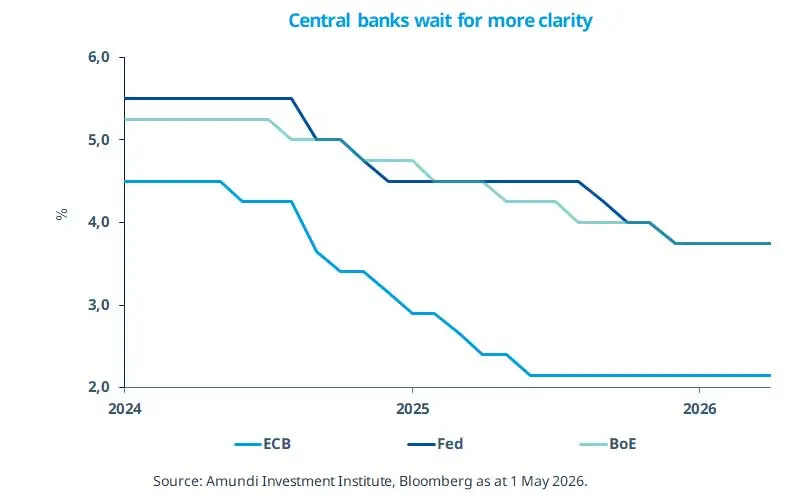

Global central banks are assessing the extent of the stagflationary shock. They want to keep market and consumer inflation expectations in check, while also retaining the flexibility to respond to any shock to growth and consumption. This is what we call disciplined optionality.

- The energy shock is large enough to change the policy backdrop, but it is not yet clear enough to justify an immediate response in the form of a rate cut or a hike.

- Although oil and gas prices remain close to the ECB’s March baseline, they are still above pre-war levels.

- Thus, central banks including the ECB, will need to proceed cautiously with monetary policy in the current uncertain environment.

Major central banks (the Fed, ECB and BoE) kept interest rates unchanged in April, in line with our expectations. We believe central banks are buying time and assessing the impact of this supply shock from the war in the Middle East on broader inflation across the economy, corporate margins, wages and consumption. At the Fed, the fact that three governors opposed maintaining an ‘easing bias’ in the policy statement is evidence of how inflation concerns are becoming increasingly important at the central bank. However, we think the Fed is in observing mode and, looking ahead, would remain tilted towards a relatively dovish stance. The previous fairly balanced comments from Kevin Warsh, who will most likely be appointed as the next Fed Chair, also suggest that. But assessing the conflict’s impact on inflation calls for greater patience in the near term. We expect the next move to be a rate cut in early 2027. Even for the ECB and the BoE, we continue to advocate greater patience and believe they would stay on hold this year.

This week at a glance

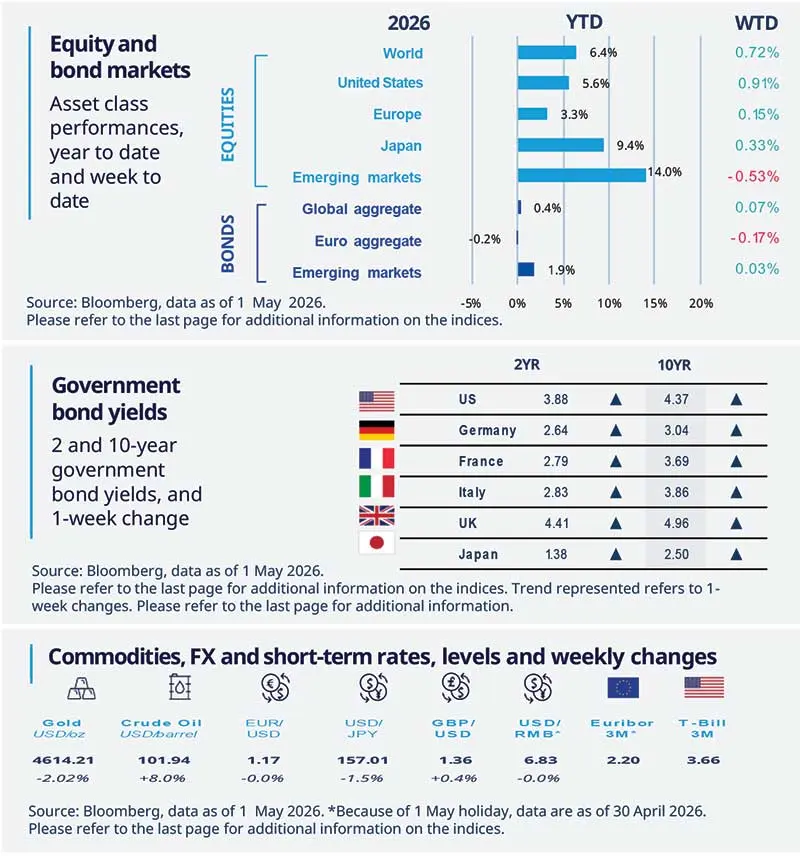

Oil price briefly touched its highest level in almost four years as the US-Iran standoff raised fears of a prolonged supply shock. Global equities were supported by strong earnings from mega-cap tech companies, despite growing concern about the Middle East conflict. Bond yields continued to rise amid cautious central banks and inflation fears. The dollar remained unchanged (against the euro), while gold fell.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 1 May 2026. The chart shows the price of gold.

* Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US capital expenditure supporting growth

US durable goods rose by 0.8% MoM in March. The core index, which excludes aircraft orders and is a proxy for investment in equipment, jumped by an even bigger margin. The improvement was broad based, from communication equipment to machinery and fabricated metals orders, which reached record levels, as well as motor vehicles. Overall, capital expenditure continues to provide strong support to GDP growth, not only in tech-related areas, helped also by the tax cuts under the OBBBA (One Big Beautiful Bill Act).

Europe

Eurozone credit conditions are tightening

The ECB’s bank lending for Q1 2026 reported a tightening in credit supply. For corporate, the tightening was most pronounced since the third quarter of 2023, while demand saw a slight decline following three consecutive quarters of improvement. Banks also reported a small tightening for housing loans, after two quarters of modest easing. Overall, the expectations component points to a greater risk of further tightening in the next survey.

Asia

China PMI came in above expectations

April’s manufacturing PMI held up better than expected, edging down only marginally to 50.3 (compared with 50.4 in March) despite the prolonged conflict in the Middle East. Notably, export orders rose above 50 for the first time since May 2024, reflecting the relative strength of China’s export sector amid a global supply shock. This contrasts with the notable softening in services and construction PMIs, suggesting that the divergence between domestic and external demand is likely to persist.

Key dates

Indonesia and Turkey Inflation, Eurozone Manufacturing PMI |

US Productivity and Unit Labor Costs, Mexico policy rate |

Japan Labour earnings, US Non-farm Payroll, University of Michigan Consumer confidence |

Authors