Summary

The stagflationary impulse from the conflict will reshape the growth and inflation risk trade-off, creating a policy dilemma for central banks globally. Overall, we expect central banks to postpone easing, but not to reverse it, a wait-and-see stance seems plausible and appropriate.

- The major DM central banks – Fed, ECB, BoE and BoJ - have left rates unchanged, in line with our expectations.

- The Fed and ECB governors’ comments emphasized the importance of taking a “wait and see” approach.

- Bond-market movements have been significant: investors are now pricing in hikes for the ECB and the BoE, and no cuts for the Fed in 2026.

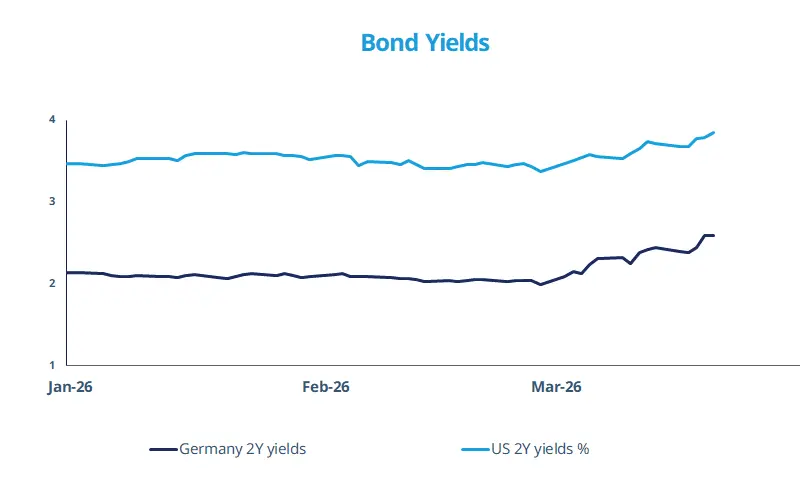

Major central banks including, the Fed, the ECB and Bank of England held their policy rates unchanged in a week that saw escalation in the Middle East conflict. The conflict is also pushing up bond yields, as shown in the chart. While we believe the impact on inflation (from the crisis) will be slightly more pronounced in Europe, the common theme across central banks is that of keeping a ‘wait and see’ approach. This is because the duration for which energy prices stay high (and the crisis persists) could be the key factor for assessing the price pressures in the economy.

For the ECB, Christine Lagarde reassured that the bank is well positioned and equipped to deal with the war shock but she stressed that it is too early to draw firm conclusions about the economic impact of the Middle East conflict. Markets have also changed their expectations for rate cuts by central banks. We expect policy rates to remain largely stable in the very near term.

This week at a glance

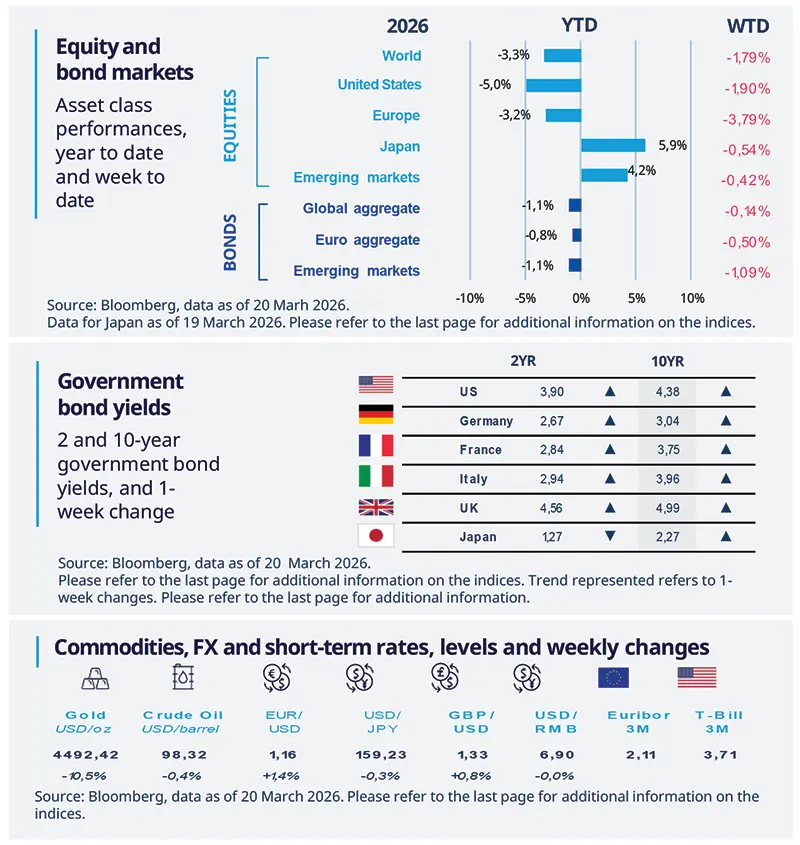

Global equities fell for a third consecutive week as tensions escalated in the Middle East. Investors in bond markets have rushed to price in higher interest rates amid a jump in energy prices and hawkish rhetoric from central banks. Diminished prospects of near-term US rate cuts have put downward pressure on gold.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 20 March 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

Increasing input costs in the US

The PPI Index increased more than expected in February (0.7% MoM). This dynamic, especially in processed goods and services, suggests that inflationary pressures from greater input costs were already intensifying before the spike in oil prices linked to the Iran conflict. Although the US remains relatively more insulated from the energy shock than other countries, the ongoing rise in energy prices and tariff-related costs might further strain the economy.

Europe

Eurozone sticky price pressures

Eurozone inflation accelerated to 1.9% YoY in February, led by transport and hospitality. Core inflation confirmed at 2.4% while services inflation increased at 3.4%, signaling domestic cost pressures. Rising oil and gas should lift headline inflation in coming months and may feed into core inflation with a lag if the Middle East conflict extends beyond the near term. Recent commodity moves are less likely to spark the same effects on wages and core inflation as was the case during the pandemic.

Asia

South Korea’s multi-layered response to crisis

South Korea’s heavy dependence on Middle Eastern energy imports has led to multiple support measures. Following the introduction of a fuel price cap and export restrictions on refined oil products, the government is preparing a supplementary budget to compensate refiners and support households and businesses. At the same time, authorities are discussing an expansion of the market stabilization backstop to prevent liquidity stress.

Key dates

Japan CPI, EZ PMI |

UK CPI and PPI, Germany IFO, US Import and Export prices |

EA CPI expectations, US University of Michigan Consumer Confidence |

Authors