Summary

The conflict in the Middle East is denting sentiment in Europe. We think the economic — and more specifically the inflation — outlook depends on how long oil and gas prices remain elevated and on whether those price effects spill over into other parts of the economy.

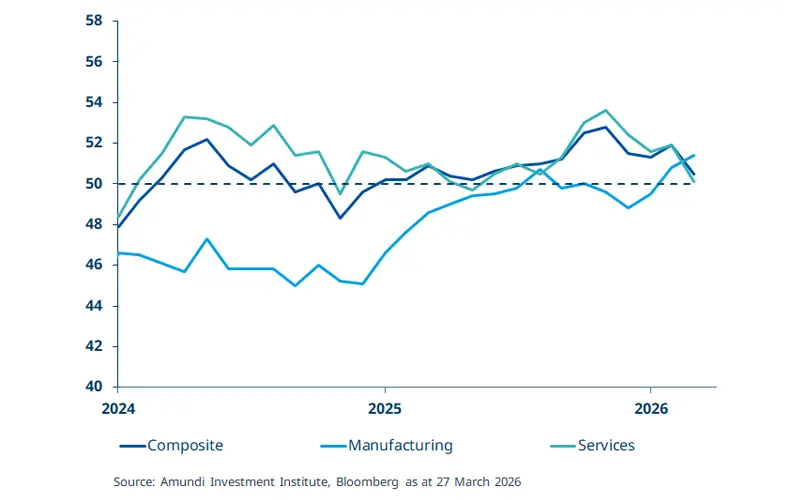

The Eurozone March PMI survey fell during the previous month, indicating businesses are getting worried about the Middle East conflict.

The composite PMI remained above the 50 expansion threshold, but it was the lowest in the past ten months.

Robust household savings, combined with new policy measures, should help cushion the economic impact across Europe.

The preliminary composite Eurozone PMI (50.5) signalled a deceleration in economic activity in March. While the reading remains above the 50 threshold, it is the lowest since May 2025. Specifically, the manufacturing component rose, while the services component declined from February’s level. We believe businesses are pricing in some of the risks posed by the Middle East conflict: higher inflation, disrupted energy supplies and growth concerns. Looking ahead, we believe the crisis is likely to add stagflationary pressure to the economy through higher energy prices. If oil and gas prices remain elevated for a prolonged period, we may see inflation seep into other parts of the economy. As a result, the ECB’s task will become more complicated as the central bank tries to balance inflationary pressures with a nascent economic recovery. We expect the ECB to pause in the near term before making any further policy decisions.

This week at a glance

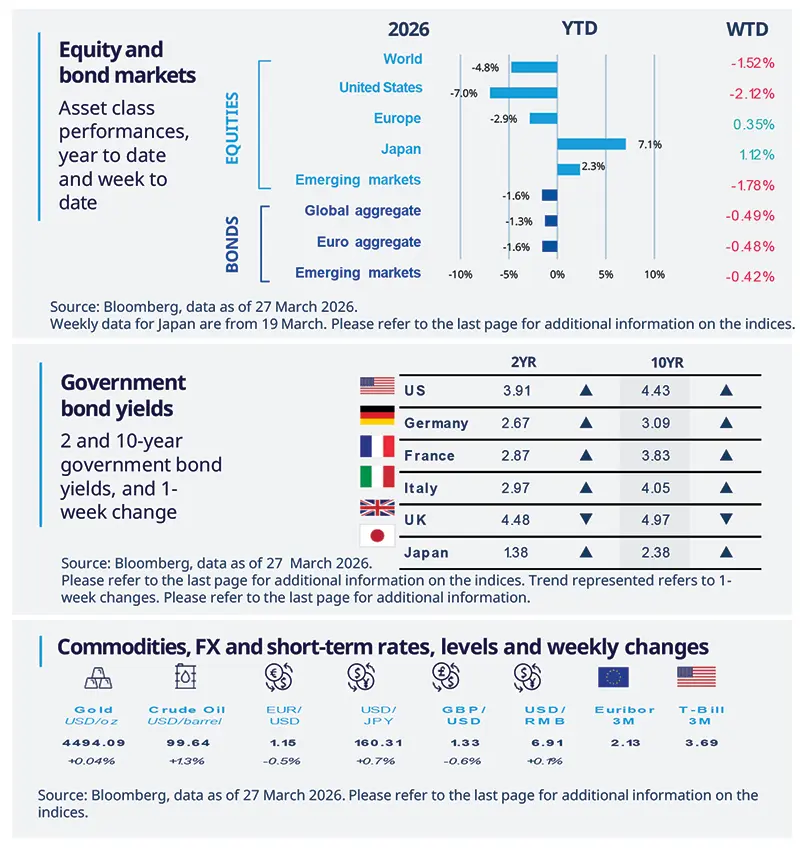

Global equities headed for further weekly losses as traders grew more nervous about a protracted war in the Middle East, with Japan being an exception. Global bond markets rallied early in the week on hopes of US-Iran negotiations, but yields rose eventually amid renewed threats. Oil prices rose over the week.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 27 March 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

Mixed signals from US labor market

Recent data on initial jobless claims showed a slight rise while continuing claims fell, indicating fewer people remain unemployed over time. Both measures are noticeably lower than in 2025, suggesting layoffs remain limited nationally or concentrated in a few sectors. In a labour market with low hiring and low firing, reduced labour turnover should help moderate wage growth and limit second‑round effects of the energy price crisis.

Europe

Price concerns in the EU

In March, surveys in Germany showed higher price plans (especially in manufacturing) and moderating consumer expectations. In France, they indicated a stable business climate but weaker consumer confidence and higher expected prices. In Italy, surveys showed steady business sentiment but rising price expectations in manufacturing and retail and a marked fall in consumer confidence. The signals of growing price pressures among consumers and mixed business sentiment complicate the ECB’s response.

Asia

Japan base-pay increase

Japan’s first‑round wage negotiations showed a 3.85% YoY base‑pay rise, with data for small and medium enterprises up 3.54%. The final outcome will likely ease to around 3.7%. With base pay above 3.5%, total nominal wages should climb about 2.5–3% in FY26, allowing real pay to turn positive relative to 2.4% inflation. Middle East tensions and higher oil could complicate the recovery.

Key dates

Europe Confidence, India and South Korea Industrial Production, Brazil CPI |

EA CPI, Japan CPI, US Consumer confidence, JOLTS data; China Manufacturing PMI |

US Nonfarm Payrolls, Turkey CPI |

Authors