Summary

The market response to the Middle East crisis has been driven chiefly by concerns about inflation. This episode reaffirms our view that investors should remain diversified and maintain multiple layers of resilience and quality within portfolios.

The crisis will likely accelerate Europe’s shift to strategic autonomy and greener energy to reduce geopolitical risk.

With inflation risk on the rise, central banks will likely become more cautious and embrace a wait-and-see approach.

The need to stay vigilant and well-diversified is high, and investors should look beyond the crisis for areas of quality through careful selection.

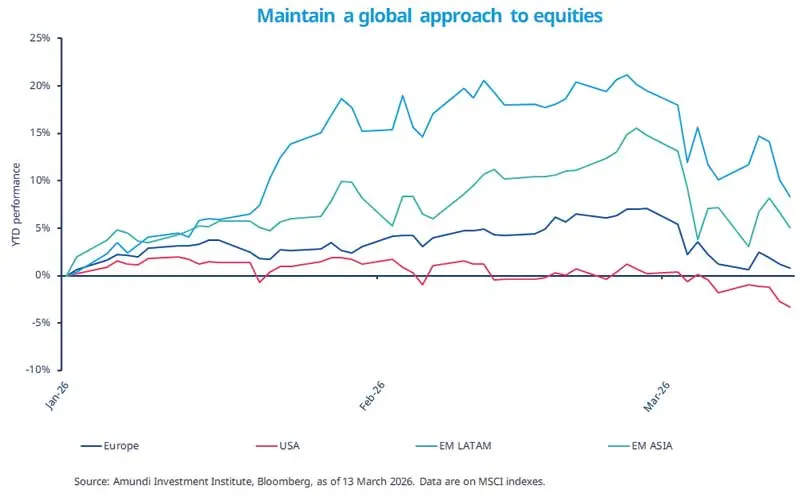

The impact of the Middle East crisis on equities across regions reflects economies’ sensitivity to higher energy prices and renewed concerns about inflation. In some cases, it represents a pull‑back in markets that have performed strongly this year. While US assets (including the dollar) have been more resilient during this episode, vulnerabilities associated with expensive AI segments and a large US fiscal deficit remain. In contrast, EM Asia and European markets declined sharply, given those regions’ dependence on energy imports. Despite this volatility, these markets have outperformed year‑to‑date, and LatAm has been a top performer.

These movements affirm the need to maintain a global diversified stance across both developed and emerging markets, as it provides multiple layers of resilience for long-term returns. A key factor is the scale and the duration of disruption in the Strait of Hormuz.

This week at a glance

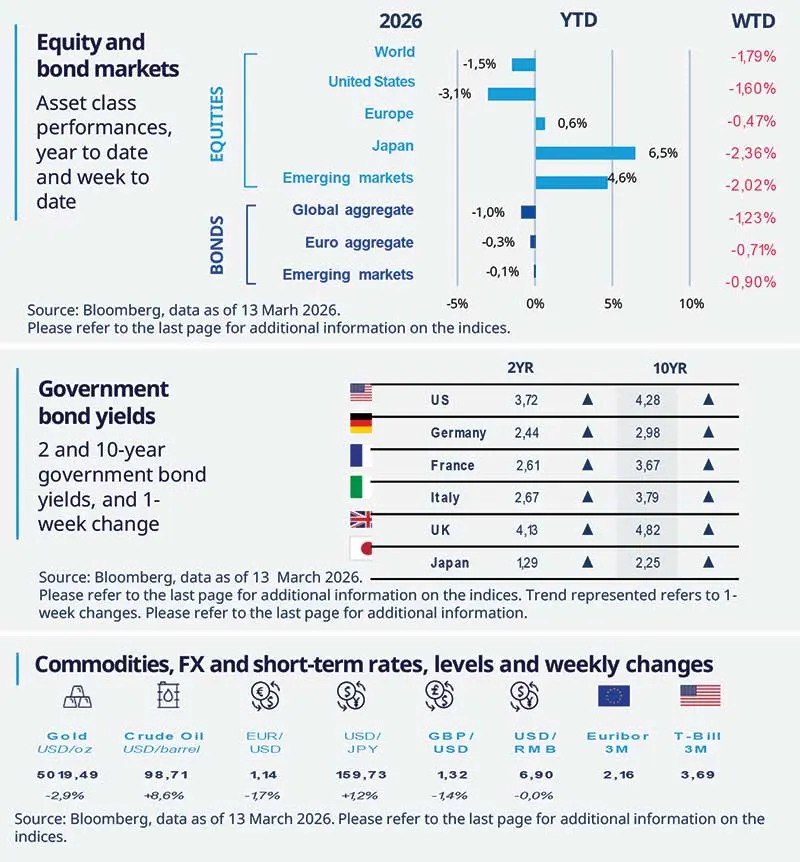

Equity markets fell, particularly in Asia, as investors remained concerned about tight energy supply and its impact on inflation. Consequently, bond yields rose as investors reduced expectations that the Fed and other central banks would cut rates. Oil extended its gains to the highest close since August 2022 amid wide intraday swings, while gold fell for the second consecutive week.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 13 March 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US services inflation pressures eased

Headline CPI remained at 2.4% (year-on-year) in February, whereas core inflation (CPI excluding food and energy prices) was relatively benign, led by the easing of services inflation. Core goods inflation also remained muted. This report shows no impact yet from US-Iran tensions; however, looking ahead, rising oil prices amid geopolitical risks could accelerate inflation momentum in March and early Q2.

Europe

Germany’s energy-intensive industries weakened

German industrial production fell 0.5% MoM in January, driven by sharp declines in energy-intensive sectors – losses that could continue amid the Middle East conflict. Orders plunged by over 10% following some positive data for the past few months. This clouds the near-term outlook. Overall, persistent weakness in energy-intensive industries highlights vulnerability amid ongoing geopolitical tensions and pressure on energy prices.

Asia

Asia’s response to the energy crisis

The Iran crisis has triggered a sharp rise in global energy prices, weighing on Asia’s growth prospects and pushing up inflation expectations. Policymakers in the region have responded with targeted measures - fuel subsidies, energy rationing and export restrictions on refined petroleum products. The disruption has begun to spread along supply chains, prompting some companies — for example, petrochemical producers — to scale back operations and raising concerns on electronics and semiconductor manufacturing.

Key dates

Germany ZEW, China Industrial Production and Retail Sales |

FED interest rates decision, USA PPI index, EA CPI, South Africa CPI |

ECB rate decision, Japan Industrial Production |

Authors