Summary

Markets are shifting from expectations of a quick resolution to a renewed crisis escalation, with the Strait of Hormuz still disrupted and inflation and growth risks in focus. In this environment, we favour long-term convictions, exploring areas with strong earnings and fundamentals.

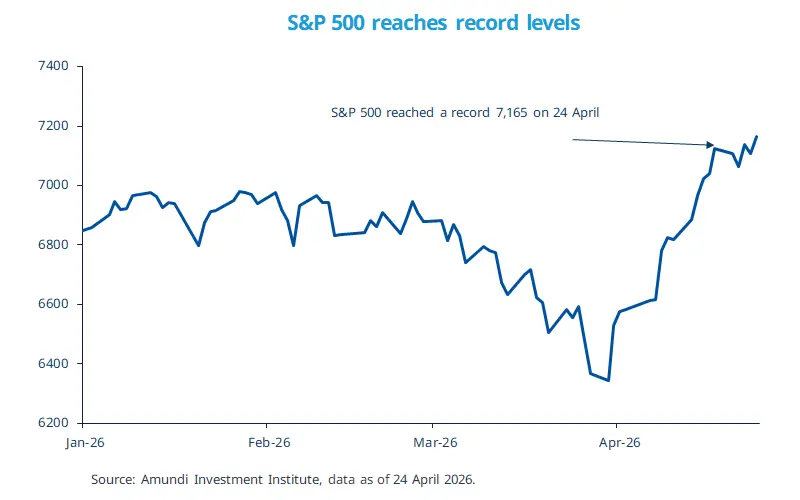

The S&P 500 hit an all-time high this week, with the longest-ever advance in semiconductors.

The S&P 500 companies reporting first-quarter results have beaten estimates so far, providing a fundamental backstop to the market.

The Tech and AI theme is gaining traction in the US, while strategic autonomy supports Europe and demand for natural resources favours Latin America.

US stocks climbed to a new record this week, supported by several factors. Firstly, as investors look for a swift resolution of the Iran crisis, strong corporate earnings boosted confidence, with 80% of S&P 500 companies that have reported first-quarter results having beaten estimates so far. At sectoral level, technology has regained leadership, with the Philadelphia Semiconductor Index posting a notably strong performance. This has reinforced optimism around the sector’s growth and, more generally, around the AI theme.

Secondly, the broader theme of energy independence continues to support sentiment around US domestic growth and strategic security, given the ongoing uncertainty over the resolution of the Iran crisis. Thirdly, the market has also benefited from signs of economic resilience, including positive signals from consumer spending.

Beyond the US, we see opportunities particularly in Europe, Japan, and Latin America.

This week at a glance

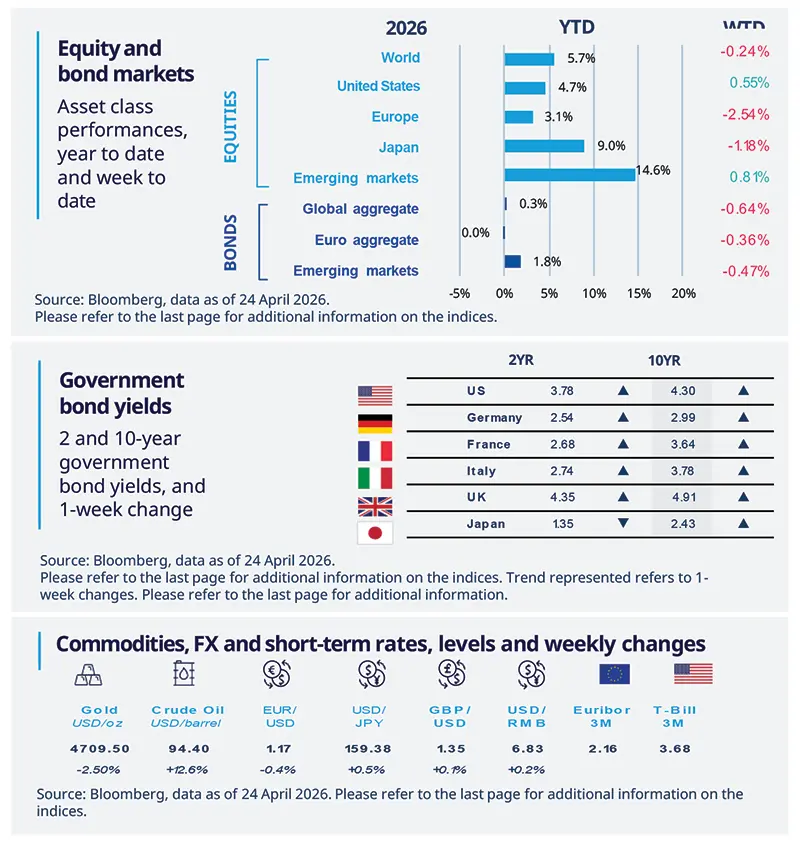

Equity markets were mixed over the week, due to increased uncertainty over negotiations between the US and Iran, with US and EM moving higher. The Strait of Hormuz remained largely closed. The standoff pushed oil prices higher, reviving inflation concerns and triggering an upward push in most bond yields. Gold prices declined.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 24 April 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US consumer spending is growing slowly

Retail sales jumped 1.7% MoM in March, mainly driven by higher gasoline prices. Adjusted for inflation, the index slipped slightly as consumers remain cautious on gasoline and auto components. Excluding these two components, core retail sales increased in both nominal and real terms, led by furniture and electronics. Restaurant sales were modest, pointing to softer service spending and some discretionary saving. Overall, the report suggests real consumer spending expanded modestly in Q1, slowing but still supported by employment and tax refunds.

Europe

Eurozone consumer sentiment weakens

Confidence in the EU and the Eurozone continued to deteriorate in March, falling to -19.4 and -20.6 respectively. Both readings remain well below their long-term averages and are at their lowest levels since late 2022. While real services sales in France suggest modest growth for Q1 and support the view of positive, albeit subdued, growth, the broader backdrop remains cautious, with consumers in the Netherlands and Belgium also becoming less optimistic. Overall, consumer confidence took another hit as geopolitics continues to weigh on sentiment.

Asia

The Philippine central bank in a tightening mode

The Central Bank of the Philippines raised its policy rate by 25 bps to 4.5%. The pre-emptive move is likely to be followed by further tightening, as inflation in March came in above target at 4.1%, up from 2.4% in February. While most central banks globally have adopted a wait-and-see approach, this move suggests that EM central banks may be among the first to embark on a new cycle of rate hikes.

Key dates

BoJ policy rate decision, ECB inflation expectations, US consumer confidence |

Fed policy rate decision, Brazil policy rate decision |

China PMI, Eurozone GDP Q1 and Inflation, BoE and BCE policy rate decisions, US GDP Q1 |

Authors