Summary

So far, 2026 has been characterised by an acceleration towards a geopolitical ‘controlled disorder’, underscoring the importance of diversification. Inflation has returned to the near-term agenda, prompting central banks to assess the situation and adopt a wait-and-see stance.

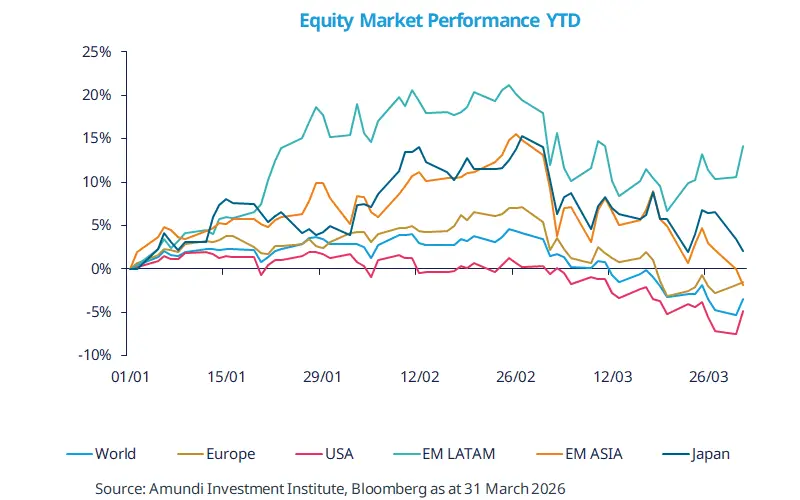

The Iran crisis has triggered a repricing in equities, with most regions coming under stress - US more so than others, year to date.

Long-term, the rotation towards Europe, Japan and EM may play out in different phases and could be affected by how long energy prices remain elevated.

In our view, adding multiple layers of diversification*, seeking returns across the asset class spectrum and maintaining safeguards in place may support a more resilient portfolio.

The year-to-date has been characterised by a series of geopolitical events. While markets largely shrugged off the US military action in Venezuela, the war in the Middle East triggered a sharp rise in energy prices, with knock-on effects across global markets. Consequently, equities declined worldwide, and bond yields rose. Markets are pricing in aggressive central bank actions, as they are overly concerned about inflation, whereas growth worries are on the backburner at the moment. We agree only partially with the markets but believe growth may be affected if prices stay high for a long period.

The impact of the crisis on equities was not uniform. Energy-importing countries and those that had performed strongly before the start of the war were more affected. Despite this heightened uncertainty, year-to-date performance in selected emerging markets — particularly Latin America — and Europe has been better than in the US. Looking ahead, this crisis reinforces our view that diversification* across regions such as emerging markets, Japan and Europe is key to long-term resilience.

* Diversification does not guarantee a profit or protect against a loss

This week at a glance

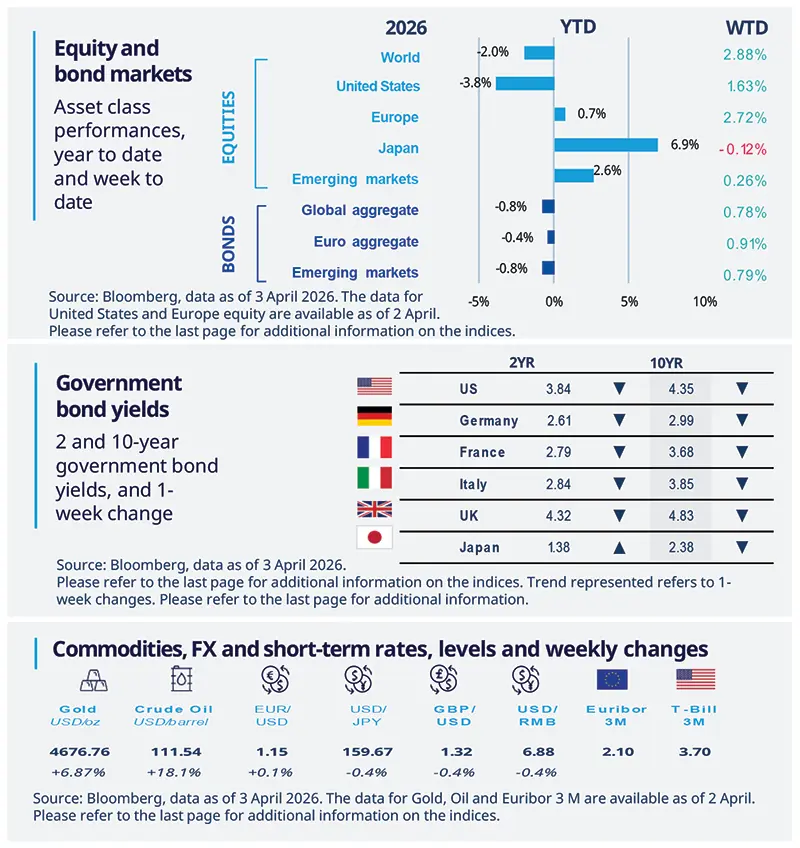

Markets closed out an undeniably volatile week in positive territory. US President Trump dashed hopes initially and then built optimism around a resolution of the Iran crisis, leading to a relief rally that drove the markets higher. Global yields declined, whereas gold and oil prices rose.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 3 April 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US labour market in a ‘low hiring and firing’ phase

The latest US labour market report for February highlighted a sharp fall in the hiring rate, which had been flat and subdued for two years, alongside a decline in job openings. The data suggest somewhat softer labour demand at the start of 2026. Meanwhile, layoffs remain low and stable, pointing to a soft, "low-hire, low-fire" labour market rather than a sharp deterioration.

Europe

Eurozone inflation jumped in March

EZ inflation rose to 2.5% YoY in March, from 1.9% in February, driven mainly by energy inflation, whereas food inflation eased slightly and core inflation remained unchanged at 2.3%. Looking ahead, energy prices are likely to keep pushing CPI higher, with oil and gas-related waves potentially followed by another food-related wave. However, we expect spillovers into other inflation components and wages to remain limited, while weaker economic activity should partly offset inflationary pressures.

Asia

Asia business confidence softened

March manufacturing PMI data show that activity is still expanding in many economies, but growth slowed from February as new orders and output eased. Rising costs and weaker supply conditions were a common theme, driven by higher oil, fuel and raw-material prices, as well as longer supplier lead times amid the Middle East conflict. Looking ahead, firms have become more cautious on hiring, purchasing and restocking. Overall, growth remains positive but less synchronised, while cost pressures and supply-chain strains are increasingly shaping the outlook.

Key dates

USA ISM service, EA PMI. |

EA Retail sales, US Fed Meeting Minutes. |

US PCE Index, Jobless Claims, GDP 4T. |

Authors