Summary

Ongoing conflict lifts inflation expectations

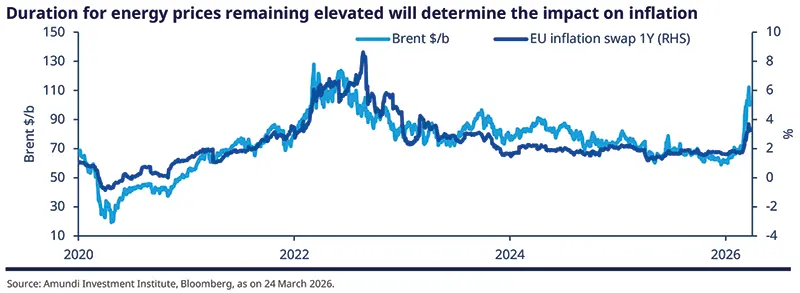

With the Middle East conflict now entering its second month, high energy prices have produced knock-on effects across global financial markets. The US and European breakeven curves surged as markets repriced inflation expectations and the likelihood of central-bank rate cuts. Nominal yields, particularly at the short end, also rose sharply in countries including the UK. At this stage, some of this reaction seems excessive to us. We think the length of time that energy prices remain high will determine the second‑round inflationary effects.

On the growth front, markets do not appear overly concerned at present. We believe persistently high energy prices would weigh on consumption and growth. Overall, this crisis is generating stagflationary pressures across the global economy. Our main convictions are outlined below:

The impact on inflation will vary across regions, with the eurozone (EZ) likely to be more affected than the US. Whether inflation is transitory depends on how long prices for oil, gas, food and fertiliser remain elevated. Eurozone CPI could spike substantially above the ECB’s target in 2026 before subsiding the following year — albeit still above target. This would occur if inflationary pressures become embedded across the economy, for example in intermediate goods, freight and insurance costs. In the US, we expect high energy prices to hit lower‑income households harder.

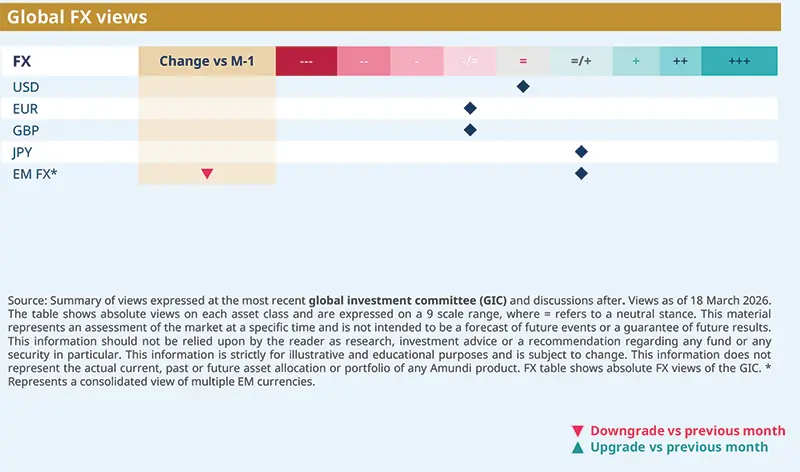

US-dollar strength is back in focus — Although the dollar may be resilient in the near term because of its safe‑haven characteristics, we expect the longer‑term secular weakening to continue. Structural headwinds against the dollar persist, including strains on US public finances, geopolitically driven shifts in global capital flows, and comparatively attractive yields outside the US.

Markets overestimate the crisis’s inflationary impact and underestimate its growth hit; they are not pricing in the risk of weakening consumption compressing corporate margins.

For us to see a sustained US‑dollar appreciation, headline inflation would need to feed through to core inflation and inflation expectations would have to rise sufficiently to compel the Fed to embark on a hiking cycle — a game‑changer that is not our base case.

European and emerging-market countries reliant on energy imports from the Gulf are seeking to stay out of the conflict — EU and UK leaders have declined calls from US President Trump to participate in the fighting. In Asia, India and China are reliant on energy imports and have, so far, successfully sought to negotiate safe passage for ships with Iran. As a net oil importer, India is vulnerable to high prices; one risk is that the government may be forced to divert resources from productive capital expenditure to energy subsidies.

Overall, we believe EM growth will remain robust and see no secular reason for this to change. Fiscal and macroeconomic metrics in emerging markets are improving — macroeconomic orthodoxy has returned to many EMs. In Latin America in particular, this marks the end of a prolonged period of derating. Brazil has significant rare‑earth reserves, and Mexico is benefiting from near‑shoring.

To conclude, we do not see hyperinflation or a global recession. We do expect an impact on inflation and growth; the extent will depend on the duration of the war and how long oil and gas prices remain elevated. For investors, adding multiple layers of diversification — inflation‑linked instruments, government bonds and commodities — is important, not least because correlations between bonds and equities are shifting. We also see a greater need for hedging and tactical risk reduction.

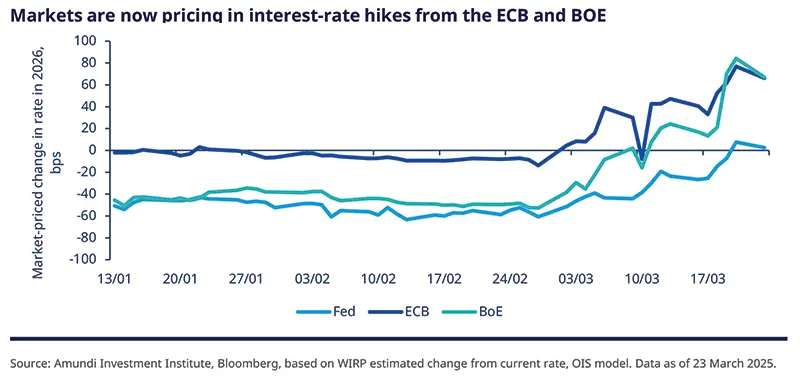

| Amundi Investment Institute: Some major central banks likely to pause this year |

The ECB, the Bank of England (BoE) and the Fed all are expected to keep rates unchanged in 2026. For the ECB, assessing the impact of energy prices on headline and core inflation — and on wages — remains key. Markets are already pricing in hikes. We have removed our projection for an ECB rate cut this year. Additionally, we think that in case of a persistent deviation of inflation from its target and de-anchoring of inflation expectations, the ECB may hike (not our base case for the moment). The Fed’s wait‑and‑see approach is also justified given the rise in inflation expectations, weak US payrolls in February, and stronger‑than‑expected recent PPI data. The Fed’s hold in March was in line with our view, and we now do not expect any cut this year. For the BoE also, we project the bank to remain on hold for 2026. The second‑round effects of inflation — which depend on the duration of supply disruption and the persistence of elevated prices — are a key consideration for the ECB and the BoE. Energy prices depend not only on near‑term physical disruptions to gas and oil supplies but also on any lasting damage to Gulf states' production capacity, which could persist even after the Strait of Hormuz becomes navigable again. The Iranian strike on the Qatari gas plant is an example of a disruption that will affect gas supplies well beyond this year. |

Monica DEFEND

The ECB will not automatically tighten policy in response to higher energy prices; it will wait to assess the shock’s size, persistence and spillovers to broader price pressures before adjusting its policy stance.

As we remain vigilant of the crisis, inflation and monetary policies, we believe in trimming down risks tactically and improving the resilience of portfolios through a diversified stance. Our granular convictions are outlined below:

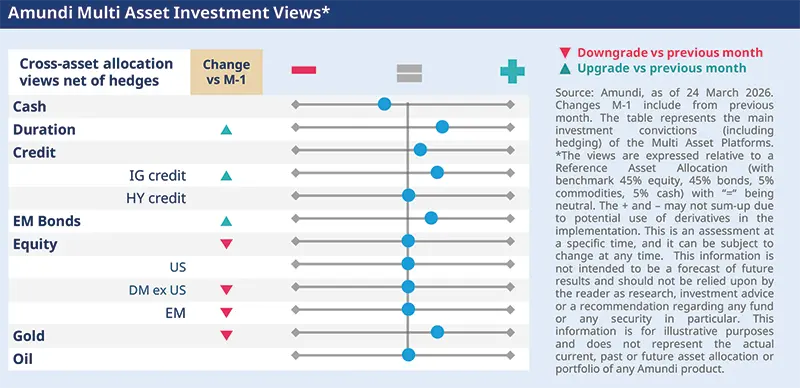

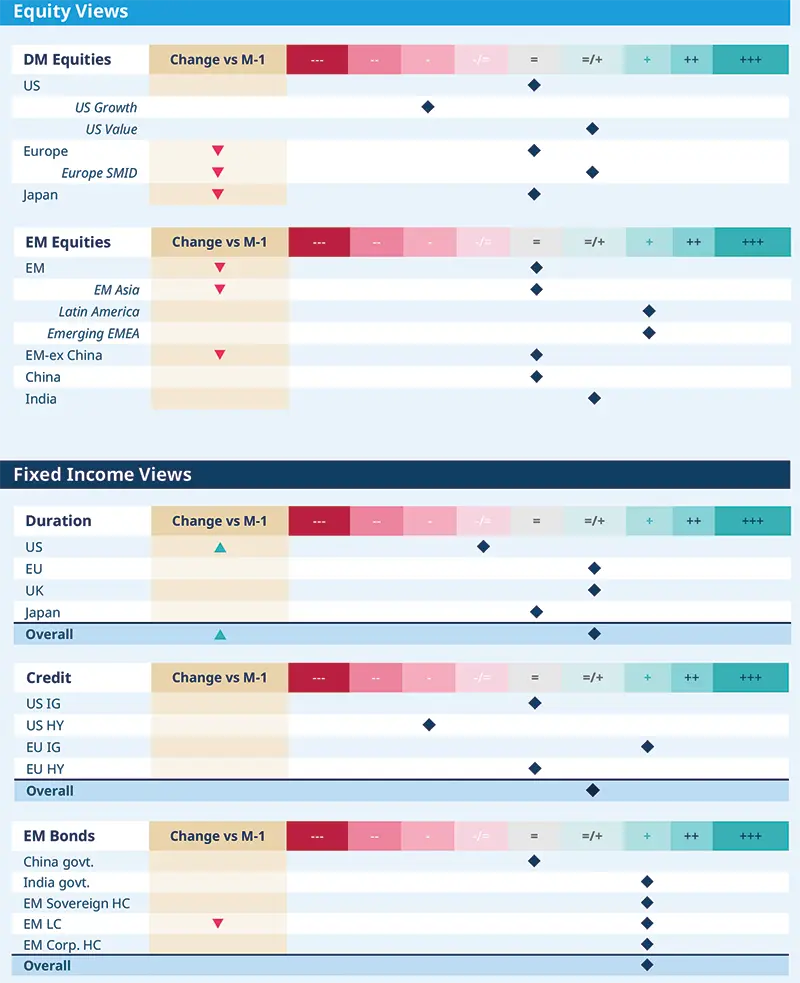

We raised our stance on duration in fixed income and are exploring ways to add resilience through an active approach. At the same time, we maintain a positive stance on corporate credit amid strong fundamentals. We’ve slightly downgraded emerging market local currency bonds but are still constructive due to ongoing robust economic growth and are particularly exploring countries where yields are high.

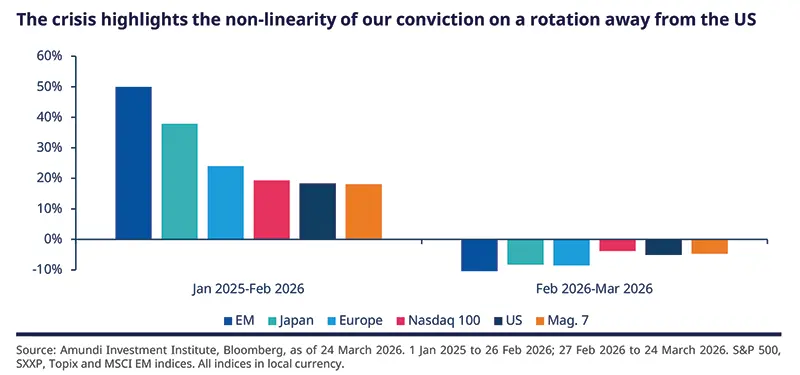

While we agree that near-term volatility has led us to be a bit cautious on some segments of equities, our long-term convictions around Europe, Japan and emerging markets have not changed. The current crisis is an indication that the rotation away from the US into these regions may not be linear, but it will continue over the long term.

From a multi asset perspective, this crisis has been an opportunity for us to adapt and tactically cut down risks in areas such as equities, which are more vulnerable to volatility. That said, we’ve enhanced our views on government bonds and maintained our convictions on corporate credit and emerging market bonds.

We are refraining from taking bold directional bets and avoiding concentrated areas. Instead, we prefer to remain diversified and seek value in government bonds, particularly short‑dated issues.

FIXED INCOME

Active, disciplined duration management

Amaury D’ORSAY |

The inflation story has received greater attention because of high energy prices and supply disruptions. As a result, markets are pricing in rate hikes by the ECB and the BoE. Although we have revised our assessment of monetary policy, we do not currently expect central banks to raise rates. We expect them to pause to await greater clarity on the crisis and on supply disruptions before making any decision.

Hence, this is a time to be flexible, given opposing pressures (on yields) from rising inflation expectations and safehaven demand. On curves, steepening is our central scenario for the medium term, but we acknowledge that this view is now widely shared across the industry and has already advanced significantly. Overall, we favour a selective approach rather than broad‑based exposure.

We have turned slightly positive on duration overall. We are less cautious on US (particularly at the short and long ends) and remain very active.

Our constructive stance is reflected mainly through EU, where we are gradually looking for additional opportunities. We also like peripheral debt for its attractive fundamentals and carry. In the UK where we remain constructive, we see potential in the 2Y part of the curve.

US inflation‑linked bonds remain a good hedge

We maintain a positive view on IG, particularly in Europe, where carry is attractive and balance sheets are strong. In contrast, we are more cautious on HY, where valuations are less compelling and dispersion remains high, reinforcing the need for selectivity.

From a sector perspective, we prefer financials over non-financials and euro spreads over US. Relative value is attractive in Europe.

Constructive and selective on EM debt. We are slightly less positive on LC debt amid high geopolitical risks, although we continue to favour countries where real yields are high, notably Brazil and South Africa.

In EM FX, recent performance echoes past geopolitical episodes, prompting close attention to LatAm elections.

Tactically, the dollar may be resilient. But structural issues in the US remain. Once we are past this crisis, we expect the USD to weaken.

EQUITIES

Focus on areas of long-term resilience

Barry GLAVIN |

Volatility in equities is explained by the Iran conflict, but importantly, some sections that are pulling back are the ones that have performed well so far this year. Now, the key uncertainty is the duration of the conflict. If tensions ease in the coming weeks, oil prices should normalise, and the current volatility may present attractive entry points across sectors. However, estimating the timing of this will be difficult.

So, we are sticking to our long-term convictions but acknowledge the near-term uncertainty in equities. Our aim remains to identify quality businesses with strong balance sheets and minimal earnings impact from the crisis. We are also exploring areas exposed to structural growth themes for instance around German fiscal spending, Japanese corporate reforms, and robust EM growth.

We are focusing away from the US to limit concentration risk. Europe, Japan and EMs remain attractive but are oil‑price sensitive and require vigilance.

In Europe, we favour stocks that can benefit from increased German fiscal spending, and select mid‑caps whose valuations are near historic lows, earnings growth is robust and quality is improving.

Sector‑wise, we favour banks and industrials, which we expect to benefit from the next wave of AI-related capex (e.g., batteries). We also see opportunities among quality construction stocks hit by growth concerns.

We remain positive on Japan given reflation and the corporate reform agenda, and also like UK‑listed global banks and pharmaceutical companies.

EM are attractively priced and growth is resilient. We are assessing whether a prolonged conflict (not our base case) could delay monetary easing (higher energy prices) and dampen consumption.

Secondly, the diversification from DM to EM is still a structural trend, although some short-term adjustments are understandable. We have slightly downgraded EM Asia given the region’s exposure to energy imports. In India, we like select consumer companies. A sustained conflict could push fertiliser and food prices higher.

Finally, as long as AI capex continues, select companies in countries such as South Korea will benefit. We favour memory suppliers owing to a supply–demand imbalance and government “corporate value‑up” measures.

MULTI-ASSET

Tactically cautious, enhanced safeguards

Francesco SANDRINI CIO Italy & Global Head of Multi-Asset | John O’TOOLE Global Head - CIO Solutions |

Recent events in the Middle East have allowed us to take a step back and reassess how our long-term views will play out. We believe the duration for which energy prices stay high will determine the pass-through of this crisis to the economy. While our macro signals are still calling for a late-cycle environment, they do not fully include the impact of a prolonged crisis. Hence, from a near-term perspective, we have reduced our directional views on risk assets. Secondly, we believe there is a need to strengthen hedges, particularly on DM equities. Overall, it is important to stay diversified and acknowledge that some market movements may have been excessive.

In equities, we have turned neutral on DM and EM, with an aim to explore opportunities once volatility declines. In FI, we’ve used the recent volatility in EU credit to upgrade our stance. We have also slightly raised our positive view on EM debt. We think following the surge in energy prices, a section of EM rates was pricing in excessive inflation fears, ie., yields rose substantially. Valuations are now more appealing in a select basket of EM short-term rates but additional FX risks should be avoided. In general, we have trimmed our views on EM FX. We also think the currencies of energy-importing Asian countries could remain subdued, and hence, we prefer the FX of select energy exporters such as Brazil.

On duration, we upgraded our view following the sharp upward move in German bond yields. While the markets expect the ECB to hike rates, we think the central bank’s response will be more muted (no rate hike expectations for this year). German bonds retain their safe-haven status when risk aversion rises. In general, we are positive on US 5Y, EU rates and long BTP versus Bund, but we are cautious on JGBs. Finally, in commodities, the strong movement in gold recently has allowed us to reduce our constructive stance, even though we believe risks related to debt sustainability, deficits and geopolitics are still in place. In DM FX, we are cautious on the dollar over the long term.

We remain active about exploring opportunities if weakness persists — but are unlikely to make bold directional bets, while the Iran conflict remains the dominant risk.

VIEWS

Amundi views by asset classes

Definitions & Abbreviations

Currency abbreviations: USD – US dollar, BRL – Brazilian real, JPY – Japanese yen, GBP – British pound sterling, EUR – Euro, CAD – Canadian dollar, SEK – Swedish krona, NOK – Norwegian krone, CHF – Swiss Franc, NZD – New Zealand dollar, AUD – Australian dollar, CNY – Chinese Renminbi, CLP – Chilean Peso, MXN – Mexican Peso, IDR – Indonesian Rupiah, RUB – Russian Ruble, ZAR – South African Rand, TRY – Turkish lira, KRW – South Korean Won, THB – Thai Baht, HUF – Hungarian Forint.

Authors