Summary

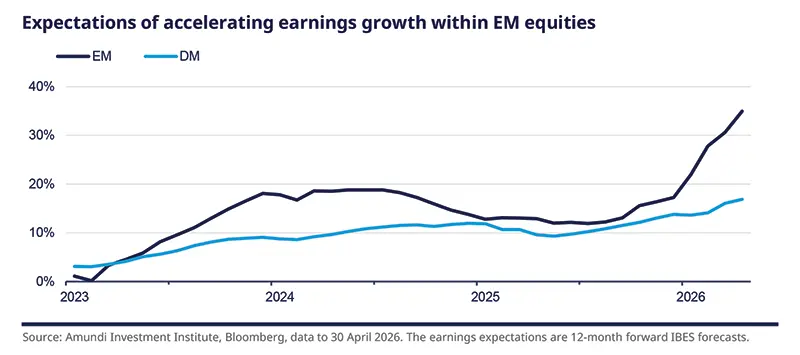

EM equities have climbed to new highs despite the ongoing conflict in the Middle East. The main vulnerability lies in energy: further disruption to the Strait of Hormuz, a key oil and gas transit route, would lift energy prices and worsen inflation. A sustained shock would also complicate fiscal policy, especially in countries with limited buffers. Yet, despite uncertainty over how long energy flows could be affected, EM equities have remained resilient, supported by regional dispersion, the tech rally and earnings growth, which is expected to accelerate well above that of developed markets.

EM equities: strong earnings growth, a robust tech cycle and better positioned for stress

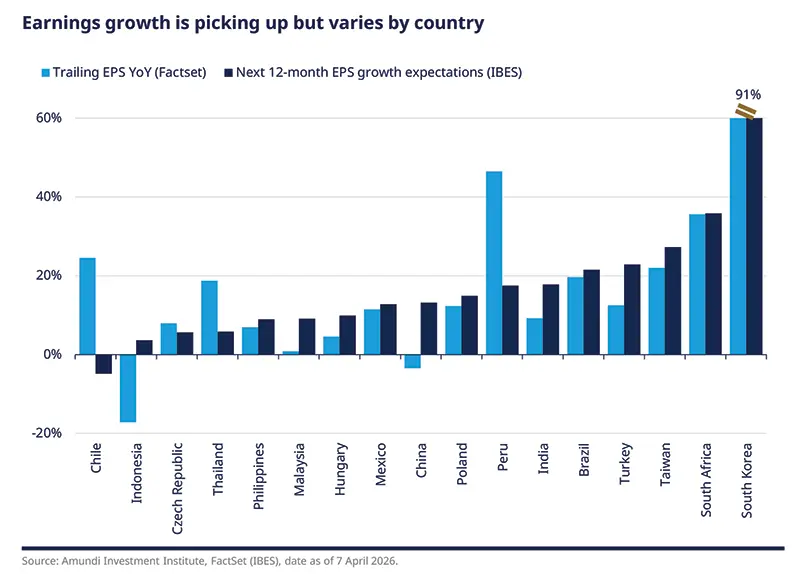

Earnings growth is a key driver of this EM resilience, but divergences persist as EM countries are being affected unevenly. Latin America is relatively insulated given its distance from the conflict and status as a net energy exporter, while Asian energy importers are more exposed. Higher oil, gas, fertiliser and freight costs can slow disinflation, with a tougher inflation/interest-rate trade-off for importers. Fiscal space and the ability to implement subsidies also vary across the region. For example, the fiscal space is greater in Korea, Taiwan and China than in India, Indonesia, the Philippines and Thailand. Overall, EM resilience is confirmed also by the smaller capital outflows, contained borrowing costs and stronger policy frameworks recently highlighted by the IMF.

Earnings expectations are accelerating, resulting in the MSCI EM Index EPS expectations rising to 31%. We believe this expectation is too optimistic, albeit we expect that EPS growth will remain strong, particularly as the tech cycle remains a key support. Asian tech companies are delivering strong results, with EPS expectations having stabilised at 66% (April 2026). Even so, EM equities trade at a significant valuation discount (MSCI EM Index is at discount of about 39% on a forward PE and about 42% on price-to-book).

In this current environment, we remain constructive on EM, including EM Asia and EMEA. In particular, we prefer Korea and Taiwan, which benefit from the tech and semiconductor cycle as well as robust earnings momentum. Although oil sensitivity has tempered expectations in India, we remain positive on this region as the earnings cycle is healthy. Elsewhere, we are neutral on China and retain a positive view on Latin America, particularly Brazil.

POSITIVE South Korea – energy importer but supported by tech exposure and fiscal strength

South Korea remains one of EM’s strongest earnings stories. Earnings momentum remains supportive with consensus 2026 EPS growth expectations at 91%. Our internal estimate is more cautious but momentum remains positive. Revisions are among the strongest in EM Asia, profitability is improving and the tech cycle remains supportive. In Korea and Taiwan, hardware stocks have risen on strong AI-driven memory demand. Higher memory prices would usually trigger more supply, but there is no sign of that yet. This supports EM semiconductor earnings and provides AI exposure at more attractive valuations than in the US. After the initial sell-off, the market recovered quickly, and we continue to view South Korea as one of the most attractive EM equity markets. South Korea is exposed to the conflict, through energy-intensive sectors, exporter margins and weaker global demand, but we expect overall a modest economic hit. Valuations remain reasonable, especially given earnings strength, and Korea still trades at a discount to both EM and developed markets. Medium-term upside is also supported by governance reform, including the Value-Up programme. | 91% |

POSITIVE Taiwan – tech and earnings revision support with a modest CPI pickup expected

Valuations have improved recently, while consensus 2026 EPS growth expectations have risen to around 27%. ROE is close to 17%, supported by semiconductor and AI-related component demand. Revisions are the best in EM Asia, though we remain cautious over a six-month horizon, as medium-term valuations are not cheap. Taiwan is exposed to Middle East energy, especially LNG, but the near-term risk is more inflationary than related to a supply shortage. LNG reserves are limited, though supply has been secured through June, and critical tech-sector power loads will be backed by coal generation. With fuel-price pass-through capped, we expect only a modest CPI pickup, allowing the central bank to stay on hold. The main risk is a longer disruption, which would pressure energy costs and petrochemical output. Overall, earnings are less directly affected by the crisis, but remain vulnerable to weaker global growth. Taiwan tech has held up well, and we still see upside supported by AI capex and non-AI export frontloading, though concentration remains a concern. | 27% |

NEUTRAL (but POSITIVE longer-term) India – earnings expectations are decent and valuations are not excessive

India has underperformed due to its sensitivity to energy imports and direct corporate exposure to the Middle East. Valuations are now more reasonable and earnings expectations are solid, with consensus EPS growth forecast close to 18% in April 2026, not far from our internal expectations. Revisions are improving. Nominal GDP growth should pick up as loan growth rises and credit costs trough, although private corporate capex remains a headwind. India is one of EM Asia’s most oil-sensitive economies and one of the highest oil-beta markets globally, through inflation, fiscal pressure, fuel subsidy risk, and INR depreciation. We estimate EPS sensitivity at roughly -3% to -5% for every 10% increase in oil prices. Energy imports amount to 2.7% of GDP, with around 40% of oil and LNG and almost all LPG sourced from the Middle East. The government can use price caps and targeted support, but this shifts the burden to the fiscal accounts and the current account. With only about 25 days of strategic reserves, the key risk is to activity and external financing rather than inflation. Overall, we retain a long-term positive outlook for India, while acknowledging that in the short-term, exposure to higher oil prices and fiscal pressures may act as a dampener on economic growth and the equity market outlook. | 18% |

NEUTRAL China – limited growth impact but meaningful inflation impulse, prefer H-shares

China is a diversified economy with large coal and oil reserves and a growing share of renewables. So far, exposure to the Strait of Hormuz is manageable thanks to electrification and diversified imports, especially from Russia and Central Asia, although oil still matters: net oil and gas imports amount to about 1.8% of GDP, around 50% of imported oil passes through the Strait of Hormuz, and oil accounts for nearly 30% of final energy consumption. Fuel-price pass-through is capped at 50%, with the rest absorbed by state-owned companies. This should limit the growth impact, but inflation pressure through PPI and energy-intensive sectors remains meaningful. We prefer H-shares, where the policy backdrop is more supportive. While the earnings outlook for this market is less supportive than in other markets, valuations suggest greater upside potential for H-shares. | 13% |

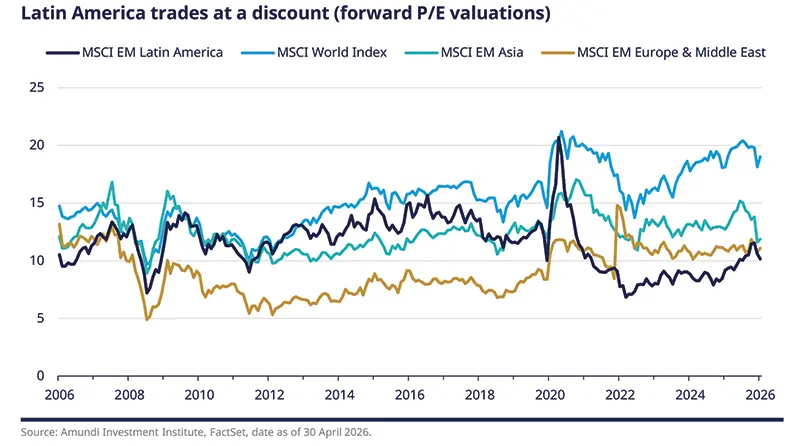

Latin America: oil support and solid macro backdrop

Latin America stands out favourably in the current global environment, supported by net energy exposure, metals production, stronger macro fundamentals, prudent monetary policy, and its distance from the conflict region. While the impact of the war is uneven, the overall macro and earnings backdrop supports a positive tilt.

The main distinction is between net oil exporters and importers, with the region being a net energy exporter on average. Brazil, Argentina, Colombia, Ecuador, and Venezuela should benefit from higher oil prices, while Chile and Peru are more exposed to higher costs. A sharp rise in commodity prices could hurt importers and complicate inflation and easing cycles. This could not only slow disinflation but also lead to outright inflationary pressures, with spillovers to transport and food. The IMF suggests the main risk is inflationary pressure rather than stagflation. Central banks remain cautious and are ready to act if needed to protect credibility and inflation expectations.

The region also benefits from exposure to natural resources, including rare earths, precious metals, and metals linked to the energy transition and AI investment. Relative to other regions, Latin America’s AI exposure remains limited, making it a useful source of equity diversification.

Performance has been strong, reflecting investor rotation away from expensive US assets. The region remains at a discount to EM, though it is not especially cheap versus its own history. Selectivity remains key.

POSITIVE Brazil – strong earnings growth supporting valuations

We have a favourable tilt towards Brazil, driven by improving IBES EPS growth expectations, which rose from 12% in March to 21% in April, and we expect positive earnings revisions due to high commodity prices.

We believe the easing cycle is better described as a “calibration cycle”. Brazil’s policy rate remains very high by historical standards, as the central bank stays focused on potential inflationary pressures. This caution may limit support for the market. So far, the economy has avoided recession: last year’s second-half soft patch did not turn into a recession, and the economy accelerated at the beginning of the year. However, if the commodity shock lasts too long, it could weigh on the domestic economy through higher inflation and tighter financial conditions.

The fiscal position remains the main structural weakness: high debt and it is still rising, and the IMF remains skeptical about consolidation. The October 2026 election is also a key risk factor, with markets likely to pay closer attention as the vote nears. A tight race is expected. The political outcome could matter for fiscal consolidation, investor confidence and potential market repricing. Valuations are not extremely cheap, but they are supported by stronger earnings growth than some peers.

Authors