Summary

Key takeaways

Asia is stepping up as a focal point for ESG regulation innovation, demonstrated by a market-calibrated approach that is increasingly aligned with international standards.

Asia’s responsible investment market remains resilient, with sustainable investment inflows continuing in Q3 2025, and regulatory improvements strengthening disclosure and incentives, while rising public financing and de risking mechanisms are accelerating investment in transition projects.

China: Asia’s green finance giant moves towards mandatory corporate disclosures for high polluting firms, with expansion to major stock indices by 2026. Hong Kong: charges ahead in the race to go green, as Hong Kong Monetary Authority (HKMA) publishes a taxonomy for the country.

Japan: strengthening standards amid slow progress, with the release of International Sustainability Standards Board (ISSB) aligned disclosures standards and the implementation of gender diversity targets and sectoral transition roadmaps.

India: regulation push builds momentum as the Business Responsibility and Sustainability Reporting (BRSR) has been made mandatory for top 1000 listed companies, and a Draft Climate Finance Taxonomy has been published.

Singapore: Innovating the region’s green finance playbook, as the Monetary Authority of Singapore (MAS) launches Finance for Net Zero (FiNZ) plan.

Racing towards the green hub post: Regional Trends and Market Realities

Asia’s ESG Momentum: Phased Policy, Traffic-Light Taxonomies and RI Expansion

Asia is rapidly emerging as a pivotal arena for ESG regulatory innovation, driven by the region’s unique economic dynamics, environmental challenges, social priorities, and development levels. The shift from voluntary ESG practices to mandatory, market-specific disclosure regimes reflects local realities while aligning with global standards, portraying different jurisdictions’ efforts to tackle increasing climate risks through regulation. Such concerns are especially pressing for the APAC region, which derives about 75% of its GDP from moderate to heavily nature dependent sectors1. This paper offers cross-market, non-exhaustive, insights to help investors operate in Asia’s fast-paced environment, followed by a detailed country-level analysis of ESG regulatory landscapes in China (including Hong Kong), Japan, India, and Singapore.

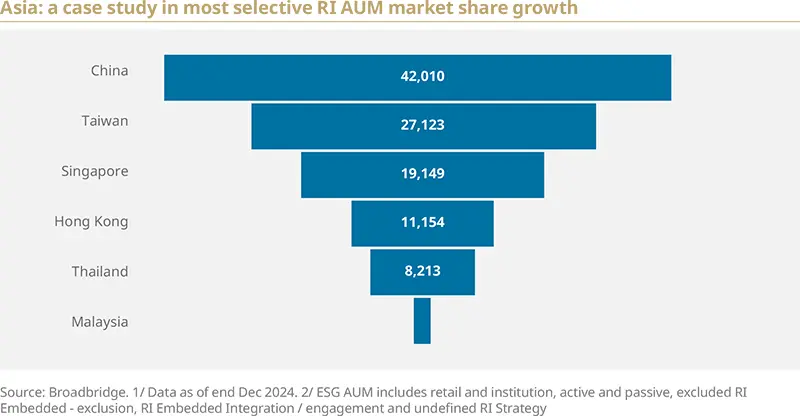

Despite backlash from certain stakeholders, Asia’s share of Responsible Investment (RI) Assets Under Management (AUM) still remains relatively low but displays steady growth rates, increasing from 1% in 2020 to 3% in 2025 (Broadridge, 2025). The expected shift of economies towards mandatory ESG reporting aligned with international frameworks, combined with a race among regions – particularly Hong Kong and Singapore- to become the region’s green finance hub, suggests that this region is poised for even faster growth in responsible investing in the near future.

A key aspect of the region’s ESG regulatory development is the move towards regulations tailored to local social, economic and political realities, acknowledging the current reliance on non-sustainable assets while still paving the path for decarbonization routes. Examples include phased implementations of regulations, the use of traffic light taxonomies (which define a category for transitional activities with a structured decarbonisation pathway), and mechanisms to avoid market disruption, such as transition risk management and aid to hard-to-abate sectors.

Focus #1 - Sustainable Finance: Asia’s Expanding Role as a Global Green Capital Hub Asia’s sustainable finance market is among the fastest growing worldwide, with green bond issuance reaching approximately 24% of the global total. This growth is underpinned by strong government support, innovative taxonomy development, and expanding financial instruments.

|

Market opportunities remain despite headwinds

While market conditions have moderated compared with previous years, the fundamental drivers that make the region an attractive investment destination remain. As shown by Morningstar6, despite outflows from China, Hong Kong and Japan in the last quarters, sustainable finance inflows remain positive at $1.6 billion during the third quarter of 2025 (excluding China), primarily driven by Thailand through regulatory benefits such as tax deductions.

At the same time, regulatory advances are creating a supportive environment for sustainable finance, being reflected in market-based mechanisms that are scaling up investments in transition projects. Global investments in clean energy, for instance, reached $2.1 trillion in 2024 (up 11% yoy), partially financed via debt issuance and equity raises. The Asia Pacific region grew the fastest, at 21%, with China taking the lead and representing roughly two thirds of the total increases7.

Focus #2 - In Practice: regional tools to push forward RI policy developments

|

Asia’s ESG Regulatory Transformation: Critical Drivers Reshaping Investment Decisions

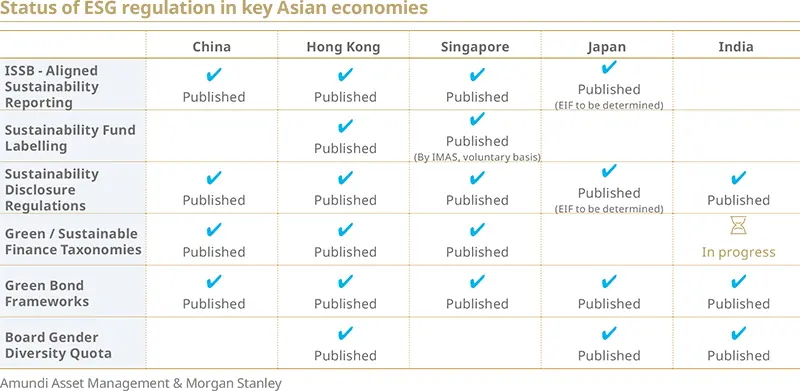

As has been already pointed out, the five Asian countries studied here follow a pragmatic approach when it comes to navigating the ESG, with frameworks such as ISSB-aligned sustainability reporting, sustainability fund labelling, and green taxonomies being present or under development for most of the jurisdictions analysed. While there is an effort to cooperate and develop benchmark-aligned regulations, the need to calibrate regulatory frameworks to local realities and different stages of development must not be overlooked.

Convergencies and complementarities in the region are unfolding together, with most regulations increasingly aligning corporate disclosure requirements with ISSB and Task Force on Climate-Related Financial Disclosures (TCFD) standards, and all of them are moving towards mandatory reporting for top companies. Such efforts help attract international capital for multinational firms. Regulators are also adopting phased approaches, as well as delaying requirements for smaller firms (as is the case in Singapore regarding its Climate Reporting Requirements).

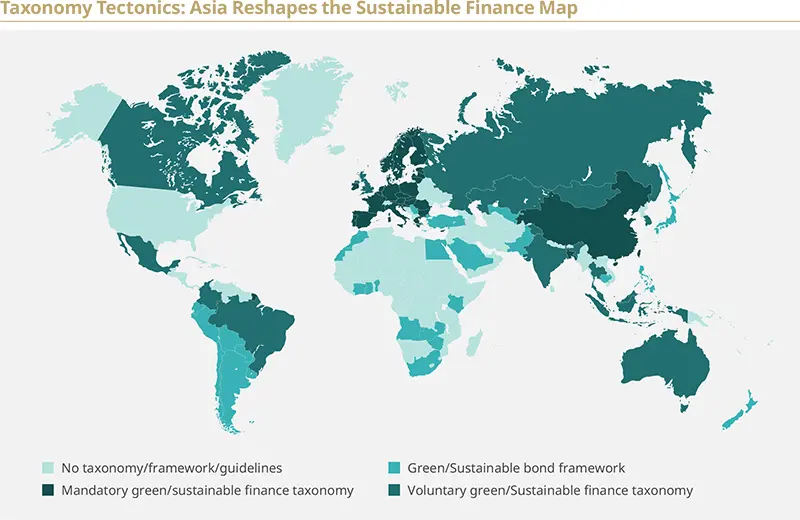

On taxonomies, China’s Common Ground Taxonomy and the Multi-Jurisdiction Common Ground Taxonomy (M-CGT) are important milestones as they build bridges between Asian and European economies, in an effort to reduce fragmentation and improve interoperability to enhance cross-border capital flows.

Another key factor is the collaborative learning dynamic across the region. Public disclosure of results and credibility of indicators have spillover effects in interconnected countries, fostering regional cooperation and the exchange of best practices. When one regulator body implements an effective policy, neighbouring authorities are more likely to adopt it quickly, generating efficiency gains. For instance, China and Singapore have identified synergies within their sustainable finance ecosystems, with the People’s Bank of China and the MAS committing to deepen collaboration in joint initiatives such as taxonomy development, facilitating bilateral green financing flows and technology solutions11.

Although there is broad agreement on the overall direction of ESG policy development, approaches to implementation vary by region. In some countries, the State takes a leading role such as in China with low-cost loans designed for companies who want to cut carbon emissions12. By contrast, monetary authorities in Singapore and Hong Kong tend to issue guidelines and offer incentives to encourage adoption by the private sector, as is the case of the Sustainable Bond Grant Scheme launched by MAS13 or the Finance Grant Scheme launched by HKMA, which provide subsidies for green finance.

Focus #3 - A case study on interoperability: M-CGT and Singapore Asia taxonomy As sustainable finance advances in Asia, some key initiatives are focusing on building bridges between different regulations. Efforts to enhance interoperability are central to building a more efficient regional sustainable-finance ecosystem. Beyond promoting greater harmonization, the multiple efforts illustrate how jurisdictions are developing frameworks to position themselves within the emerging green finance landscape. Among these efforts; the M-CGT (an extension of the CGT), and the Singapore-Asia taxonomy stand out as important case studies.

|

Country Spotlights: ESG Regulatory Landscapes and Sustainable Finance in Asia’s Key Markets

China: Asia’s green finance giant enters a phase of deeper regulatory convergence

China’s ESG regulatory framework has evolved from voluntary guidelines to a mandatory system targeting high-polluting companies and bond issuers, with expanded ESG reporting required for major stock indices by 2026 for large listed companies. The China Green Bond Endorsed Project Catalogue (2021) and the updated EU-China Common Ground Taxonomy underpin its green finance taxonomy, facilitating cross-border investment flows.

Corporate: In February 2024, the China Securities Regulatory Commission mandated that constituents of major indexes disclose their ESG data from 2026 onward. In parallel, the Basic Guidelines for Corporate Sustainability Disclosures published by the Ministry of Finance in 2024 established a unified national framework and encourage all reporting entities to disclose sustainability information.

Finance: In 2022, China Banking and Insurance Regulatory Commission (CBIRC) issued the Green Finance Guidelines for the Banking and Insurance Industry, mandating insurance institutions to disclose on green finance strategy, status and development, as well as to align portfolios with neutrality goals. New 2022 green bonds rules require 100% of proceedings to be invested in green projects (vs 70% previously).

Taxonomy: China strengthened its classification system through two domestic pillars: the Green Finance Support Project Catalogue14, which unifies standards across green financial products, and NDRC’s Green and Low-Carbon Transition Catalogue, which expands coverage to transition activities. It also advanced G20 transition finance work, developed transition taxonomies for four hard to abate sectors, and progressed on a Multi Jurisdiction Common Ground Taxonomy based on the EU–China Common Ground Taxonomy.

Hong Kong: Targeting the green finance hub position amid Mainland Integration

Being the biggest market for offshore Chinese green bond issuance issuance, the region accounts for more than US$ 43bn of GSS15+ bonds issued in 2024, about 45% of Asia’s total16. Its Sustainable Finance taxonomy, alongside the publishing of their Sustainability Fund Labelling, has also strengthened their hub role17.

Corporate: HKEX mandates all issuers to make climate-related disclosures aligned with ISSB and TCFD standards from 2025.

Finance: following mainland China, Hong Kong has developed a robust green bond market. Cooperation with China remains central to its strategy, evidenced by several partnerships, including a collaboration with the China Emissions Exchange in Shenzhen. The HKMA has also launched the Sustainable Finance Action Agenda, focusing on four key areas: Banking for net zero, Investing in a sustainable future, Financing net zero, and Making sustainability more inclusive - signalling the ambition to become a sustainable green finance hub for the region.

Taxonomy: in 2024, the HKMA launched the Hong Kong Taxonomy for Sustainable Finance, having as its goal to serve as an assessment tool for the industry and facilitate green finance flow.

Japan: strengthening standards amid slow progress

Japan’s Corporate Governance Code integrates sustainability into management strategies, with the Tokyo Stock Exchange’s Prime Market requiring

enhanced climate disclosures. The Sustainability Standards Board of Japan adopted ISSB standards in 2025, with phased application starting from the largest companies. Social initiatives focus on gender diversity and pay gap reporting, with targets to increase female directors to 30% by 2030.

Corporate: Japan’s Sustainability Standards Boards released ISSB-aligned disclosure standards, which is probably going to be applied from 2027 for Prime Market companies. Greenwashing reduction strategies have also been put in place, as the Financial Services Agency (FSA) present guidelines for investment, with sustainable funds having to consider ESG a key factor.

Finance: country’s focus on support of transition bonds, impact investment and innovative green finance products.

Taxonomy: though the country does not yet have a consolidated taxonomy, a detailed transition roadmap has been presented for 10 main sectors.

India: regulation push builds momentum

India’s sustainable finance landscape is progressing as disclosures become mandatory for top companies and a draft taxonomy is currently being developed. SEBI has introduced regulations on ESG rating providers and detailed ESG fund categories and disclosure requirements. Labor reforms and value chain disclosure requirements further strengthen social and governance aspects.

Corporate: focus on the BSRS, with reporting becoming mandatory for top 1000 listed companies by market caps from FY 2022-2023.

Finance: initiatives to expand green financial instruments have been implemented with

the development of a Green Bonds framework to attract green investment,

the engagement of largest banks in publishing TCFD reports, and

mandatory green deposit schemes by Scheduled Commercial Banks (SCBs) and deposit-taking NBFIs. Complementing existing regulations on disclosure requirements for green debt securities, SEBI has also published in 2025 disclosure requirements around issuance of social, sustainability and sustainability-linked bonds.

Taxonomy: the country has also made advancements regarding taxonomy with the Draft Climate Finance Taxonomy, which aims at preventing greenwashing and mobilizing green finance aligned with climate goals.

Singapore: Innovating the region’s green finance playbook

Singapore mandates climate reporting for high-impact sectors, with MAS’s FiNZ Action Plan expanding transition finance instruments, reinforcing the country’s efforts to become the region’s green finance centre. It also leads regional taxonomy innovation with the Singapore-Asia Taxonomy (SAT), featuring a pioneering traffic-light system including transition activities, and has been active in the development of carbon markets.

Corporate: Singapore Exchange (SGX) has made disclosures mandatory for listed business, taking effect for financial, energy, food and forest sectors in 2023; and materials, buildings, and transportation sectors in 2024. SGX has also progressed toward incorporating ISSB-aligned climate reporting into its disclosure requirements in 2025, requiring issuers to report based on ISSB requirements for reports published in 2026.

Finance: the MAS has launched its FiNZ action plan, with the objective of setting out strategies for a net-zero transition. Among the proposed mechanisms are transition bonds and loans and the extension of Insurance-Linked Securities issuance grants.

Taxonomy: convened by MAS, the Singapore-Asia Taxonomy for Sustainable Finance innovates as it introduces a traffic light system allowing for the incorporation of transitioning activities and hard-to-abate sectors. The country has also walked towards cooperation, working alongside China and the EU to launch the M-CGT, though full application remains in progress.

Conclusion

Asia’s ESG regulatory landscape is undergoing transformation, marked by a pragmatic convergence towards international standards such as ISSB and TCFD, while simultaneously tailoring frameworks to local realities. The region adopted phased mandatory disclosures, innovative taxonomies, and stronger oversight of ESG data providers, fostering both transparency and market integrity. Notably, Asia is pioneering transition finance, with Japan and China providing blueprints for decarbonizing hard-to-abate sectors, and Singapore mobilizing blended finance to accelerate net-zero pathways.

These regulatory advances are not only attracting international capital but also catalyzing regional cooperation and knowledge transfer. The focus on social dimensions, including gender diversity and labor reforms, further enhances the region’s sustainable investment proposition. Despite global headwinds, Asia’s responsible investment market continues to expand, underpinned by resilient inflows and supportive policy environments. For global investors, understanding the nuanced, rapidly evolving ESG frameworks across China, Hong Kong, Japan, India, and Singapore is essential to unlocking value and managing risks. Ultimately, Asia’s regulatory innovation and market dynamism position it as a pivotal driver in the global sustainable finance agenda, offering both challenges and unprecedented opportunities for forward-looking asset managers.

ADB: Asian Development Bank

AIA: Asian Infrastructure Investment Bank

ASEAN: Association of Southeast Asian Nations

AUM: Assets Under Management

BRSR: Business Responsibility and Sustainability Reporting

CBIRC: China Banking and Insurance Regulatory Commission

CGT: Common Ground Taxonomy

CSRC: China Securities Regulatory Commission

FAST – P: Financing Asia’s Transition Partnership

FiNZ: Finance for Net Zero

FSA: Financial Services Agency

HKEX: Hong Kong Stock Exchange

HKMA: Hong Kong Monetary Authority

IPSF: International Platform on Sustainable Finance

ISSB: International Sustainability Standards Board

MAS: Monetary Authority of Singapore

M – CGT: Multi-Jurisdiction Common Ground Taxonomy

MoF: Ministry of Finance

NBFI: Non Banking Financial Institutions

PBoC: People’s Bank of China

PRI: Principles for Responsible Investment

RI: Responsible Investment

SAT: Singapore-Asia taxonomy for sustainable finance

SCB: Scheduled Commercial Banks

SEBI: Securities and Exchange Board of India

SGX: Singapore Exchange

SGFC: Singapore Green Finance Centre

SFIA: Sustainable Finance Institute Asia

SGFin: the Sustainable and Green Finance Institute

TCFD: Task Force on Climate-Related Financial Disclosures

1. Asia-Pacific Climate Report 2025: Unlocking Nature for Development | Asian Development Bank

2. Global State of the Market 2024 | Climate Bonds

3. Singapore Commits US$500 Million in Matching Concessional Funding to Support Decarbonisation in Asia

4. Green Investments Partnership, a Blended Finance Fund under Singapore’s FAST-P initiative, Achieves First Close with US$510

Million in Committed Capital

5. Singapore and UK Collaborate on Energy Transition and Sustainable Infrastructure Investments in Southeast Asia

6. Global Sustainable Fund Flows: Q3 2025 in Review | Morningstar

7. Energy Transition Investment Trends | BloombergNEF

8. Finalization of “the Code of Conduct for ESG Evaluation and Data Providers”

9. MAS Media Release - MAS Publishes Code of Conduct for Providers of ESG Rating and Data Products - For media.pdf

10. ICMA-Hong-Kong-Code-of-Conduct-for-ESG-Ratings-and-Data-Products-Providers-ENGLISH-version-October-2024-031024.pdf

11. https://www.mas.gov.sg/news/media-releases/2025/mas-and-pboc-deepen-cooperation-in-green-and-transition-finance-at-

the-3rd-singapore-china-gftf

12. China’s central bank to extend low-carbon lending tool to end of 2027 | Reuters

13. Monetary Authority of Singapore

14. China’s new Green Finance Catalogue brings clarity… | Climate Bonds

15. Green, social, sustainability and sustainability-linked

16. Hong Kong Leads Asia’s GSS+ Bond Market as Policy and… | Climate Bonds

17. List of ESG funds | Securities & Futures Commission of Hong Kong

Author