Summary

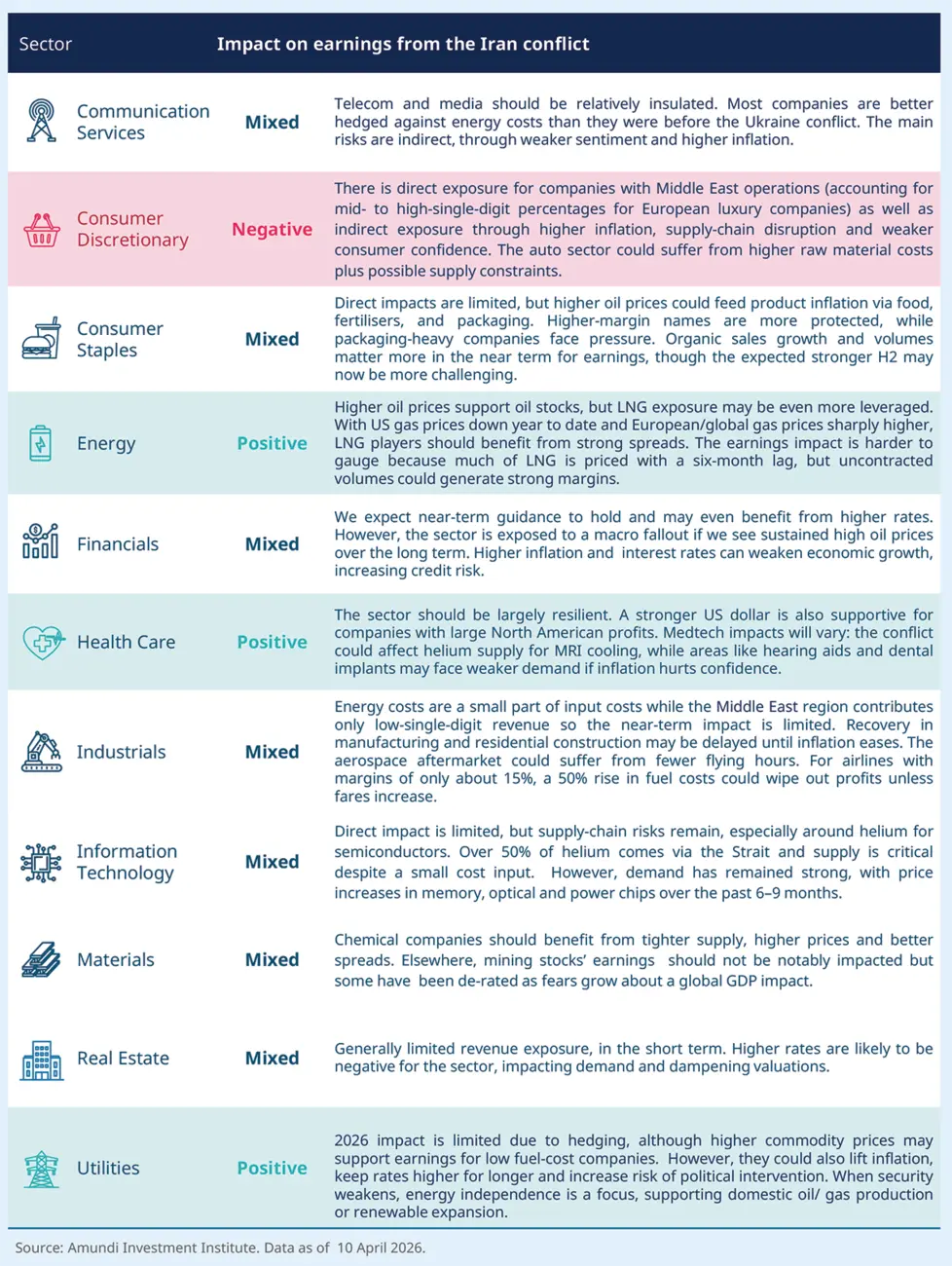

We believe that European companies’ Q1 earnings should remain relatively robust. As the Iran conflict only started at the end of February, the impact is likely to be more visible in Q2 reporting and beyond; while the pullback in share prices so far have mostly been due to valuation multiple de-rating from a higher equity risk premium given the uncertain outlook. The eventual magnitude of the earnings impact will ultimately depend on the intensity of the conflict and how long the Hormuz Strait energy supply blockages persist.

We note that generally periods of higher inflation tend to support nominal earnings, while stronger currency pairs at the end of Q1 (compared to when guidance was issued in Feb), such as USD/EUR, should also be a modest tailwind for some sectors (e.g. pharma companies generate more than 50% of revenue from North America). As evident from the Ukraine invasion experience of 2022, EPS growth was revised higher for many sectors, with energy leading the way. This should be the case again for the Iran conflict, with energy and utilities set to benefit from higher oil, LNG and power prices.

In addition, the financial sector’s revenues should benefit from the higher yield backdrop, albeit potentially offset by any front-loading of loan provisions under the new IFRS 9 accounting rules for some institutions (mostly by the UK Asian banks which have exposure to the Middle East region). Chemical companies could benefit from supply dislocations, and airlines are protected in the near term by fuel hedging programmes, although they face jet fuel shortages if the situation persists. The push by policymakers to secure Europe’s energy supply over the coming years is also likely to intensify, and this should support the renewable industry, as well as companies involved in the electricity grid buildout.

The longer the conflict lasts, the greater the drag on growth, earnings and markets.

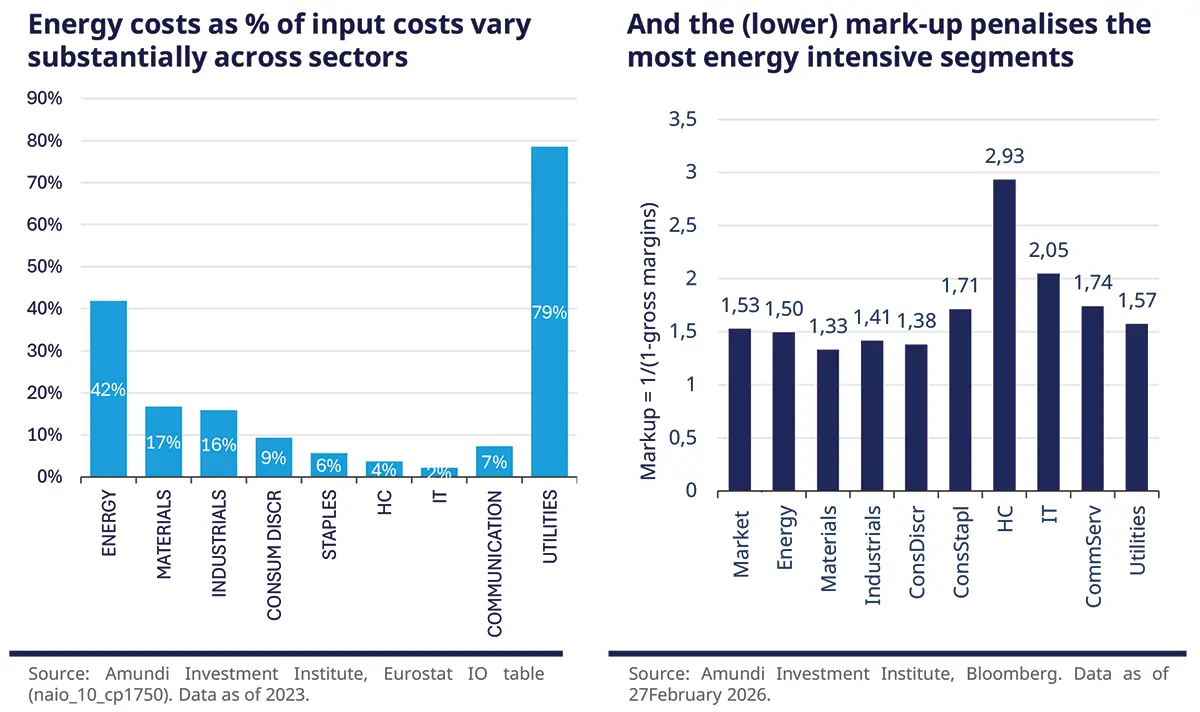

However, the longer the conflict persists, the greater the toll on economic growth across the region, which would create margins and earnings pressure. While Eurozone PPI remains substantially below the level seen before Ukraine was invaded (EZ PPI was around 29% YoY in February 2022, it is firmly below -3% YoY currently), macro conditions are less conducive for most companies now to a full pass-through to consumer prices, and this highlights a negative asymmetry for margins. Higher energy prices would likely penalise sectors with high energy costs as a percentage of total input costs, as well as those facing intense competition and limited pricing power. This would be the case for the transport sector (where, on average, around 30% of input costs are energy-related) and consumer discretionary stocks. In addition, weaker consumer affordability and confidence would adversely affect demand for consumer products in general. The ability of companies, such as those in consumer staples, to raise prices to offset higher raw materials and energy costs is also likely to diminish, in contrast to the Ukraine-related inflation shock.

The consequences of a long-lasting conflict will increase the risks of recession over time (more adverse scenario).

If higher energy prices persist, global recession risks increase, creating asset-quality concerns for banks and insurance companies, notwithstanding their currently strong balance sheets and solvency levels heading into this crisis. Global companies’ supply chains have been better diversified in recent years, although reliance on certain products, such as helium and agri-feedstocks that pass through the Strait of Hormuz, could adversely affect some sectors, including semiconductors and medtech, as shortages emerge. Demand destruction and delayed capex decisions are also likely in this scenario, which would be negative for industrial companies and the wider economy. While defence stocks should benefit from current conflicts and heightened geopolitical tensions underlining the need for Europe to re-arm, there has been some volatility in this sector since the outbreak of the Iran conflict, due to long positioning and worries about potentially higher government fiscal deficits which may be exacerbated by the potential need to subsidise energy prices.

Therefore, we may see a slowdown in new defence orders if the conflict persists and the economic outlook deteriorates, although longer-term growth remains well underpinned for this sector. Energy and utility companies also increasingly face the risk of new government taxes/levies over coming months if they are perceived to be generating super normal profits at the expense of the public.

European sectors impact of a short-term conflict The main transmission channels to sectors are higher oil and gas prices, which feed through to margins, input costs, consumer spending and inflation. A second channel is the macro and policy response: stronger inflation can keep rates higher for longer, lift credit risk, and increase intervention risk in more regulated sectors.

At this stage it is unclear if companies will provide new / reset financial guidance for the remainder of full-year 2026 given the uncertainties in the macro outlook. Source: Amundi assessment as of 10 April 2026. |

European sectors – assessing the impact of the energy shock

Authors