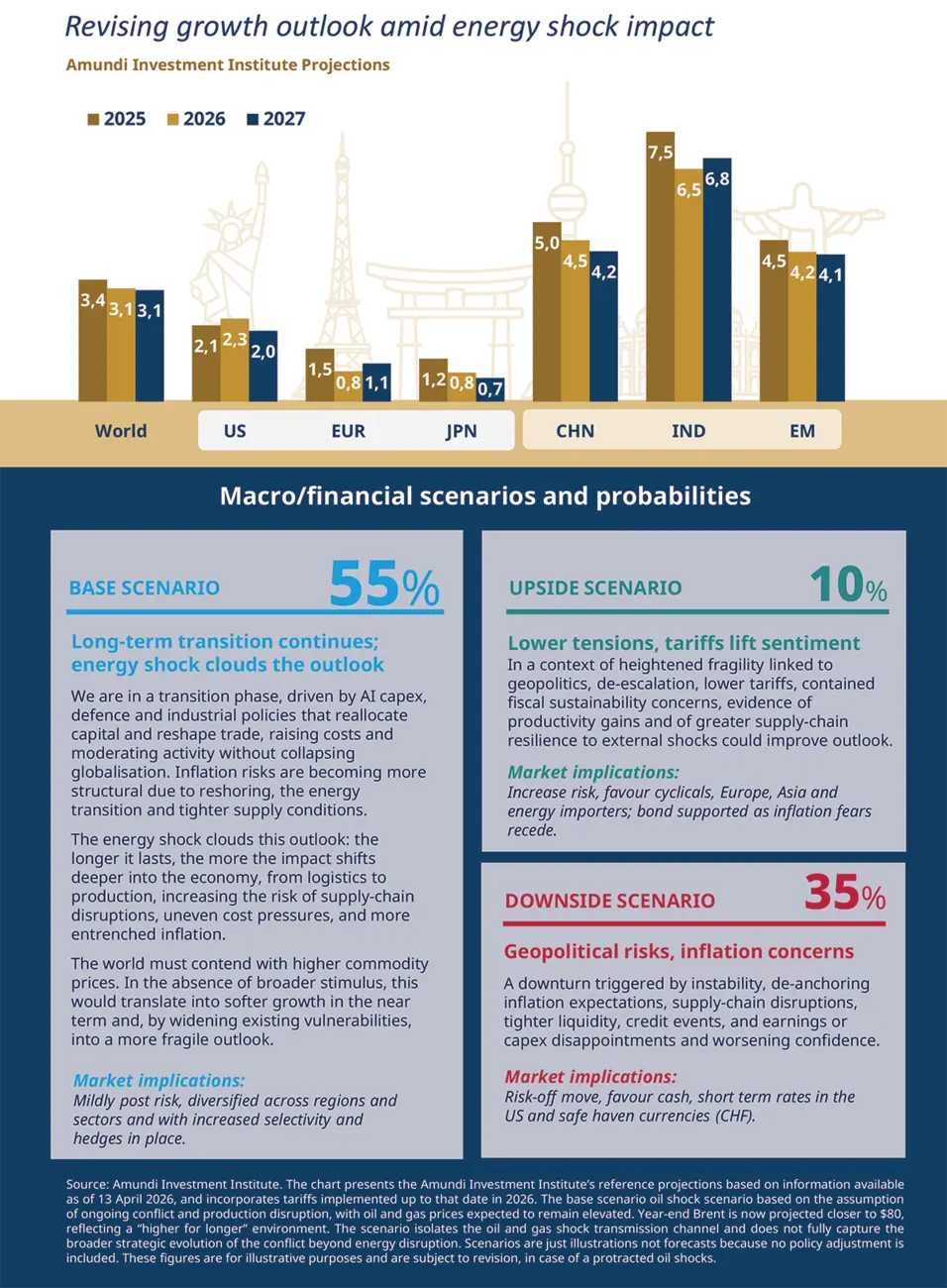

Summary

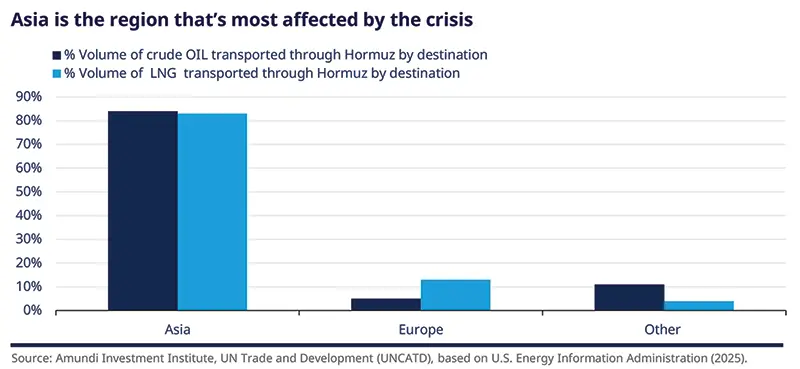

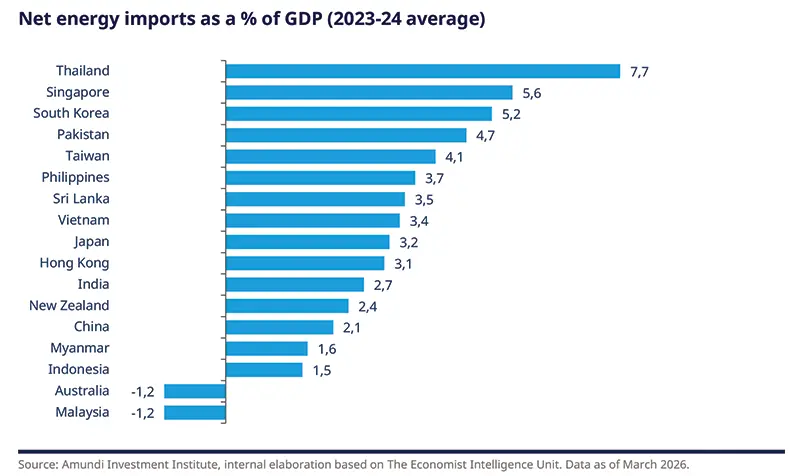

Asia is exposed to the Middle East conflict and the resulting rise in oil and gas prices. Most countries in the region are net energy importers (Malaysia is a notable exception). Even if the pass‑through to headline inflation remains limited, sustaining cost‑of‑living support to shield household purchasing power will be expensive for governments. Many of these governments entered the shock with weak fiscal positions and active fiscal consolidation plans; the conflict will make consolidation more difficult. In practice, policymakers are likely to reallocate spending from capex — weakening growth perspectives — toward subsidies as a first response, before accepting wider fiscal slippage. On the investment side, we should not underestimate the impact on North‑East Asia’s energy‑intensive chip and memory sectors and the global repercussions if those supply chains are disrupted. The region still has short‑term buffers for energy — more than three months for oil in many cases, but substantially less for gas.

CHINA – diversification efforts are positive, but oil still accounts for a significant share of end use.

While China’s net imports of oil & gas account for 1.8% of GDP, and ~50% of its oil imports come through Hormuz, the country has advanced rapidly on electrification and diversified energy import sources (notably with the Shanghai Cooperation Organization countries, i.e. Russia and central Asia). Still, oil represents nearly 30% of final energy consumption, and a shortage will affect jet fuel, trucking, and petrochemical industries mostly. The government has limited the pass-through of fuel price hikes to consumers by 50%, with the rest of the costs shared by state-owned oil companies. The impact on growth will be minimum, but the inflation spike, especially to PPI, will be meaningful. | 30% |

INDIA – risk of funds meant for capex being diverted to subsidies

India's energy imports represent 2.7% of GDP, with ~40% of its oil & LNG and almost all LPG (cooking fuel for ~330mn households) sourced from the Middle East, making it one of the most vulnerable Asian economies to the Hormuz disruption. The government's retail price cap and its corporate burden-sharing mechanism deliberately suppresses the consumer-facing inflation pass-through. But the cost has not disappeared — it has been shifted onto fiscal accounts as an accumulated subsidy burden and onto the external position as an import cost rise without any corresponding price adjustment. | 40% |

With only 25 days of strategic oil reserves, a prolonged supply disruption is a more acute near-term risk, while the price caps should contain the inflation shock. The activity impact will be felt relatively more than the inflation impact; although a fiscal slippage will depend on the length and intensity of the conflict.

The immediate impact will be on public capex once expenditure is diverted from investments to households through subsidies. High energy and fertiliser prices will significantly increase the subsidy bill, while the end of March excise tax cuts will diminish revenue. Bond yields face upward pressure from the twin-deficit narrative (a widening current account combined with rising fiscal burden), while INR will face renewed depreciation pressures despite its attractive valuation.

SOUTH KOREA – bigger push to inflation, modest hit to growth

South Korea is one of the most highly exposed economies to the Middle East conflict. Its net energy imports are above 5% of GDP, and disruption in the Strait of Hormuz would hit domestic energy consumption and its large refinery sector, which source around 70% of its crude from the Middle East. That said, we do not expect a major deterioration in the terms of trade in 2026: strong memory-chip exports, supported by AI-driven demand, should offset part of the energy shock. We therefore see only a modest hit to growth (-0.3%), but a meaningful inflation pickup, keeping the Bank of Korea on hold for now while raising the risk of a July hike. Fiscal support has expanded, with a KRW 26.2tn supplementary budget (1% of GDP) announced and 40% of spending allocated to mitigate the Iran war impact in the form of cash handouts and subsidies. | 70% |

TAIWAN – contained inflation pick-up if the crisis is limited in duration

Taiwan is highly exposed to Middle East energy, especially LNG (~25% sourced from the region), but the near-term risk is linked more to inflation than to outright shortages. LNG reserves are limited (~11 days), yet the authorities have already secured LNG supply throughout June. Critical power loads for the tech sector will be secured by its back-up coal power generation capability. As the fuel price hikes are capped, we expect only a contained CPI pickup, allowing the CBC to look through the energy-driven inflation bump and keep policy on an extended hold. The key risk is a longer disruption, which would eventually pressure both energy costs and petrochemical output. | 11 |

INDONESIA – fiscal stance was already loose before the crisis

The country’s direct energy vulnerability to the Iran conflict is structurally lower than its Asian peers. It is a net exporter of coal and LNG, and imports only ~13% of crude oil from the Middle East. Government response options are nonetheless constrained: subsidy absorption risks breaching the 3% fiscal ceiling, while restricting coal or LNG exports to preserve domestic supply would sacrifice foreign exchange earnings. Critically, the country entered this shock carrying pre-existing institutional damage — the policy mix has already become less orthodox increasing the country risk premium. | 13% |

By the end of last year, fiscal spending in Indonesia has become more indisciplined due to several initiatives like the intensifying free meal programme — all of which had already eroded investor confidence in policy credibility before this latest energy shock. Energy subsidies represent an important component of public expenditure (around 6.5%) and in the budget assumptions, oil was set at $70/bbl. Therefore, bond repricing risk is also driven by the accumulated institutional and fiscal risk premium: the 3% ceiling was already being stretched pre-conflict, and the July S&P review creates a binary outcome that bond markets cannot ignore; Bank Indonesia's stance reflects delayed and reduced cuts, amid renewed concerns about financial stability and IDR depreciation. | 1,5% |

PHILIPPINES – fiscal deficit limits space for broad subsidies

Philippines faces 3.7% energy imports as a percentage of GDP (chart above) with extreme concentration: ~95% of crude oil comes from the Middle East, and limited substitute supply sources create a structural vulnerability to single-region disruption. That concentrated energy shock, together with weakening remittances (~18% of remittances come from the Middle East), could widen the current account deficit by more than 0.5 percentage point of GDP. The government response is explicitly constrained: the fiscal deficit was already at 5.6% pre-crisis, eliminating room for broad subsidies, and forcing a reliance on targeted transport measures only; energy conservation mandates (air conditioner limits, shortened work weeks) and VAT exemptions on fuel provide limited relief. The central bank’s (BSP) hawkish inflation-targeting bias and willingness to raise rates if inflation pressures materialise reflects an orthodox central banking stance. But raising rates becomes a demand-destructive policy tool when fiscal space is already exhausted. Bond repricing reflects the triple pressure of BSP rate hikes, fiscal deterioration and the fastest inflation pass-through in the region. PHP depreciation pressures will likely remain with external vulnerability. | 3,7% |

THAILAND – risks of a strong stagflationary impulse

Thailand's over 7% total energy imports as a percentage of GDP is the highest in Asia, with ~50% of crude oil sourced from Middle East. This creates a structural vulnerability amplified by tourism dependency (11% of GDP), where energy costs directly translate into higher travel costs and weaker receipts. The government has introduced an export ban on selected petroleum products and imposed diesel price caps. But an export ban cannot substitute for lost supply if the Hormuz disruption is prolonged. Bank of Thailand’s (BOT) latest rate cut was undertaken in a context of weak economic conditions amid entrenched deflationary concerns. The conflict in the Middle East came later and could now expose Thailand to a stagflationary risk that fiscal policy will struggle to deal with due to the limited room available. Bond pricing reflects the heightened risk and limited policy space to prevent further deterioration. | 50% |

JAPAN – BOJ likely to delay rate hike, not reverse course

The country remains structurally exposed to Gulf oil, importing roughly 70% of its crude from the region, so higher energy prices will squeeze real incomes. However, Japan has the highest level of oil reserves in Asia (over 260 days), and Prime Minister Takaichi’s fiscal stimulus should cushion the shock and prevent a deeper growth slowdown. The Iran conflict reinforces our call that the next BoJ hike is more likely to happen in June instead of April, as we expect the BoJ to focus on the impacts of uncertainties in its growth outlook; if the shock worsens, the BoJ is more likely to delay tightening than to reverse it. The conflict also strengthens the case for Japan’s longer-term supply-chain security agenda. | 260 |

Asian sectors in focus

|

Authors