Summary

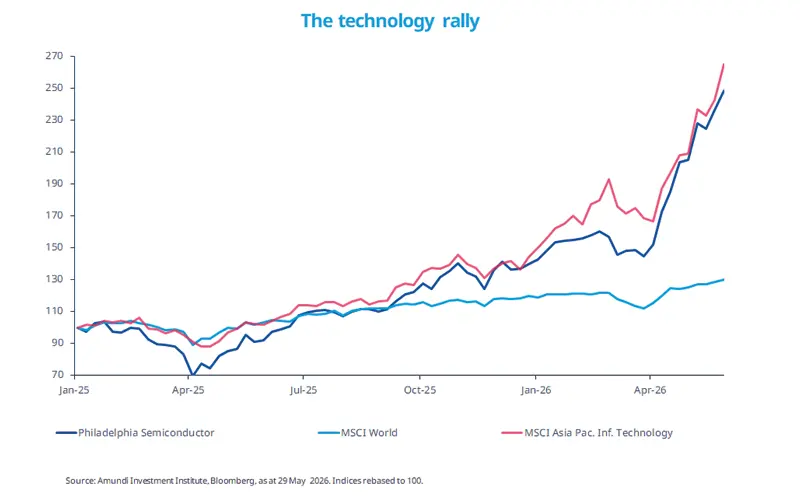

The AI rally is not just a US story. Opportunities are strengthening across regions, especially in Asia. The mantra for generating long-term returns is diversification across different segments in the global technology sector.

The rally of global markets from the lows of March has been mainly an IT-driven story. This has been visible in US and Asian markets.

We are constructive on sectors such as Asian technology where earnings growth is strong.

Greater diversification within the tech sector can improve portfolio resilience and reduce exposure to unexpected shifts in the AI landscape.

The global artificial intelligence (AI) rally this year has enabled the markets to look through the geopolitical conflict in the Middle East. The AI rally is clearly visible in the outperformance of the US semiconductor sector, but the US is not the only space offering AI-related opportunities. Led by tech companies, Asian markets have also rallied strongly since the start of 2026.

This strong performance of Asian tech highlights the breadth of opportunities across the AI value chain globally. While US companies maintain leadership in semiconductors and cloud computing, Chinese firms benefit from economies of scale, government support and access to critical minerals. South Korea offers expertise in memory chips, while Europe is home to businesses in AI-related physical infrastructure and enabling technologies such as data centres. Over time, the opportunity should spread out across regions, and more industries — making diversification increasingly important. The key is to identify companies offering sustainable earnings growth that are available at attractive prices.

This week at a glance

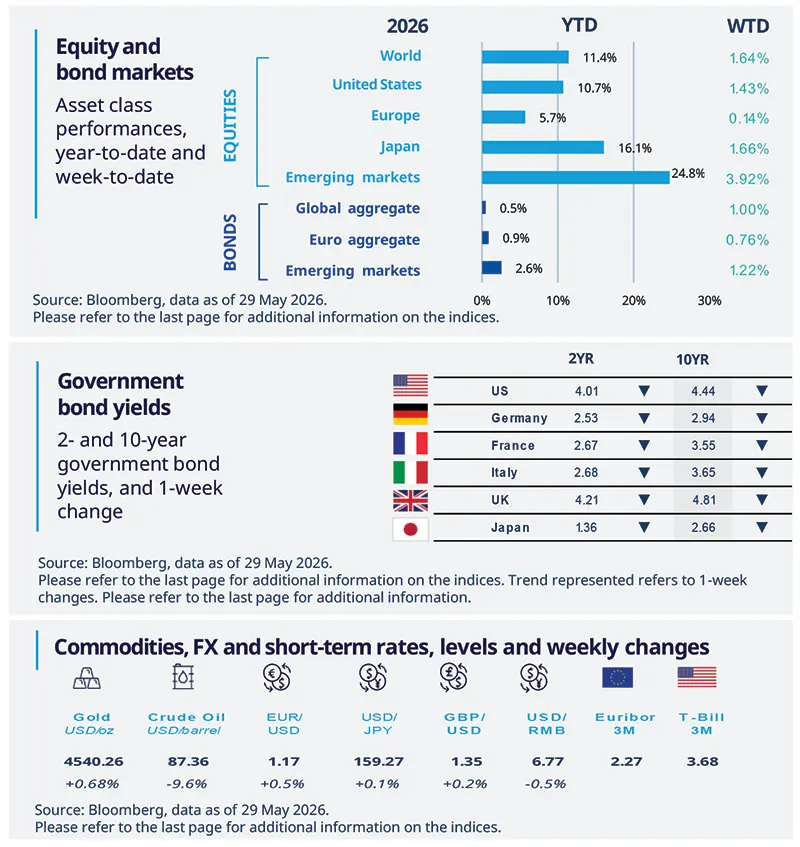

Global equities rose, with the S&P 500 and Nasdaq reaching all-time highs as investors waited to see whether a deal would be finalized between the US and Iran. This prospect eased pressure on oil prices amid optimism that flows through the Strait of Hormuz could be restored. It also supported a downward revision in inflation expectations and risk premium, with consequent declines in bond yields across curves.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 29 May 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

In the US: weaker GDP, solid corporate profits

The second estimate of Q1 GDP growth was revised down to 1.6% QoQ, from the previous estimate of 2%. The downward revision mainly reflected softer consumer spending and a weaker contribution from inventories. Meanwhile, the first estimate of corporate profits for Q1 pointed to a quarterly growth of 3.3% QoQ growth. Domestic profits rose sharply, driven by the non-financial sectors, highlighting healthy margins among domestic companies and providing an important buffer against input-cost pressures.

Europe

Eurozone Sentiment improves, but remains subdued

The Eurozone Economic Sentiment rose to 93.5 in May, above expectations, although it remains well below its long-term average. The survey showed a rebound in services and some stabilisation among consumers, while industry, retail trade and construction weakened. Services were supported by improved demand expectations, while industry was weighed down by lower production expectations and a less favourable assessment of finished goods stocks. Managers’ selling price expectations also eased across all sectors, interrupting the steep upward trend seen over the previous two months.

Asia

Bank of Korea turns more hawkish

The Bank of Korea left policy rates unchanged, as expected, but its forward guidance was more hawkish than markets had anticipated, pointing to two rate hikes as the baseline over the next six months. The updated outlook suggests a stronger growth picture, with the 2026 GDP forecast raised to 2.6% from 2.0%, supported by the semiconductor boom and government measures to offset Middle East shocks. The 2026 inflation forecast was also lifted to 2.7% from 2.2%. Together, resilient exports, firmer inflation, renewed housing price pressures in Seoul and a weak won suggest that policy tightening is likely on the horizon.

Key dates

EZ Manufacturing PMI, ECB Inflation Expectations, US ISM, China Manufacturing PMI |

EZ Services PMI and PPI, China Services PMI |

EZ GDP Q1, US NonFarm Payrolls, India GDP |

Authors