Summary

As the path to a stable ceasefire remains uncertain, investors should diversify across regions and asset classes in order to withstand the ongoing geopolitical shifts.

Tensions flare amid fragile ceasefire

Tensions flared in the Strait of Hormuz as Iran attacked passing ships. The US responded with airstrikes.

Recent tensions pushed Brent oil prices towards $80, interrupting the steep decline since mid-June.

The latest round of attacks has underscored the “fragile” nature of the de-escalation and sparked market volatility.

Tensions in the Middle East have resurfaced, underscoring the “fragile” nature of the recent de-escalation. The latest round of attacks may be tied to Iran’s effort to preserve its leverage over the Strait of Hormuz. Meanwhile, Trump may become more willing to escalate tensions while oil prices remain subdued. Still, both sides have reasons to remain at the negotiation table, as the US approaches midterm elections and Iran would benefit from economic relief.

Although rerouting efforts have helped to normalise oil prices, recent tensions have emphasised that the ceasefire remains fragile, and traffic through the Strait of Hormuz is once again disrupted. Brent oil prices rose towards $80 a barrel, and we expect them to remain under pressure in the coming days.

The dynamics of oil prices and rerouting are important for their implications for inflation and central bank action. In the meantime, markets will remain volatile.

This week at a glance

The resumption of attacks in the Middle East immediately sent equity markets lower and oil prices higher. A subsequent recovery in semiconductor stocks helped broader equity markets rise slightly as investors tried to look past fresh hostilities between the US and Iran. In fixed income, yields rose amid expectations of hawkish central banks and inflations concerns. Gold fall as tensions raise the prospects for interest-rate hikes.

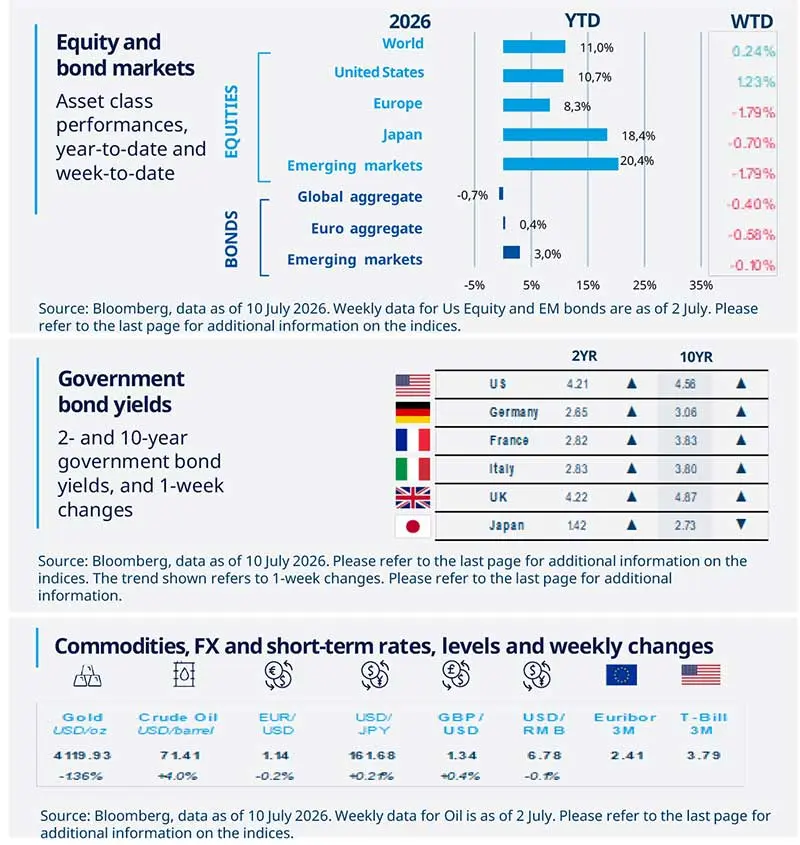

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 10 July 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US ISM services index remains in expansion territory

The ISM services index eased in June but remained above the expansionary threshold for the 24th straight month. New orders and business activity both softened by roughly 2 points, while employment jumped to its best reading since 2024, with World Cup hiring noted in the fine print. However, inflationary pressures remain evident: the index has stayed above 60 for 19 consecutive months, with diesel, petrol, oil and related commodities most frequently cited as rising in price.

Europe

Euro area retail sales slowly pick up

Euro area retail sales increased in May. The report indicates that consumption is holding up even as fuel purchases quietly retreated. Compared with a year earlier, retail growth ticked up to 1.6%. Looking ahead, consumption could be supported by the recovery in real disposable income as inflation slows; however, as savings rates remain structurally high, reflecting strong precautionary behaviour, we see limited scope for further consumption growth.

Asia

Asia: inflation mostly down, with exceptions

Declining fuel prices and lower transport fares helped push headline CPI softer across several Asian economies in June, including China, Thailand, and the Philippines — all coming in slightly below expectations. Taiwan was the exception, posting higher-than-expected CPI driven by broad-based inflation pressures. Renewed uncertainty stemming from tensions in the Middle East is clouding the inflation outlook once again, though the shock from energy prices remains more manageable than before.

Key Dates

Japan industrial production; US CPI; China trade balance |

China GDP, retail sales and industrial production; US PPI |

Euro area inflation, US consumer sentiment |

Authors