Summary

The crisis is a stark reminder that security extends beyond defence. It depends, among other things, on secure energy and resilient supply chains. Transitioning to clean energy is therefore both an environmental priority and a strategic imperative for geopolitical strength and economic resilience.

The energy crisis is increasing the need for green transition investment. On 3 June, the European Commission announced additional fiscal flexibility for energy security investments.

This conviction is not without historical precedent: for instance, the 1973 oil crisis led France to expand its nuclear energy program.

Overall, a well-planned green transition may help build economic resilience and improve energy security. In the process, investors would come across long-term opportunities.

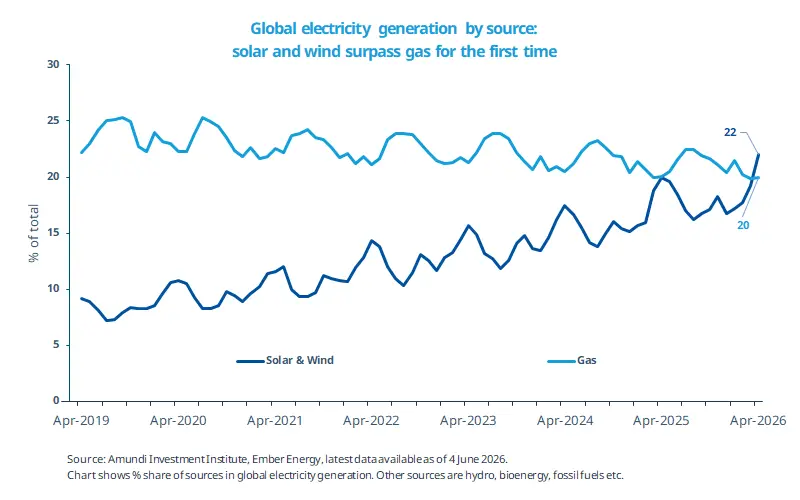

The ongoing energy crisis is exposing the vulnerabilities associated with imported energy, particularly in Europe and Asia. Most countries have implemented targeted measures in the form of tax cuts and subsidies on fuel. Additionally, the EU has given member states greater fiscal room to support households and businesses in reducing their reliance on fossil fuels. While investments in the green transition are beneficial from an environmental perspective, they also enhance energy security and improve long-term economic resilience. Already, the share of solar and wind in global electricity generation has increased substantially (22% in April 2026), as shown in the chart. Looking ahead, proponents of green energy will draw support from the limited control that energy consumers have over fossil fuel supply and will likely highlight the reliability of domestically produced energy. The crisis is therefore likely to accelerate the transition towards clean energy and create investment opportunities across the value chain globally.

This week at a glance

Equity markets came under pressure in the second half of the week amid fading enthusiasm around AI and concerns over Fed rate hikes, as US data remained resilient. In addition, the S&P 500 maintained the inclusion criteria for recently listed companies, preventing newly listed but large companies from being included in the index immediately. Bond yields and oil rose amid strong US data, particularly on the labour market, and concerns about the Iran-US conflict. In FX markets, the USD gained.

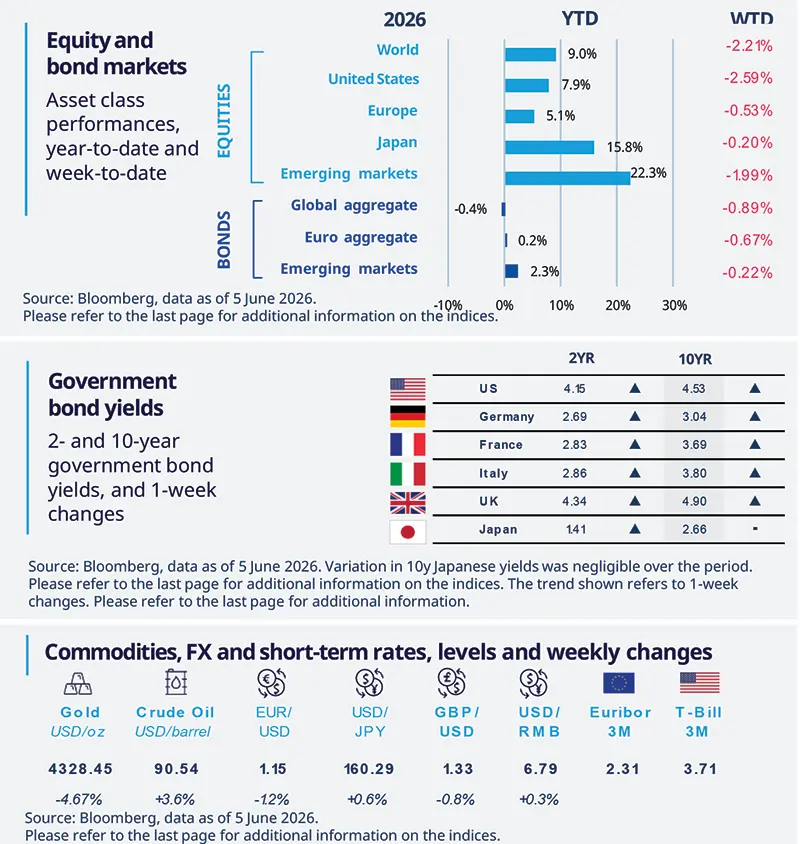

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 5 June 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US economy shows resilience despite lingering risks

The ISM Manufacturing Index rose to 54 in May from 52.7, its strongest reading since May 2022, while the Services Index increased to 54.5 from 53.6. Second, durable goods and factory orders jumped in April. Although these data indicate resilience, factory employment has fallen by 77,000 jobs, and private spending on manufacturing construction is also down since Trump’s second term began. Looking ahead, we think the resilience of the American consumer will increasingly come into question, as will the impact of the likely next Fed hike.

Europe

Euro Area inflation rises as energy costs surge

EZ inflation reached 3.2% in May, up from 3.0% in April. Energy costs surged 10.9%, the steepest rise since February 2023, fuelled by supply constraints linked to the Iran conflict. In general, energy costs continue to be the most pressing issue in the economy, but the situation is not as severe as the energy shock seen in 2022. Looking at some leading indicators such as the manufacturing PMI, we noticed that the index fell to 51.6 in May but stayed in the expansionary territory. Services data, however, remained in contraction territory.

Asia

Japan wage gains support consumption

April wage growth maintained strong momentum, with the BoJ’s preferred measure – the full-time scheduled earnings – growing 3.7% YoY. Real wages stayed positive for the fourth consecutive month as inflation eased amid a series of government subsidies. Consequently, consumption rose 1.6% MoM, the largest increase since September 2022. The broad-based wage gains should help cushion potential headwinds from Middle East tensions and rising cost pressures.

Key dates

US CPI, Canada policy rate, China PPI and CPI |

ECB Policy Rate, US PPI, Turkey policy rate |

Japan Industrial Production, UK Industrial Production, US Consumer Confidence |

Authors