Summary

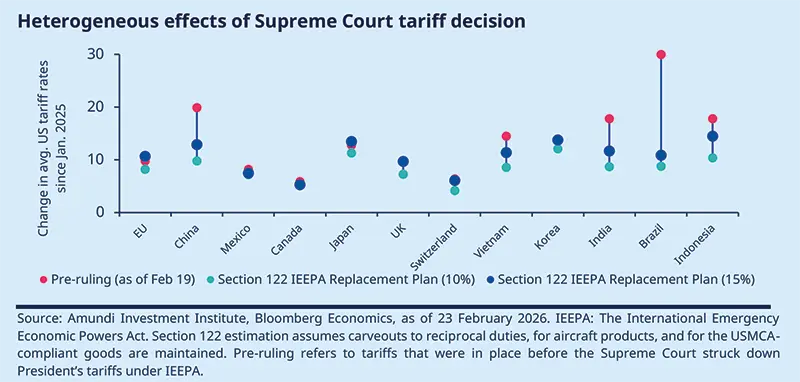

Since the start of the year, some of the key convictions that we have highlighted in our outlook have been playing out and some trends have accelerated. We are witnessing a regime shift characterised by heightened policy uncertainty and a distinct break in the international order — key themes highlighted at the Davos World Economic Forum and confirmed at the Munich Security Conference. Tariffs remain a key tool for the redesign of the new order. Here, the recent Supreme Court ruling against Trump’s emergency tariffs introduced an additional layer of uncertainty to the policy landscape.

All these developments confirm that the overall geoeconomic environment is in transition. President Lagarde’s mention in her speech of the ECB’s new repo facility for central banks outside the euro area signifies how policymakers are thinking about the rising importance of geoeconomics.

We are clearly entering a more complex market equilibrium, where policy — including trade policy — geopolitics, and capital allocation are as critical as the economic cycle itself. With growth proving more resilient than initially expected and corporate profitability remaining robust, markets have remained well sustained. However, significant rotations are underway across countries, sectors, and individual stocks as the environment adjusts to the ongoing regime shift.

A diversified and flexible approach will likely be the name of the game for investors to deal with these shifts and rotations.

In a fast changing world, it is a good time to reassess our main convictions:

Conviction #1: The cycle keeps turning: a transition with better momentum in US and Europe, not a downturn.

In 2025, the US economy has proved very resilient, driven by artificial intelligence (AI) and tech investments and the wealth effect. Robust domestic consumption dynamics have led us to upgrade our growth view for this year to close to 2.5% year-on-year (yoy), assuming a positive impact from US fiscal measures (such as tax cuts) affecting consumers and companies this year on top of a stronger carry over momentum from consumption. However, labour markets could prove a tricky puzzle to solve leading to a two speed economy, which is what the recent economic numbers point to. January’s CPI, which was below market expectations, confirms our views on disinflation and we maintain that inflation will remain between 2.5% and 3% this year. There will be volatility in the next few months, but overall CPI and core PCE should decelerate. The key elements that would drive core CPI lower are services inflation and owners' equivalent rent. In the Eurozone (EZ), the positive growth surprises at year end (Italy, Spain) are welcome and are creating a stronger carry over into 2026. We also see better momentum in domestic demand in these countries.

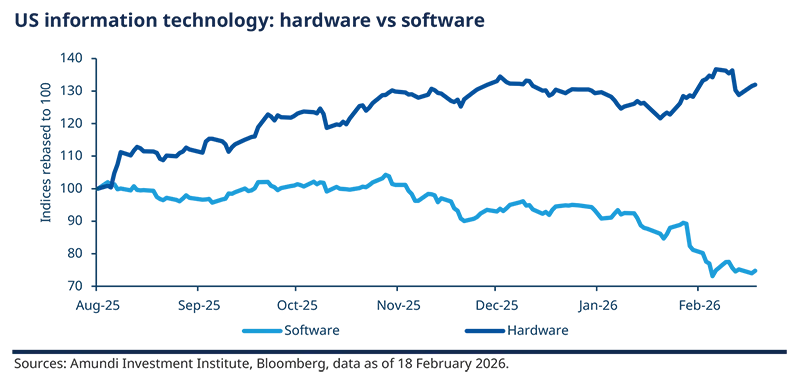

Additionally, our conviction on the AI capex cycle is firmly in place but we note that markets will increasingly distinguish between the winners and losers — those that can demonstrate returns or potential returns clearly and are transparent, versus those that remain ambiguous ('where is the money'). The recent weakness in some technology names reflects the market’s assessment of risk and its questioning of companies that could lose out (for example, certain software segments and trucking) from AI disruption. Yet, with AI expected to drive productivity gains for the economy, which will be reflected in corporate earnings over the long term, we continue to see a pro-risk backdrop in place.

Conviction #2: Diversifying in an era of controlled disorder, to generate long-term returns.

The era of controlled disorder is about realising that the world is not de-globalising but becoming multi-polar. Investors would need to navigate the markets through better diversification.

We believe we are still in the initial phase of a regime shift, in which the rise of middle powers is accelerating the shift towards a multipolar world. The India–EU deal is a recent example, enabling Europe to diversify its trade and dependence on the US, although this will take time. This challenge to US superpower status will occur in parallel with the rise of China, spanning geopolitics, supply chains and Beijing’s emphasis on establishing leadership in technology.

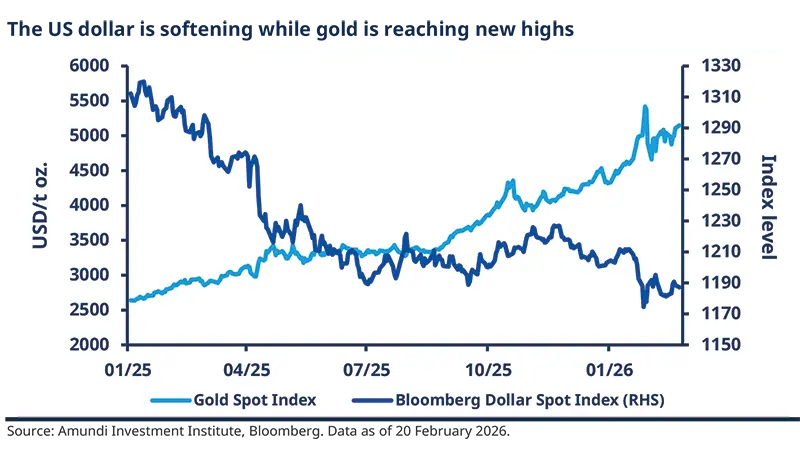

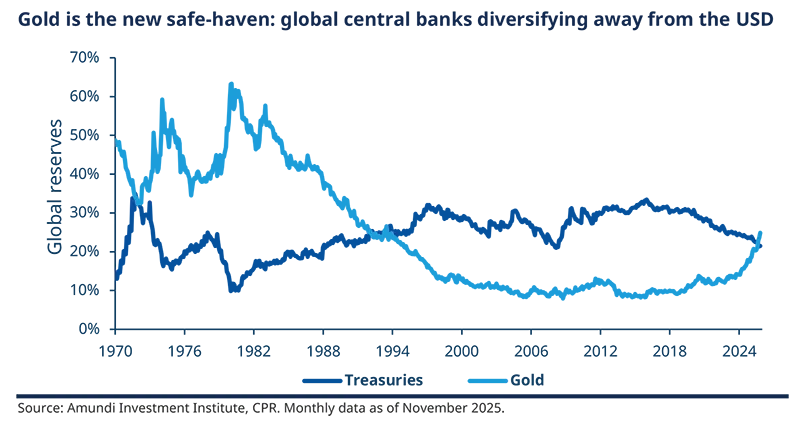

Commodities as structural hedges and source of portfolio resilience. From an asset allocation perspective, we believe metals such as gold balance out the risk coming from geopolitics and rising public debt. Gold will also benefit from structural demand. At the same time, base metals such as copper should remain essential for cleantech and the green transition.

Among global investors, there is rising discomfort with concentrated US dollar exposure, and early signs of portfolio reallocation towards European and emerging market assets. The dollar system is not being abandoned. But it is notably being questioned, for instance by the high uncertainty arising from the US Supreme Court ruling.

We believe this shift towards a controlled disorder is structural, not cyclical, and diversification conversations are accelerating. It also reinforces our view of gold as a structural hedge.

Alessia BERARDI | Aidan YAO Senior Investment Strategist, AII | |

The US Supreme Court ruling and Trump’s response add to the uncertainty. The court’s ruling affects only the tariffs imposed under the International Emergency Economic Powers Act (IEEPA). These include the fentanyl tariffs on China, Canada, and Mexico; the universal (10%) and reciprocal tariffs announced on April 2; and the additional charges against India and Brazil. However, sectoral tariffs (under Section 233), tariffs levied on China since 2018 (under Section 301), and specific duties on steel/aluminium/solar panels (under Section 201) are not affected. The President has responded to the Court ruling with harsh words and moved quickly to seek replacements. That consists of two steps.

“The ruling serves as a reminder to investors that the rule of law is firmly in place in the US. It also confirms that in a world of controlled disorder, trading arrangements would change quickly.”

Market implications Overall, we think the verdict will create near-term uncertainty for US trade policy but should not alter the medium-term path of Trump’s protectionist agenda. Reconstructing the same effective tariff rate under different laws is feasible but will take time and may provoke further legal challenges, making the tariff transition a risk for the economy and markets. At the same time, uncertainty — about which products will be taxed, at what rates, and for how long — will likely create volatility in trade flows and may further delay corporate investment. The reaction of other countries that signed trade deals on the basis of IEEPA tariffs is an additional source of uncertainty. Secondly, if tariffs were removed (unlikely) or reduced (more likely, but not our base case), reversing a negative supply shock would be positive for the economy and markets, and would make the Fed’s job easier. Abolishing IEEPA tariffs would also lift US GDP growth. This helps explain the initial positive reaction in risky assets. However, losing the tariff revenue is bad news for the US government, bonds and the US dollar. Finally, if reduced use of tariffs gave rise to greater US military muscle-flexing, global geopolitics could become far more perilous. “President Trump can still use other acts to further his tariff agenda, which would of course complicate matters for companies and countries involved.”

| ||

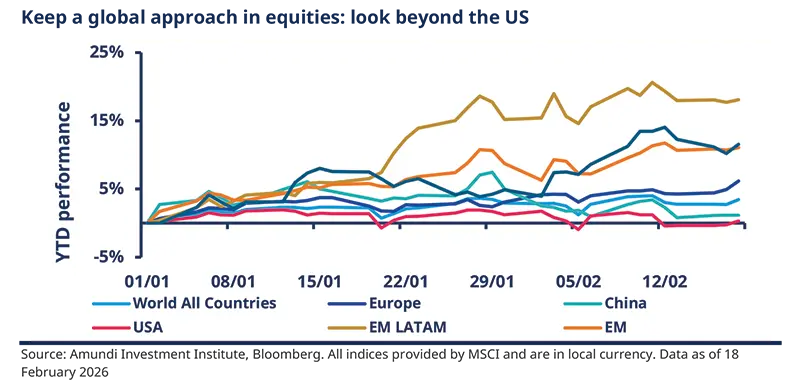

Conviction #3: Think global in equities, beyond the tech race to reduce concentration risks.

Maintaining a global approach in equities, beyond the tech race in the US, will be crucial for generating sustainable returns.

Thinking global means understanding that we are shifting from a phase dominated by liquidity and synchronised policy toward one where balance sheets, industrial policies and capital allocation decisions are setting prices. We are also observing a transition toward a more fragmented, selective and granular market environment. One such example of granularity is that instead of focusing on the broad AI theme, we believe companies involved in AI-related physical infrastructure and the industrials sector are the ones to favour.

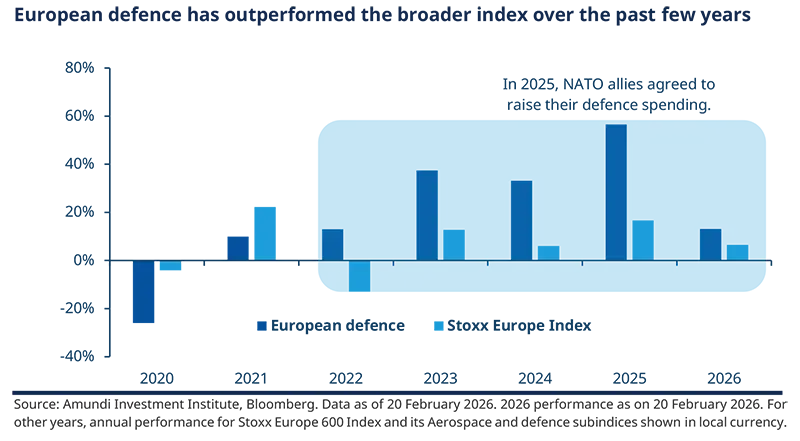

Regionally, in Japan, industrials, financials and businesses that show corporate reforms are where value will be generated. We also see opportunities in the US in industrials, innovation-led technology and financials. In Europe, sectors such as industrials, defence, financials and infrastructure would gain prominence. In particular, we think Europe’s push towards its strategic autonomy with an objective to improve economic resilience and boost security spending will create opportunities from a long term perspective. Markets have also been appreciating this over the past few years, as outlined in the chart.

Additionally, the rotation out of US technology names towards other sectors and regions was already visible in Q4 last year and it is continuing in 2026.

More recently, this year’s AI scare has given the rotation a renewed vigour. The S&P 500 software, Mag 7, Nasdaq 100 and Russell 1000 growth indices have all declined so far, whereas the S&P 500 Equal Weighted and Russell 1000 Value indices rose, year to date (as of 20 Feb). Interestingly, Chinese tech was also slightly positive during this period. From a regional perspective, the Japanese, European and the broader emerging market indices outperformed the leading US and technology indices.

To conclude, our conviction to explore global equities beyond the US tech sector stays in place — it may have different legs, but we see it as a long-term trend.

Conviction #4: Fiscal and monetary policies will drive investment opportunities.

The interplay of fiscal policy, monetary policy and geopolitics would affect market behaviour, implying traditional safe- havens may no longer work.

We have been vocal about the debasement risks to the US dollar stemming from high US debt and fiscal deficits, and from global central banks diversifying their reserves away from the greenback for geopolitical reasons. This is eroding the dollar’s safe haven allure, although the private sector has been slow to shift its preference away from the currency so far. If and when that happens, it would be another long term headwind. We keep a structural weak call on the US dollar (1.22 at the end of the year versus euro), with tactical adjustments in the near term.

Staying on the fiscal side, an era of fiscal expansion appears confirmed in Japan. Political stability, corporate governance reforms and reflation are affecting the behaviour of foreign investors towards Japan. PM Takaichi’s consolidation of power means she is likely to pursue measures (including tax cuts) to boost real wage growth by reducing CPI, while also prioritising economic growth. This will, of course, affect JGBs and the yen in the near term.

On the monetary front, we made some revisions and postponed Fed rate cuts. We expect one rate cut around the middle of the year (June/July) and another in September. By then the Fed will have more visibility on inflation data, and the new Fed Chair nominee, Kevin Warsh, will have taken office.

There is debate about his past hawkish tendencies regarding reduction of the Fed’s balance sheet. We think the bar for Warsh to reduce the Fed’s balance sheet is high, as it could drain market liquidity and put the repo market under stress. What the Fed might instead do is reduce the share of longer-dated Treasuries on its balance sheet and increase the share of shorter maturities. Regarding the ECB, we expect the bank to cut rates once this year, in Q3. Euro strength, tighter credit conditions or any deterioration in the labour market could change that.

Hence, it is crucial to remain tactical on duration, given that risks of financial repression are high and central banks such as those in the US and Japan may potentially come under political pressure, with already high fiscal deficits. The BOJ aims to bring inflation within the 1.5–2.0% range. At the same time, following PM Takaichi’s consolidation of power, the BOJ may face pressure to slow its rate hikes. Hence, we remained cautious on Japanese duration for much of last year, and rising bond yields helped. Moving into 2026, we have raised duration to neutrality.

Conviction #5: Europe and emerging markets offer long-term opportunities.

Diversification and flexibility in allocation would be key to identifying market rotations across various segments and regions.

Europe is realising that it can no longer rely on the US as an economic partner and provider of security as it used to previously. This realisation will go a long way in helping the region build its strategic autonomy. But the region, independent of the US, needs to invest more in defence, technology and supply chains, a message reiterated by the recent Munich Security Conference. All of these aspects would have a security dimension. Additionally, we continue to believe that emerging markets (EM) should be a key pillar for global investors — not only to diversify but also to access strong businesses and growth opportunities.

In India, which we confirm as a structural allocation in EM, we have marginally upgraded this year’s growth projection from 6.6% to 6.8%, and believe the Reserve Bank of India will keep rates on hold for the rest of the year. The risk could be short-term volatility but not a structural reversal. Policy continuity will support the capex cycle, and the lowering of US tariffs is reinforcing the China-plus narrative (manufacturing outside China). The recent EU–India deal and the annual budget are measures that will boost growth in the long term and hence keep us constructive.

Conclusion

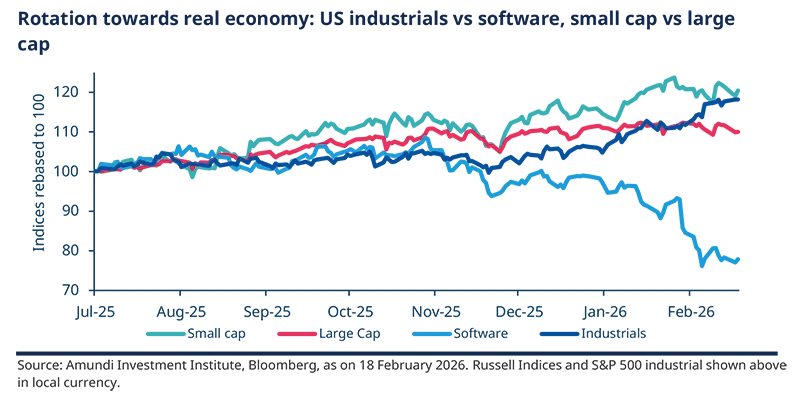

We think diversification and flexibility will continue to be key in enhancing portfolio resilience and long-term returns. The macroeconomic environment appears increasingly resilient, but with changing policy transition dynamics and strong market rotations that will continue to affect market behaviour. Given this backdrop, we see a late cycle environment continuing this year and therefore maintain a moderate risk on stance. Within this stance, we expect a rotation towards real economy sectors such as industrials (as outlined in the chart) and dispersion across regions and asset classes.

Secondly, high valuations of risk assets constrain our ability to raise our risk stance. Valuations alone, however, are unlikely to trigger a major correction. Instead, triggers would more likely arise from liquidity tightening or a deterioration in credit conditions.

Authors