Summary

The message is clear for Warsh’s new Fed: prioritise price stability to preserve credibility, while also creating task forces to adapt monetary policy to a changing world.

A new Fed era under Warsh

The Fed left interest rates in the range 3.5% - 3.75%, a widely expected outcome. The decision to hold was unanimous.

Warsh was clear in saying that the Fed will prioritise price stability, but he also announced task forces on reforms crucial to the conduct of policy.

With no forward guidance, investors will need to delve deeper into the data to gain insight into monetary policy actions.

The Fed left interest rates unchanged at Kevin Warsh’s first meeting as the new Chair. Warsh was explicit that the FOMC will prioritise delivering price stability, which was also reflected in the policy statement.

One sign of a new regime of monetary policy was the announcement of five task forces. These include efforts to examine the Fed’s framework for inflation analysis, productivity, how it issues communications, data sources, and, most importantly, the balance sheet. The latter has significant implication for market liquidity and the US dollar, given its enormous size.

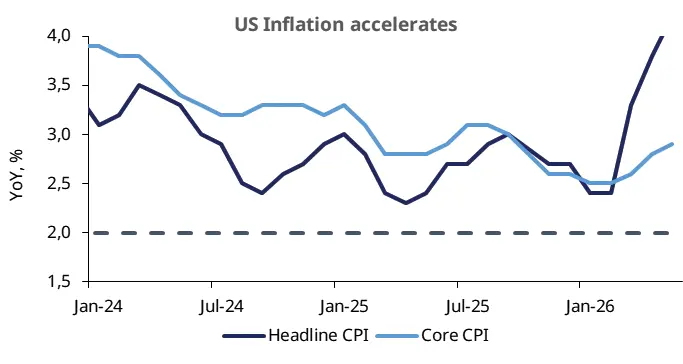

The focus on inflation is paramount: recent data have already highlighted the increase in producer price and headline inflation, with core inflation that could follow with a lag. The intensity of pass-through is important for implication in terms of corporates margins and consumers’ real income.

This week at a glance

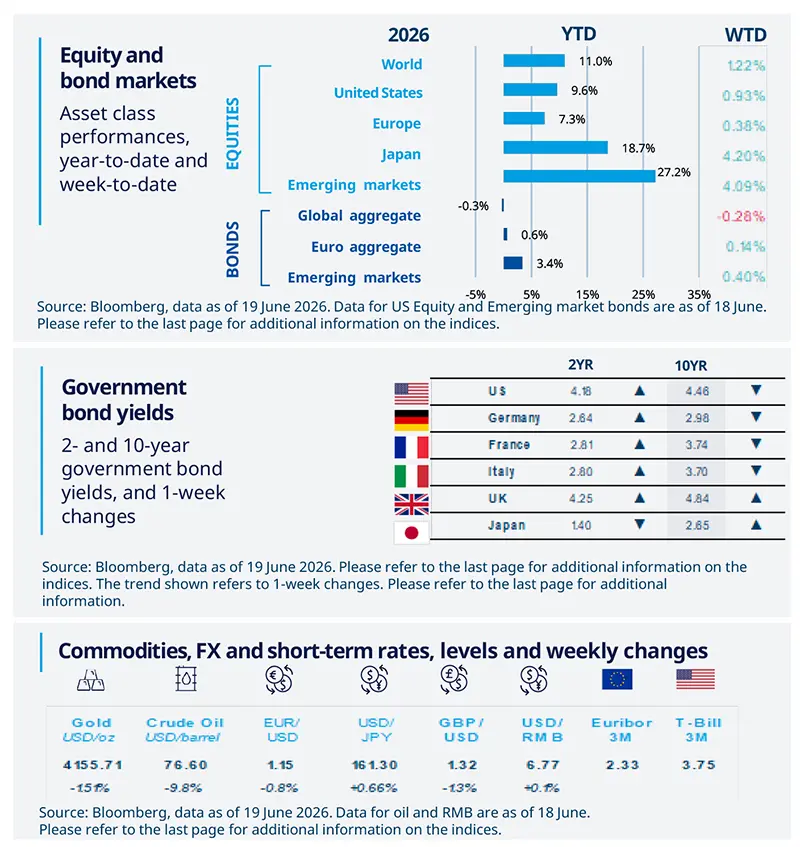

Equity markets rose on optimism generated by the Iran–US deal. In fixed income, short term US yields rose as the market is now pricing in more Fed hikes than before. Warsh’s comment gave a boost to long-term Treasuries, as they are more sensitive to inflation expectations. Oil fell on hopes of a gradual reopening of the Strait of Hormuz to traffic. The dollar surged while gold fell.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 19 June 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US manufacturing momentum holds up

US industrial production rose just 0.1% month-over-month in May, with flat manufacturing output showing the sector is still feeling some pressure from higher oil prices. But the underlying trend remains solid: manufacturing output is still growing at a solid annualised, based on recent three-month trends, pointing to an ongoing cyclical upswing. Durable manufacturing rose, led by autos and metals, and AI-linked high-tech manufacturing remained strong. A lasting normalisation of shipping through the Strait of Hormuz could support the sector further.

Europe

Eurozone inflation still sticky

Eurozone inflation held at 3.2% in May, up from 3.0% in April, while core inflation was revised up to 2.6%, driven by services. The higher core reading in the flash estimate had already raised concerns about inflation “broadening out,” a point recently highlighted by the ECB when it hiked rates. Energy inflation remained elevated, while food inflation eased. Overall, this suggests inflation is still sticky, which may keep the ECB cautious. Meanwhile, a deal to reopen the Strait of Hormuz has helped push oil prices lower, but gas prices remain a risk.

Asia

BoJ raises rates, but stays on gradual path

The Bank of Japan raised its policy rate by 25 basis points to 1.0% and will likely continue a gradual hiking path. The Central Bank cited government relief measures and efforts to secure supplies of raw materials as key supports to Japan’s growth outlook, making the risk of a significant economic slowdown less likely. Despite positive global tailwinds, such as the reopening of the Strait of Hormuz and lower oil prices easing global inflationary pressures, Japanese Government Bonds are lagging the global bond rally.

Key Dates

Eurozone PMI, US PMI |

US Personal Income |

ECB CPI Expectations, US Consumer Confidence |

Authors