The Iran crisis reinforces a structural shift that we have been highlighting: geopolitics is becoming a recurring macro driver again. We are moving further into a “controlled disorder” environment, where shocks generate rotation and dispersion rather than a uniform market direction, as referenced in our latest Global Investment Views.

We see oil as the transmission channel to economy and markets. Current oil price level embed the shock. Without a Strait of Hormuz disruption, sustained oil prices above USD 100 are unlikely — and paradoxically, if prices reached those levels, demand destruction and recession risks would quickly cap the move. We read this primarily as a temporary stagflationary impulse, not a new oil super-cycle.

As long as oil flows continue, this remains a volatility event, not a systemic one — but it confirms that geopolitics is now structurally embedded in the investment cycle. In the short term, it feeds inflation risk, USD strength, and asset-class dispersion. Energy volatility, inflation uncertainty, and regional dispersion are returning as defining market features.

Asia and EM oil importers face tighter financial conditions and weaker external balances. Europe is more sensitive to gas due to lower storage levels but should normalize seasonally. The US remains relatively insulated, benefiting from its energy exporter status and safe-haven flows.

Investment implications: gold is the clear winner across scenarios while US assets should remain relatively resilient. EM will see winners and losers: oil importers are the most vulnerable, while commodity exporters could benefit. Credit risks are contained but skewed toward lower quality borrowers.

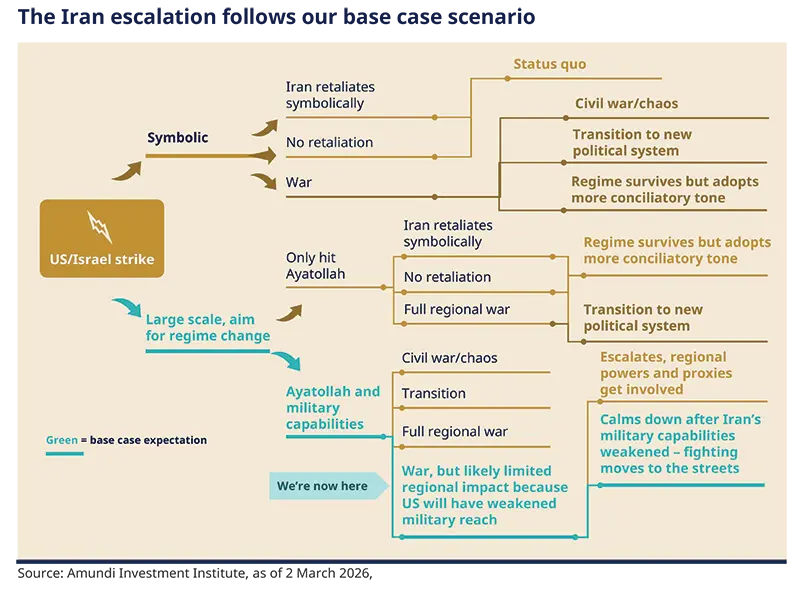

What is the nature of the attack on Iran and how could the situation evolve?

Nature of the shock – The US and Israel hit Iran in a large-scale attack, aimed at the Ayatollah, regime infrastructure, and military targets. We think this is a targeted geopolitical escalation, not yet a regional war.

Potential evolution – Over the short term (days and weeks), we will likely see continued strikes, while Iran retains its missile capability. This implies an elevated risk of retaliation, and markets could react mainly via spikes in volatility. In the medium term, the developments will depend on the involvement of other Gulf states and Iranian proxies, possible disruptions in the Strait of Hormuz, and internal instability in Iran.

Regional dynamics signal containment – Regionally, we think Hezbollah has been weakened and we expect the involvement of other Iranian proxies to be limited and only tactical. Moreover, the Gulf countries want a rapid de-escalation because economic stability is their priority. Outside the region, Russia and China will also be cautious. Overall, escalation risks exist for as long as Iran can retaliate and resist, but incentives for other major parties favour a containment of the crisis.

The length of the conflict depends on the extent of Iran’s missile capabilities. There are some reports that Iran’s missile capabilities may already have been halved. The indiscriminate Iranian attacks right now, firing in all directions, are likely a sign of distress rather than a well-coordinated military strategy, similar to a retreating army employing ‘scorched earth’ tactics: burning down anything to create as much chaos as possible.

How have the markets reacted?

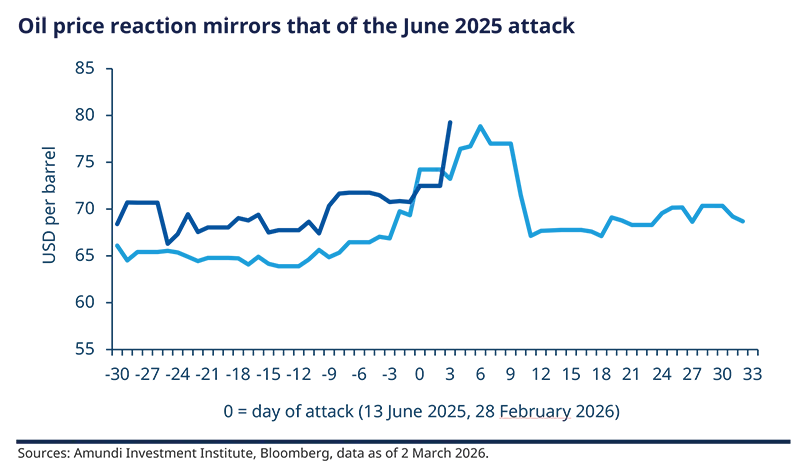

The current episode highlights the market’s sensitivity to geopolitics and rising oil prices, with a clear stagflationary impulse. The reaction is typical of past energy shocks: oil is up, with Brent surging from $72 to $79 a barrel over the weekend.

Equities are down, with major indices losing more than 2% in Europe, and Japan closing with the Nikkei down 1.4%, while the US market is holding well. Safe haven demand has pushed gold prices to a new record at around $5,390 and caused the USD to strengthen, while bond yields have been rising globally on perceived higher inflation risk.

Looking ahead, the nature of the shock is what matters most. If oil’s rise is temporary (our base case), the current trajectory — still a risk-on environment with a strong focus on diversification and hedging — remains intact.

The oil price surge is the key conduit for reassessing the macro outlook, as a prolonged shock would act as a stagflationary impulse — raising inflation, tightening financial conditions, and slowing global growth.

What is the macroeconomic impact of the current war

At the front of the recent events in the Middle East, the key conduit to revisit in the macro scenario is the oil price surge. A prolonged oil shock acts as a stagflationary impulse — driving higher inflation expectations, tightening financial conditions, and slowing global growth. This would particularly affect net oil importers in Asia and Europe.

So far, the air strikes have sharply increased oil’s risk premium, while we await a more persistent oil supply disruption to come through. Risk premium already priced in over the last weeks has further increased, taking the price just north of $80/barrel; major and persistent disruption could take the price towards $100/b or even higher.

The Strait of Hormuz, which handles 20% of global oil shipments, has been halted due to aerial strikes. Iran’s oil sales — primarily flowing to China — are likely to be shut down, and OPEC+’s planned output increase as well as the oil supplied by pipeline from the region is insufficient to offset the lost supply. Other commodities are also affected: fertiliser (impacting India, Brazil, Australia), aluminium (Middle East to Europe), liquified natural gas (LNG), and gold.

In particular:

Stagflationary impact – If oil prices persistently stay around $100, global inflation could rise more than 0.5% on average, while every $10 increase in oil could imply a 0.1–0.2 percentage point drag on global growth. The duration of the Strait of Hormuz halt will be critical in determining the overall impact.

No immediate response expected on monetary policy – Central banks should look through the shock, anticipating that weaker demand will help cool inflation. In that sense, our base case is already positioned on a continuation of the easing by the central banks that still have room to cut. We have recently postponed the next cuts by the Fed and the ECB due to their growth/inflation dynamics and we don’t envision any change in this timeline right now.

Regionally, there will be both winners and losers. Terms of Trade dynamics will play in favour of net oil exporters in emerging markets. Asian oil importers are more exposed to risks.

China has reserves and alternatives and it’s going through a fast electrification process. It is also the most important consumer of Iranian oil, but Iran is not a very large supplier for China, although Iranian oil is cheaper.

For India, the impact of net oil imports should be less severe than in the past on fiscal and current account. The share of oil in CPI basket is low vs other countries (6%) therefore we see a lower impact on inflation. With limited inflation transmission, RBI should maintain a neutral stance, carefully watching the impact on growth. Importantly, factors such as lower US tariffs, major trade deals with other countries and strong commitment to fiscal consolidation support our high conviction on India from a long term structural perspective.

Europe is not as exposed to Middle Eastern gas as Asia but storage this winter in Europe has been lower than in recent years and this explains today's European gas price reaction (+27%). Europe is vulnerable to rising oil and gas prices and some countries such as Germany have not solved its energy dependency yet. A more structural blockage scenario is clearly more impactful at the macro level for China and India.

All in all, our macroeconomic forecasts remain unchanged, as the base case assumes a temporary oil spike. The main takeaway for markets is that the disinflation narrative is now more fragile, and the Fed’s reaction function may become less dovish.

The current episode confirms a transition towards a world where geopolitics feeds inflation risk and leads to wider asset-class dispersion.

What are the investment implications of this war?

From a cross-asset perspective, gold is confirmed as a structural diversifier, and more generally, commodities and commodity currencies are favoured. Credit risk remains broadly contained, and the lower quality is more fragile. Selection is becoming even more relevant. This is particularly true in emerging markets, where oil importers are the most vulnerable in this phase. We provide more granular views on asset classes below:

Fixed Income – Fixed income yields have been falling in February, driven by concerns over equity valuations, growth, and rising geopolitical risks. The US 10Y dropped below 4%, hitting a year-to-date low. After the attack, yields have edged higher across the curve as fears of inflation reacceleration grow. Higher oil prices are complicating the easing narrative; oil around $80 could mean delayed cuts and higher inflation breakevens, while if oil moves above $100, we could see a risk-off scenario, leading to lower long-term yields. Overall, we remain cautious on US duration, as the rally looks advanced and supply is strong. We continue to seek diversification in Japanese and European bonds, particularly in the periphery. Spreads in credit markets are widening slightly, as markets become more selective.

Equities – In equities, we are witnessing strong market rotations. Energy is rallying while more cyclical sectors are coming under pressure. Regionally, the US equity market could benefit in the short term because it is less dependent on foreign energy compared to Europe or Japan which are also coming from a strong market performance. In addition, because industrials are energy users, they may also suffer in the near term. However, the underlying trends in favour of industrials and towards global diversification still hold, as we move to the next phase of the technological wave —from AI applications in language (LLM) to AI development in the physical world. Hence, the current market actions may open up opportunities to add further into strategic winners such as industrials.

USD – A surge in oil is a necessary but not sufficient condition for the USD to find a bottom and reverse its weakening structural trend. For that, we need US yields to rise ahead of inflation expectations — i.e., the market must believe the shock will push the Fed under strict inflation control, as happened in 2022. Our strategic view remains for a weaker USD, predicated on curve steepening and growing alternatives to US assets.

Emerging markets are a heterogeneous group, which will see some winners (it is not only oil prices but broader on commodities and this will be a plus for some countries). At a sector level in EM, energy and defence sectors could outperform on higher oil price and increased defence spending, while consumer cyclical sectors (tech, retail, autos) could lag sharply due to slower consumer demand and rising input costs. For EM debt, oil prices and volatility spikes will be key as any risk-off phase penalizes countries with low credit rating. This means, we will see wider spreads (current level is at fair value but we may see a sell-off in some cases), and higher refinancing stress. In FX, countries that are oil importers are the ones most exposed, whereas currencies of oil exporters will be more resilient.

Oil target unchanged – It’s reasonable to expect volatility and rising prices for oil even if current levels had already started to price in geopolitical risk and potential supply disruption. At the time of writing on 2 March Brent already reached close to $80/b. We maintain our target range (for this year) at $60-$70/b, provided Iran's oil infrastructure is not affected and the Strait of Hormuz is not significantly blocked. Additionally, OPEC may be willing to announce more production increases in the coming months, providing a further buffer and avoiding significant supply disruption. In precious metals, gold is a clear winner in all the scenarios and we confirm that it would be supported by demand to hedge geopolitical risks.

Conclusion

The escalation in the Middle East confirms the “controlled disorder” regime, where geopolitics has re-emerged as a central macro driver, energy volatility is a key pricing factor, and cross-asset correlations remain unstable. Country and sector dispersion is set to increase. Ultimately, the key question is not the risk of military escalation, but whether oil supply disruption becomes persistent. As long as flows continue, markets will face ongoing volatility rather than a structural bear shock. However, this episode highlights a transition towards a world where geopolitics systematically fuels inflation risk and greater asset-class dispersion.