Summary

The debate is no longer simply about slower growth and sticky inflation, but about a world in which policy, security, industrial strategy and capital markets are becoming increasingly intertwined.

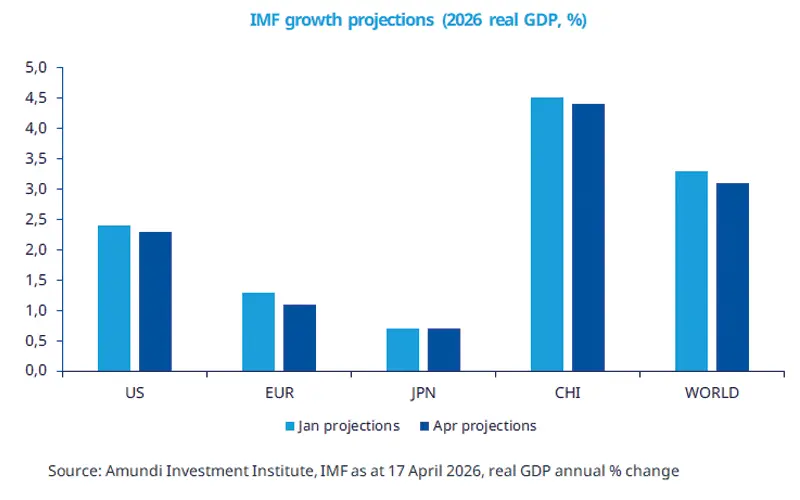

The latest IMF projections highlight that resilience to economic and geopolitical shocks has become a key variable for economic growth.

We think supply chains, energy independence, defence capabilities, infrastructure and access to critical raw materials will drive growth, inflation and asset allocation.

A consequence of these relationships is that policymaking will become difficult.

The IMF’s latest forecasts highlight that the global economy is still growing, but it has become more fragile. Before the recent conflict, economic growth was improving, whereas higher energy prices and greater uncertainty are now slowing that growth momentum.

For investors, the main point is no longer just weaker growth, but the risk that more expensive energy keeps inflation higher for longer and makes markets more volatile. The main themes to watch are therefore the path of oil and gas prices and the length of time for which they stay high. Secondly, investors should watch whether inflation starts to rise again, and whether central banks are forced to remain cautious for longer. Overall, the conflict reinforces our view of shifting traditional alliances, supply chain reallocation and diverging economic growth across regions. This mix is not neutral for markets and points to greater selectivity.

This week at a glance

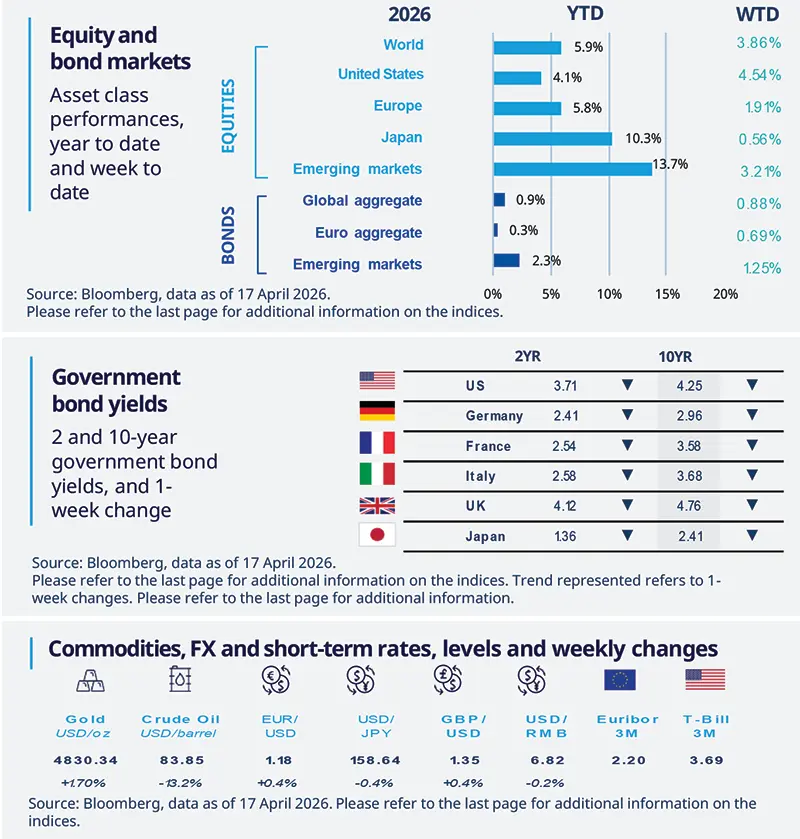

Global equity markets climbed to all-time highs on signs US and Iran may extend a ceasefire. The US corporate earnings season also boosted sentiment. Lower oil prices eased concern about inflations, which have made central banks more likely to hold interest rates steady for longer, pushing down yields. Gold prices rose over the week.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 17 April 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US small firms stayed cautious

Small business sentiment fell sharply in March, dropping below its long-term average on weaker earnings and softer expected business conditions. Hiring plans were flat, suggesting unemployment may peak later this year, wage growth eased, and capital spending slowed. While credit conditions stayed stable and prices rose slightly, plans for further price hikes and inventory buildup weakened, reflecting cautious business outlooks. The index, often used as a proxy for middle-income consumer conditions, points to a cautious outlook for demand.

Europe

Eurozone industrial recovery remains weak

In the EZ, industrial production rose by 0.4% MoM in February, rebounding from January’s decline. Germany and France saw slight declines, Italy marginally edged up, and Spain remain broadly unchanged. Growth was led by intermediate, capital and non-durable goods, while energy and durable consumer goods declined. However, production was still down 0.6% YoY, showing that the industrial sector’s recovery is far from complete and remains sluggish.

Asia

China data mixed

China’s Q1 GDP rose by 5.0% YoY, beating expectations on back of strong exports, recovering investment, and resilient industrial production, with retail sales showing early signs of stabilisation. Despite some March activity softness due to Lunar New Year seasonality and persisting property market weakness, inflation trends are improving. Against a backdrop of geopolitical risks and supply-chain concerns, we expect policy to remain broadly steady, with no rate cuts this year and only targeted support measures.

Key dates

Germany ZEW, US Retail Sales |

Korea GDP, Eurozone PMI |

Japan CPI, UK Retail Sales, Germany IFO |

Authors