Summary

Emerging markets offer a diverse set of opportunities driven by commodity exporters, technology leaders, and domestic demand. Despite the Middle East conflict, the diverse EM universe offers areas of strong economic growth and earnings resilience.

- EM equities have held up despite the Iran war, helped by strong earnings growth and the rally in the technology sector.

- Earnings growth underpins EM resilience, and the region is attractively priced compared to developed markets and offers diversification opportunities.

- Latin America stands out favourably, given its energy exports, strong fundamentals and its distance from the conflict region.

Earnings growth expectations have been improving across the emerging world, which remains a diverse universe of opportunities. Although the crisis in the Middle East caused initial volatility, at a broader level, the region seems to have recovered well. The situation remains fluid, but we see substantial long-term opportunities. For instance, in EM Asia, South Korea is one of the most attractive markets, supported by strong earnings momentum, AI-driven memory demand and governance reforms. China, however, faces a less supportive earnings backdrop. While we have a positive long-term view on India due to robust economic growth, solid earnings and reasonable valuations, near-term uncertainty could persist because of the crisis. Latin America, as an exporter of energy, offers a positive backdrop, supported by natural resources, central bank flexibility and some AI-related upside. Brazil’s outlook is constructive, but we are monitoring inflation, government debt and the 2026 election. Overall, we remain constructive on EM, particularly in Latin America and Asia.

This week at a glance

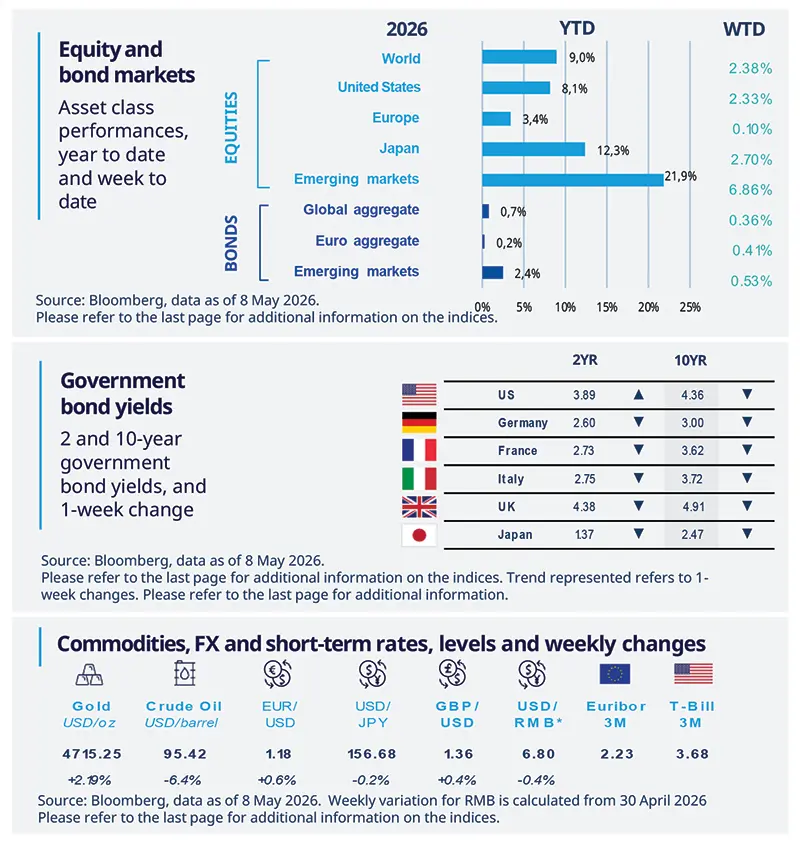

Global stocks rose over the week due to robust corporate earnings and expectations of a US–Iran deal. The latter also led to a fall in oil prices. Equities in emerging markets rose substantially on the back of optimism around the artificial intelligence theme, for instance in markets such as South Korea. Bond yields in most countries, except the US short term, declined, while gold prices rose.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 8 May 2026. The chart shows the price of gold.

* Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US investment activity remains firm

As per the final data release, US durable orders data confirmed a rise of 0.8% MoM. Although the dynamic differs between defense orders, which are increasing, and non-defense orders, which are declining, the positive signals for business investment remain intact. The core index, which excludes defense and aircraft orders, rose by 3.3% MoM, with related shipment increasing by 1.2%. Overall, the data suggest firm underlying investment activity, particularly in technology and machinery, and a positive outlook for US business spending.

Europe

Germany’s industrial recovery is delayed

Industrial production in Germany fell by 0.7% MoM in March. While output in energy and machinery declined, the automotive and construction sectors posted modest gains. Output in energy-intensive sectors rose by 1.2%, as higher oil and gas prices have yet to feed through to electricity prices. Despite improved efficiency and the closure of less productive operations, which may leave German industry less exposed to energy shocks than in 2022, high energy costs and structural challenges continue to weigh on the recovery, offsetting some support from fiscal spending.

Asia

Asia’s uneven inflation response to the oil shock

Asia’s response to the oil-price shock has been uneven, as higher fuel costs pass through according to each country’s fuel pricing mechanism, not just its exposure to global oil. Regulated markets can cushion the impact through price caps, stabilisation funds, state-owned absorption or tax relief, while liberalised markets such as the Philippines see faster pass-through to CPI. Inflation pressures are stronger where pricing is freer and fiscal buffers are thin, while many Asian central banks can keep rates steady. FX pressure and weaker growth further widen policy divergence.

Key dates

CPI: US, Brazil, India; EZ Zew Survey |

EZ industrial production, Brazil retail sales |

US retail sales, US labour market, UK GDP |

Authors