Gold has undergone a meaningful sell-off in recent weeks, but we believe the move has been driven more by a repricing of short-term macro fears than by any deterioration in the metal’s medium-term fundamentals. In our view, the market has largely been recalibrating expectations around a 2022-style scenario: a sharp inflationary shock, an aggressive central bank response, and a sustained rise in both nominal and real interest rates. That framework, however, does not fully reflect the current environment.

The recent correction was amplified by technical factors. In particular, the unwinding of ETF positions accumulated by retail investors and CTAs in March exacerbated the downside move and added momentum to the decline. As often happens in crowded trades, once prices began to reverse, the selling pressure became self-reinforcing. Yet this type of move typically says more about positioning than about a lasting shift in the fundamental outlook.

We do not believe the current economic backdrop is comparable to the one that prevailed four years ago. At that time, massive fiscal support across several regions, combined with post-pandemic supply disruptions, led to a sharp acceleration in core inflation well above central bank targets. That forced monetary authorities to react aggressively in order to anchor long-term inflation expectations. Today, the picture looks different. Core inflation remains more subdued and better contained, reducing the need for central banks to pursue an even more hawkish stance. In our view, the inflationary impulse triggered by the energy shock is likely to prove temporary rather than persistent.

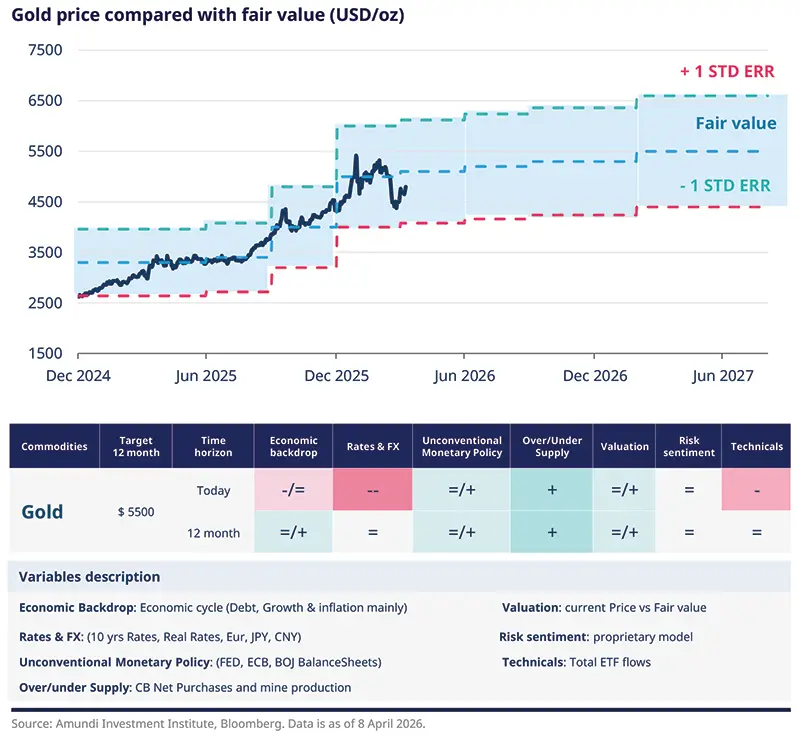

We remain constructive on gold, with potential for prices to move towards $5,500 over the next 12 months.

Looking ahead over the next 12 months, we remain constructive on gold and see potential for prices to move toward $5,500. Our positive outlook is based on several structural supports. First, central bank demand is likely to remain strong, especially among emerging market authorities that continue to diversify reserves away from traditional currencies. We do not see this trend reversing anytime soon. Gold remains a strategic asset for reserve managers seeking to reduce dependency on the US dollar and enhance portfolio resilience.

Second, mine supply is unlikely to keep pace with long-term demand trends. Structural supply constraints should continue to limit growth in new production, while official sector buying remains an important source of support. Third, rising global debt levels are becoming an increasingly important backdrop for gold. Ballooning sovereign and private leverage reinforces the appeal of hard assets and strengthens gold’s role as a store of value.

In the near term, some central banks may choose to use part of their gold holdings tactically to defend their currencies amid heightened volatility, including risks stemming from geopolitical tensions in the Middle East. While such actions are possible, they should not be interpreted as a sign of a structural shift away from gold. Rather, they reflect short-term policy management in a more uncertain environment.

Gold remains an effective protection against systemic risk, currency weakness, and policy uncertainty.

Ultimately, we continue to view gold as a valuable safe-haven asset. It is not a universal hedge against every market shock, but it remains an effective protection against systemic risk, currency weakness, and policy uncertainty. With prices already down roughly 15% from recent highs, much of the near-term bad news appears to be reflected in valuations. As a result, the downside linked purely to rate fears now looks more limited than it did at the start of the correction.

Authors