Summary

Key takeaways

|

AI techniques are increasingly being used in retail investor analysis and advisory tools. By capturing complex non-linear relationships and incorporating unstructured data such as text and images, they can better reflect the multiple factors that drive investor behaviour. These insights can improve investor segmentation and behaviour prediction, enabling more targeted coaching and personalised advice. In addition, robo-advisors, recommender systems and LLMs offer promising avenues to enhance investors’ decision-making and engagement. 2

This paper presents work undertaken to improve investor understanding, communication and service. It also outlines several real-world cases drawn from our experience and reviews the latest relevant academic insights.

Monica DEFEND

“AI advances research by enabling deeper analysis of investor behaviour and market dynamics, transforming complex data into behavioural insights that drive smarter finance for retail investors.”

Gaining deeper insights into investor behaviour

In our research, we have been using clustering – an unsupervised machine learning (ML) method - to identify subtle, behaviour-driven investor groups from complex datasets. This helps uncover hidden financial needs and decision drivers.3 Another initiative shows that synthetic surveys can fill gaps in investor data and enable rapid testing of messaging and product concepts across diverse investor profiles. Finally, academic insights highlight the potential of natural language processing (NLP) and LLMs to extract insights into investor preferences and behaviours.4

Clustering algorithms for investor segmentation

Clustering algorithms provide a data-driven approach to investor segmentation using high-dimensional datasets that combine demographic, transactional and behavioural information. Unlike traditional segmentation that is based on predefined categories (e.g., age, income, or risk profile), clustering groups investors by similarities in their overall profiles, uncovering more granular and behaviour-driven segments. In our research, we applied clustering techniques on a granular dataset of clients from Crédit Agricole du Languedoc to build comprehensive investor profiles based on demographics, consumption patterns, savings and investment behaviours.

In this study, how was AI helpful in clustering investors?

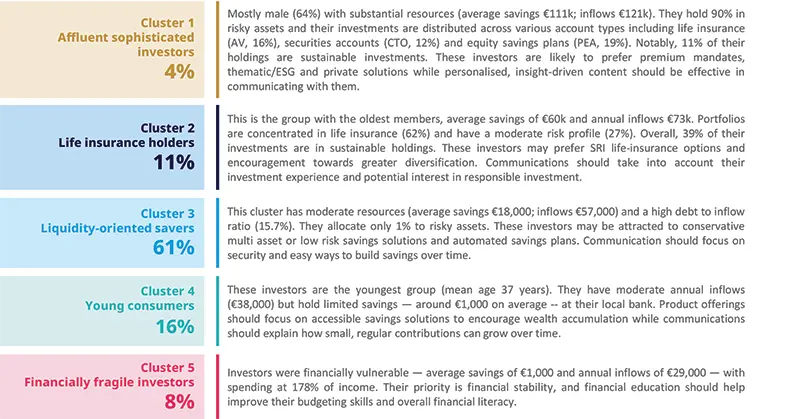

We used a two-step clustering approach to gradually reveal meaningful investor groups. First, each group was repeatedly divided until the split clearly improved the quality of the segmentation and produced reasonably sized sub-groups.5 This procedure revealed two macro‑clusters — ESG‑oriented Wealthy Investors (15.5%) and Non‑ESG Mainstream Savers (84.5%). In the next step, each macro-cluster was treated as a new dataset and recursively divided into two sub-clusters. This process produced a refined segmentation of five investor clusters — two SRI-oriented and three mainstream groups—offering a more granular understanding of investor profiles. These clusters were also matched with survey responses to provide deeper insights about clients’ financial sophistication, expectations and other unobservable aspects of their investment behaviours.

In the end, five distinct investor profiles were revealed.

What investor benefits came from AI-enhanced segmentation?

By clustering retail investors and combining the results with survey answers, we gained a better understanding of the major investor profiles within a bank’s retail base and were able to tailor support accordingly, through more differentiated product offerings and enhanced communication strategies.

“AI can help strengthen the connection between Amundi, our partners and retail investors — enabling more personalised interactions and a deeper understanding of client needs.”

Textual analysis enhances understanding of investors

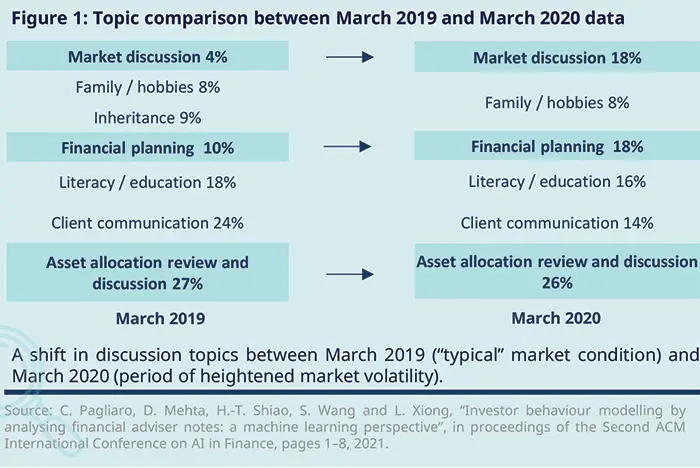

ML and NLP can also help predict retail investors’ behaviour. For example, they were used on advisers’ summary notes to identify investor concerns during market volatility and to better predict subsequent wealth‑eroding decisions.6 Figure 1 shows adviser‑note topic distributions for March 2019 and March 2020, revealing a marked thematic shift and indicating that qualitative insights predict investors' decisions to liquidate assets more effectively than transactional data can.

Related research suggests that NLP can be applied to broader forms of financial customer communication to enhance investor understanding. For example, studies have analysed textual interactions across customer contact points, including chat conversations and social media.7 Sentiment analysis and contextual language models were used to identify emotional signals and behavioural patterns in customer communication.8 This improved the interpretation of customer feedback and supported more personalised financial services and product recommendations. Similarly, other research applied sentiment analysis to banking customer feedback data to automatically classify customer opinions and identify areas for service improvement.9

These approaches enable advisers to detect concerns in advance and provide timely behavioural coaching. This can help investors avoid impulsive decisions during market stress and remain aligned with their long-term financial goals.

Fanny WURTZ

“AI is transforming how we understand retail investors — from precise behavioural segmentation to personalised coaching and recommendation engines. Our priority is to harness these capabilities to improve investor outcomes.“

Synthetic LLM surveys enhancing understanding of investors’ needs

LLM surveys are an emerging AI-driven approach that can make survey processes more efficient, reducing the time and cost of traditional market research, which often take months to complete. Work has been undertaken using a synthetic research platform to conduct market studies aimed at refining branding and communication strategies for responsible funds.

How did AI help in conducting the survey?

The project employed a synthetic research platform to gain market insights concerning fund names and communication strategies. The survey sample consisted of 1,805 AI-created respondents located in France (21.4%), Italy (21.4%), Germany (21.4%), Spain (21.4%) and Singapore (14.3%).

The platform conducted research on synthetic "personas"— AI-generated profiles built from the company’s knowledge of its target audience or segments. Each persona was a virtual individual with attributes ranging from demographics (age, gender, income, occupation) to personal preferences and behavioural tendencies. Personas were interviewed qualitatively or surveyed quantitatively, and their responses reflected their characteristics, experiences and preferences.

Comparing persona responses with human responses from the same market studies yielded an average correlation of 0.86, indicating that AI personas capture most of the underlying preference structure observed among human respondents.

“AI helps us understand investors at scale — behaviours, expectations and changing needs. Combined with our expertise and analytics, we deliver more relevant communications and experiences that put investors first.“

What are the benefits of an AI-driven survey for investors?

Using synthetic market surveys to shape branding and communications enables the provision of clearer, evidence-based information about what a responsible fund delivers. This approach simplifies decision-making and helps design wording that is both effective and compliance-approved.

LLM-enabled synthetic surveys for investor intelligence

Recent research highlights the potential of LLMs as tools for understanding investor behaviour, preferences and decision-making. For example, ChatGPT as a conversational product, has been shown to predict individuals’ preferences based on characteristics like income, gender and age, achieving a 70% correlation with human responses.10

LLM-generated synthetic respondents have been used to survey economic expectations (e.g., household inflation).11 By “freezing” model knowledge at specific dates, surveys can be rerun across decades to build historical panels of expectations and treatment effects. Financial institutions can use these to test how communication affects perceived risk and behavioural intentions across investor profiles, enabling clearer messaging and guidance for retail investors.

LLMs can also be used to generate economic forecasts from synthetic participants with forecaster attributes similar to those of real participants.12 The simulated panel reproduces key survey features — forecast accuracy, central tendencies, revisions and dispersion — but is sensitive to inputs: dropping forecaster characteristics has little effect, whereas removing real-time data degrades performance. Generally, this approach offers financial institutions a scalable way to understand expectations across different macroeconomic scenarios.

Recent research also explores the use of LLMs as behavioural agents in simulated financial markets. For example, LLM-based traders (instructed to act as value or momentum traders, or as market makers) can interact in a simulated market. These interactions produce dynamics, including price discovery and speculative bubbles.13 This allows researchers to test market responses to varying conditions. LLM-enhanced agents can also be introduced for financial market simulations that model human-like behavioural biases, including context-dependent loss aversion.14

These approaches suggest that LLM-based simulations could provide a flexible environment to explore how different types of investors react to market information, product design, or communication strategies, helping asset managers better understand investor behaviour and tailor investment guidance accordingly.

This emerging literature suggests that LLM-based synthetic surveys and behavioural simulations have the potential to complement traditional surveys and experimental methods for studying investor behaviour. However, evidence cautions against assuming that LLMs can reliably emulate human respondents. While generative models can produce consistent answers, they also exhibit “machine bias”— systematic yet unpredictable deviations from human opinion distributions, with low variance and topic-dependent biases.15 These findings suggest that LLMs cannot completely replace human subjects in attitudinal or opinion research, underscoring the need for careful validation when using synthetic respondents in behavioural and financial studies.

Investor advice and communication

Robo-advisors, chatbots (live conversational interfaces for real-time Q&A) and mailbots (automated email/messaging agents) could together enhance investor communication and advice. In particular, robo-advisors may encourage investors toward better decisions and higher levels of engagement while recommender systems powered by ML might help personalise further portfolio and stock suggestions. Mailbots automate investors’ routine requests and standardise responses, reducing waiting times and facilitating assess to account information. Chatbots complement them by offering interactive, real-time support that helps advisors or investors navigate platforms, understand financial concepts and products, and stay informed. Together, these tools could enhance service quality and investor satisfaction, reduce cost-to-serve and potentially improve portfolio outcomes.

Claudia BERTINO

“The convergence of robo-advisors, chatbots and mailbots represents more than a technological upgrade in investor servicing; it signals a structural shift in how advice is delivered, engagement is sustained, and value is created.”

Robo-advisors enhancing investment decisions

Our researchers found that robo-advisors could significantly influence investors’ decisions while allowing them to retain full control over their portfolios.16 The study examined the impact on investors’ decisions of introducing robo advisors in an employee savings plan.

What are robo-advisors?

Robo‑advisors range from simple rule‑based tools to advanced ML systems for investor profiling, portfolio construction, personalisation and virtual assistance. They automate portfolio management either fully or via an advisory, human‑in‑the‑loop model where algorithms generate recommendations, but investors make the final decisions. The employee savings plan involved in the research adopts the latter, offering algorithmic recommendations while keeping the investor ultimately in control.

How do robo-advisors work?

The robo‑advisor collects investor details (risk aversion, experience, investment horizon, etc.) to build a profile and recommend a portfolio from the employer’s fund menu. Investors can compare the proposed and their current allocations by asset class and fund. If they accept the recommendation, the robo‑advisor implements the changes, continuously monitors portfolio drift and sends email alerts with rebalancing recommendations that investors can choose to accept or ignore.

How do robo-advisors enhance investment outcomes for investors?

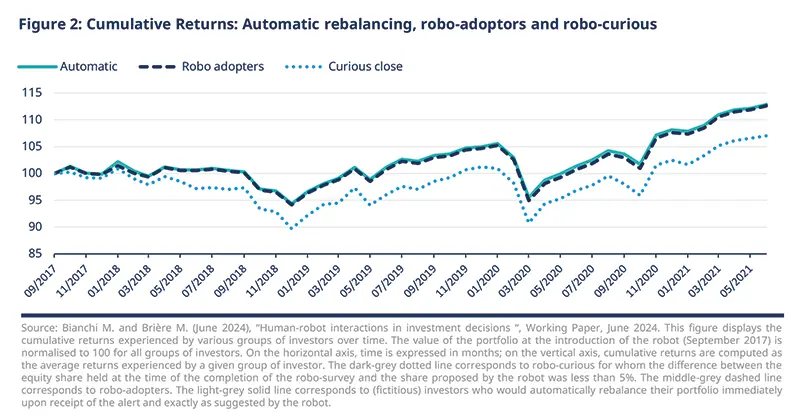

The research found that robo-advisors significantly influenced investors’ decisions while leaving them in full control. Engagement rose — logins and trading increased and stayed elevated after subscription. Following subscription, investors increased their equity allocations by 3% (from an average of 22%) and started to rebalance their portfolios regularly. Annual risk‑adjusted returns improved by roughly 2% (net of fees) over the 2016–2021 period. Alerts proved especially effective: robo-adopters who received one were 29% more likely to rebalance, compared with a 10% baseline rebalance rate. As shown in Figure 2 below, the returns that would have resulted from automatic rebalancing by the robot were only slightly higher than those experienced by robo-adopters. This suggests that, on average, allowing investors to retain control does not impose a large financial cost, while potentially fostering greater trust in the service.

Marie BRIERE

“By combining robo-guidance with investor choice, the service boosts engagement and improves portfolio discipline without materially sacrificing the value of human control.”

Recommender systems enabling more tailored recommendations

Recommender systems (RSs) are applications designed to predict a user’s preferences; they often use ML models to make these predictions and determine the most relevant recommendations. Within the financial industry, they can offer personalised recommendations for portfolio allocation or stock selection, but a significant challenge is the lack of granular information about investors’ preferences. To overcome this, ML techniques, such as case-based reasoning, have been used to improve recommendation accuracy.17

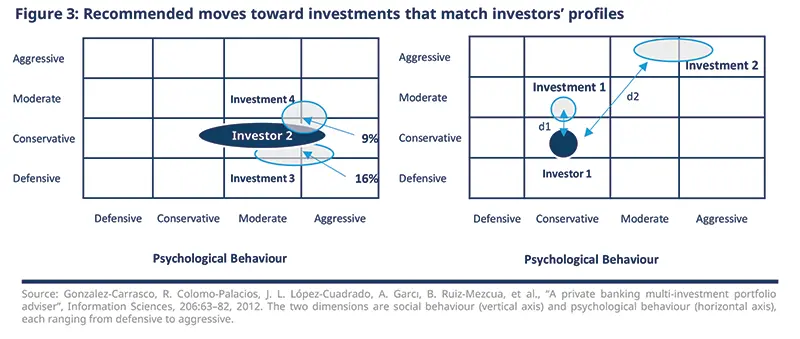

Asset allocation recommendations can be, for example, provided based on a library of past “cases,” each containing information about an investor, the portfolio recommended by advisers and its performance. When a new investor seeks advice, the system identifies similar investors and their associated portfolios. These candidate portfolios are then refined through clustering, ranking and filtering to generate tailored recommendations. In Figure 2 below, investors are represented as points in a two-dimensional behavioural space (social versus psychological characteristics), while investment products are plotted according to their attributes. Recommendations are based on proximity: products located closest to an investor’s point — i.e. those with the smallest distance are considered the best match.

On the left-hand chart, the percentages (9% and 16%) represent the dissimilarity between investor 2’s profile and the investment options, so investment 4 (9%) is a better fit for investor 2 than investment 3 (16%). On the right-hand side, investment 1 is closer to investor 1’s profile, thus it is a better match than investment 2.

Recent research extends these RSs by integrating LLMs, reinforcement learning and investor-specific risk modelling to generate adaptive portfolio strategies.18 The system uses a conversational financial agent to collect investor preferences, Bayesian methods to infer risk tolerance and a reinforcement learning engine to optimise asset allocation under changing market conditions.19

However, applying RSs in finance raises several important challenges. For example, RSs may reinforce behavioural biases or reduce diversification when they are based on past investor behaviour or similarity‑based approaches. Moreover, investment decision‑making is inherently complex and requires clear, actionable explanations to help users critically evaluate recommendations before accepting them. Unfortunately, many systems fall short in terms of explainability. Some RSs — particularly those that rely on complex algorithms — function as “black boxes,” raising transparency concerns and undermining investor trust. This opacity also complicates regulatory oversight, making it difficult to assess the risks and impacts associated with these systems.

"AI is transforming what we do. It lets us innovate quickly and deliver scalable solutions that make investing more intuitive, efficient and accessible to retail investors.“

Enhancing client communication through mailbots

Asset managers can benefit from adopting mailbots to automate routine client enquiries at scale and freeing service teams to focus on complex and value-added interactions.

What is an AI-driven mailbot and what are its main functions?

A mailbot automatically processes beneficiary emails: it analyses messages, identifies request types, and responds using a legally validated knowledge base. It handles common enquiries (such as withdrawal conditions, and plan features) and deals with common questions related to the general operation of employee savings schemes, delivering immediate, accurate responses that reduce waiting times and improves client service efficiency. 20

How do mailbots work?

The mailbot classifies beneficiary requests, extracts key details and generates responses using exclusively generative AI. Its knowledge base—manually compiled from validated FAQs, operational procedures and historical requests—is reviewed and approved by the Legal department to ensure accurate, consistent and compliant replies. Response quality is monitored daily across all requests by an LLM “judge” — an AI model that evaluates and scores responses generated by other AIs. These scores, combined with beneficiary accept/reject feedback and investor assessments, are analysed to enhance the knowledge base and trigger escalation to customer service when human intervention is required.

What are the benefits to investors of a mailbot?

A mailbot reduces manual workload and accelerates communications. This improves the investor experience and ensures timely support. Also, it frees customer‑service agents to focus on more complex or sensitive cases, enhancing overall service quality and communication.

Another area where AI benefits investor communication is the use of API platforms. These give investors real‑time access to data and portfolios, improving transparency and decision‑making. Furthermore, their seamless integration with investor systems reduces costs and supports personalised services.

Intelligent assistants for wealth management platform users

Advisors and asset managers can benefit from an API platform where investors’ portfolios, reports and accounts are accessible within a single integrated environment.

What is an API-based platform for digital investment services?

It is a system that enables different financial applications and tools to connect and share data seamlessly.

How does the chatbot work?

An AI powered chatbot has been integrated into the portal for API documentation, providing both functional and technical guidance. It is more than a simple search tool — it acts as an intelligent assistant that understands natural language and responds to the intent behind a question rather than individual keywords. It also retains conversational context, allowing it to clarify or expand on previous answers, and continuously improves over time through user feedback.

How does the AI chatbot help advisers and retail investors?

The AI chatbot can help advisers to use the platform more confidently, which in turn indirectly benefits retail investors as well—helping to ensure that the advice they receive is more accurate, personalised and grounded in a clearer understanding of the underlying analytics.

Dominic BYRNE

"AI has the potential to transform how we engage with clients on retirement, enabling more tailored conversations and helping make long-term planning more accessible and actionable.“

Transforming investor engagement with LLMs

In 2025, 51% of U.S. consumers reported using AI for financial advice or information in the past three months, and 52% of those users relied on ChatGPT.21 A similar survey conducted in Europe shows that 62% of European investors (in the UK, Germany, France and Italy) use AI tools to help with their investment decisions (with 22% saying they use them always or often).22

LLM-driven conversational agents are emerging as potentially useful tools for engaging with clients. They can provide advice based on an understanding of individuals obtained through dialogue.23 During such dialogue, potential investors can ask questions or express concerns; the agent actively elicits necessary information and guides them toward personalised investment options.

Although the quality of financial advice generated by LLMs has improved, recent research also highlights the potential risks associated with the use of LLM-generated advice in investment decision-making. For example, investment recommendations produced by LLMs may reinforce behavioural biases such as trend-following and portfolio concentration.24

Another study evaluated LLM-generated financial advice against a life-cycle consumption–savings model and found that, while the recommendations broadly align with economic intuition, they exhibit systematic deviations from optimal planning benchmarks. In particular, the advice relies on simple financial heuristics, exhibits excessive inertia in portfolio adjustments, and varies systematically with demographic characteristics and across identical queries.25

While LLMs are unlikely to fully replace human financial advisers anytime soon, their most significant impact may lie in their effectiveness as educational tools to enhance investors’ financial literacy, mitigate biases and prevent common mistakes.

Challenges with AI usage

Leveraging AI to accurately capture investor preferences and develop behavioural prediction models is promising but raises several challenges. To start, a lack of data on investors’ characteristics, styles and psychological dynamics can reduce model performance. Some sources, such as investors’ conversations with advisers, can significantly improve the predictive accuracy. However, this type of data may be inaccessible due to legal restrictions or individuals’ privacy-protective behaviour.26 In addition, the underlying data or case histories can be biased while current market or geopolitical developments, may not be adequately reflected. Generally, LLMs may be biased or lack the ethical safeguards required of human financial advisers.27

Companies involved in the development, distribution and use of AI systems in the EU must also comply with the requirements of the European Union Artificial Intelligence Act (EU AI Act), which aims to ensure that AI systems are transparent, uphold EU values and prohibit the use of manipulative AI techniques. In light of these challenges, it is critical that no single part of the investment process lacks human supervision.

Conclusion

Technology and AI can play a valuable role in improving investor outcomes within a framework that protects data and privacy. Asset managers already use these systems to identify investors’ needs effectively and deliver more personalised, data-driven insights. Distributors can benefit by offering targeted guidance and more efficient client engagement, while investors can take advantage of clearer recommendations, better decision support and improved financial outcomes.

Yet this is only the beginning, and several promising directions are emerging: (1) hyper-personalised nudges, which could deliver dynamically tailored behavioural prompts at precisely the right moment in a client’s journey, shifting the approach from reactive to anticipatory guidance; (2) affective AI and emotion recognition, where future systems could analyse vocal tone and facial expressions during client interactions to detect stress or hesitation before they lead to harmful financial decisions; and (3) human–AI collaboration models, in which AI does not replace financial advisers but instead equips them with real-time behavioural insights, allowing human empathy and AI precision to work in tandem.

Other research by Amundi

Brière M. and K. Huynh (2025), Artificial Intelligence for Behavioral Finance, Working Paper, November 2025.

Bianchi M. and Brière M. (2024), Human-robot interactions in investment-decisions, Working Paper, June 2024.

Brière M. (2024), How can human-robot interactions benefit financial decision-making?, Thematic Paper, June 2024.

Brière M. (2023), Retail Investors’ Behaviour in the Digital Age: How Digitalisation is Impacting Investment Decisions, Thematic paper, June 2023.

Bianchi M. and Brière M. (2022), "Robo-Advising: Less AI and More XAI?", in "Machine Learning and Data Science for Financial Markets: A Guide To Contemporary Practices", Ed. Capponi A. and Lehalle C.A., Cambridge University Press.

1A large language model (LLM) is a very big neural network pretrained on huge amounts of text to predict and generate language. It can perform many language tasks (e.g., generation, summarisation, Q&A, classification) and can be applied to natural language processing tasks.

2Robo-advisors are automated platforms that create and manage investment portfolios based on investors’ goals and risk profiles. Recommender systems are general algorithms that suggest products, content, or actions an investor may like.

3 Machine learning is a subset of AI that includes statistical techniques. With experience, these enable machines to improve at tasks.

4 Natural language processing (NLP) is the technology that helps computers understand and respond to human language.

5 K-mean is a simple method that splits data into K groups so that items in each group are similar.

6 C. Pagliaro, D. Mehta, H.-T. Shiao, S. Wang and L. Xiong, “Investor behaviour modelling by analysing financial adviser notes: a machine learning perspective”, in proceedings of the Second ACM International Conference on AI in Finance, pages 1–8, 2021.

7 Gottipati, Kalyan C. and Deepika Maddineni, "Personalized Financial Services Using NLP and Sentiment Analysis", 2025.

8 Contextual language models are AI models that understand and generate text by using the surrounding context of a word, sentence, or conversation — not just the word itself. Some contextual language models are large language models (LLMs), but not all of them.

9 Ekawaty, Anita, et al., "Utilizing sentiment analysis to enhance customer feedback systems in banking", 2024 12th International Conference on Cyber and IT Service Management (CITSM), IEEE, 2024.

10 A. Fedyk, A. Kakhbod, P. Li, and U. Malmendier,” ChatGPT and perception biases in investments: An experimental study”, Available at SSRN 4787249, 2024

11 Wu, Jing Cynthia, Jin Xi. and Shihan Xie, “ LLM Survey Framework: Coverage, Reasoning, Dynamics, Identification”, National Bureau of Economic Research Woking Paper No. w34308, 2025.

12 Hansen, Anne Lundgaard, et al., "Simulating the survey of professional forecasters", Available at SSRN 5066286, 2026.

13 Lopez-Lira, Alejandro, "Can large language models trade? Testing financial theories with LLM agents in market simulations", arXiv preprint arXiv:2504.10789, 2025.

14 Hashimoto, Ryuji, et al., "Agent-Based Simulation of a Financial Market with Large Language Models", International Conference on Principles and Practice of Multi-Agent Systems. Cham: Springer Nature Switzerland, 2025..

15 Boelaert, Julien, et al., "Machine bias. How do generative language models answer opinion polls?", Sociological Methods & Research 54.3 (2025): 1156-1196.

16 Bianchi M. and Brière M. (June 2024), “Human-robot interactions in investment-decisions“, Working Paper, June 2024

17 C. Musto, G. Semeraro, P. Lops, M. De Gemmis and G. Lekkas, “Personalised finance advisory through case-based recommender systems and diversification strategies”, Decision Support Systems, 77:100–111, 2015.

18 Li, Bangyu, Boping Gu, and Ziyang Ding, "LLM-based Personalized Portfolio Recommender: Integrating Large Language Models and Reinforcement Learning for Intelligent Investment Strategy Optimisation", arXiv preprint arXiv:2512.12922 (2025).

19 Bayesian methods are a simple way to start with a guess and then update that guess as one see evidence.

20 “Retail investors” refers to individual beneficiaries such as French employees whose accounts are administered through the employees retirement scheme

21 As More U.S. Consumers Struggle with Rising Prices, Many Turn to Articial Intelligence for Financial Advice, 28 August 2025, J.D. Power Insights.

22 Amundi and Yougov survey, November 2025.

23 T. Takayanagi, M. Suzuki, K. Izumi, J. Sanz-Cruzado, R. McCreadie and I. Ounis, “Finpersona: An LLM-driven conversational agent for personalised financial advising”, In European Conference on Information Retrieval, pages 13–18. Springer, 2025b.

24 Winder, Philipp, Christian Hildebrand and Jochen Hartmann, "Biased echoes: Large language models reinforce investment biases and increase portfolio risks of private investors", Plos one 20.6 (2025): e0325459.

25 Choukhmane, Taha, et al., "How good is generative AI personal financial advice?." (2025)

26 H.-T. Shiao, C. Pagliaro and D. Mehta, “Using machine learning to model advised investor behaviour”, The Journal of Financial Data Science, 4(4):2022.

27 A. W. Lo and J. Ross, “Can ChatGPT plan your retirement? Generative AI and financial advice “, February 11, 2024), 2024.

Authors