Summary

Key Messages

Clean-energy investment continues to expand

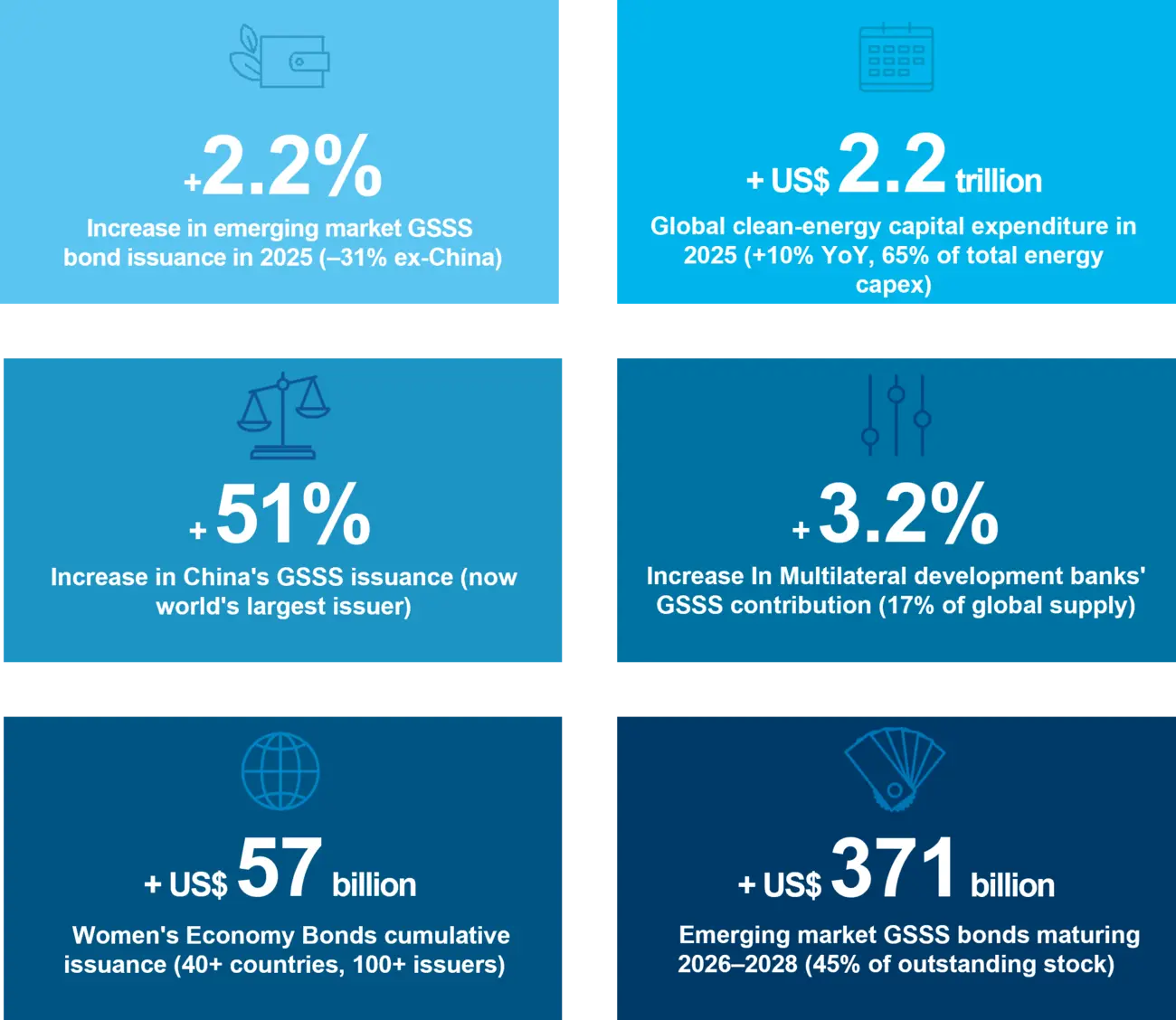

Global clean-energy capital expenditure reached a record $2.2 trillion in 2025, 10 percent higher than a year earlier and equivalent to 65 percent of total energy capex.

Modest headline growth masks a stark divergence

Emerging market green, social, sustainability and sustainability-linked (GSSS) bond issuance rose 2.2 percent to $186.8 billion in 2025. China surged 51 percent to a record $111.1 billion, becoming the world's largest issuer. Outside China, however, emerging market issuance contracted 31 percent, with the steepest declines in Latin America (–56 percent) and South Asia (–68 percent).

Sustainable bonds in emerging markets outside China lead in fixed-income share

Excluding China, GSSS bonds reached 2.6 percent of total emerging market fixed-income issuance in 2025, above developed markets at 2.5 percent. China’s share stood at 1.6 percent.

The labeled bond market in developed markets is maturing

The decline in labeled issuance does not signal a retreat from sustainable investment. Developed-market clean energy capex rose to $1.1 trillion, yet the share financed through labeled bonds fell from 48 percent to 35 percent. Issuers are not cutting on green investment. They are choosing not to label it as tighter disclosure requirements, political headwinds, and rising compliance costs have made labeling costlier without delivering commensurate benefits.

Supranationals provide a structural anchor

Multilateral development banks contributed $151.1 billion of GSSS bond issuance in 2025, around 17 percent of global supply and 3.2 percent higher than a year earlier. The supranational segment has remained largely insulated from the policy dynamics driving developed-market retrenchment, and its institutional mandates underpin a steady issuance pipeline.

The greenium has effectively vanished

The pricing advantage for issuers on green bonds fell below one basis point globally in 2025, down from an average of approximately 2.4 basis points over 2019–2024. In emerging markets, the greenium can no longer be distinguished from zero with statistical confidence. The economic case for labeling now rests entirely on non-pricing factors.

Policy architecture determines where labels survive

China's central bank lending facilities, broadened taxonomy, and macroprudential integration sustain labeling independently of market pricing dynamics. Southeast Asian authorities subsidize verification and documentation costs. In the Middle East, sovereign strategies tied to long-term economic transformation programs anchor issuance pipelines. Where these policy structures exist, labeled issuance grew. Where they do not, it contracted.

Strong financial performance, with caveats

Emerging market GSSS corporate bonds returned 10.4 percent in 2025, outperforming the broader index by two percentage points. However, the GSSS market is tilted toward higher credit quality and longer duration, and any performance differential likely reflects index composition rather than a pricing effect specific to the label.

Women's Economy Bonds reach scale

Cumulative issuance of Women’s Economy Bonds has reached $57 billion across more than 40 countries and over 100 issuers. Latin America and the Caribbean lead with 40 percent of volumes. Scaling the market further will require standardized bond principles, wider adoption of sex disaggregated data, and deeper market infrastructure in regions where issuance remains nascent.

A maturity wall threatens the outstanding stock

Approximately $371 billion in emerging market GSSS bonds will mature between 2026 and 2028, or 45 percent of the outstanding stock. Net issuance has already fallen from its 2023 peak of $187 billion to $91 billion. If maturing issuers choose not to re-label their refinancing, the total stock of emerging market sustainable bonds could contract for the first time.

Transition bonds and taxonomy interoperability are the key catalysts

The ICMA Climate Transition Bond Guidelines, published in November 2025, create a credible pathway sector that green bonds were not designed to serve. Progress on taxonomy interoperability and the European Union's (EU) flexibilization of its sustainable finance framework could lower cross-border issuance frictions. Whether these developments will be sufficient to offset the maturity wall and restore net issuance growth remains the defining question ahead.

Key 2025 Highlights

Author