Summary

Geopolitics is changing the investment playbook

Geopolitics is now a critical macro and market variable

Geopolitics shapes the backdrop for policy and business decision-making. It influences fiscal and industrial policy, public spending, inflation and interest rates. It shapes choices companies make, thereby affecting trade routes and supply chains too.

As recent events in the Middle East have shown, geopolitical developments can cause regime shifts, altering the market’s expectations on growth, inflation, liquidity, and policy responses.

In short, geopolitics can change the macro regime, the policy reaction function, the risk premia, and the winners and losers — and therefore capital allocation, risk management, and portfolio construction.

Geopolitics shapes investment trends

Geopolitical developments now influence where capital flows. Some of the strongest performing asset classes of 2025 — including gold, selected equities, and parts of emerging markets — were driven by geopolitical trends. This may seem contradictory through a traditional ‘risk on, risk off’ lens, but through a geopolitical lens, they are part of the same story: the search for alternative opportunities in a multipolar world, trust in gold as a store of value and spending on defence and AI, driven by uncertainty and competition.

While geopolitics shapes longer-term trends, asset class behaviour in the short term depends on which factor dominates the macro environment. Since the escalation in the Middle East, gold has been among the weaker performers, as markets priced higher inflation and the implications for interest rates — confounding its usual safe-haven reputation. Equities rallied on AI optimism, while oil outperformed on supply risk concerns.

The pattern is not contradictory: geopolitics reshapes the dominant risk regime. When inflation risk outweighs growth risk — as in a supply-shock, conflict-driven environment — the standard playbook breaks down. Bonds lose some of their hedging power, commodities and defence-related exposures tend to outperform, and conventional portfolio construction assumptions no longer hold.

Geopolitical developments will continue to cause shocks and pose large risks

For example, sanctions can cause losses that are hard to recuperate as has been the case for investors exposed to Venezuela or Russia.

Intensifying geopolitical risks raise the odds of downside scenarios materialising, increasing the need for hedging and for building resilient portfolios.

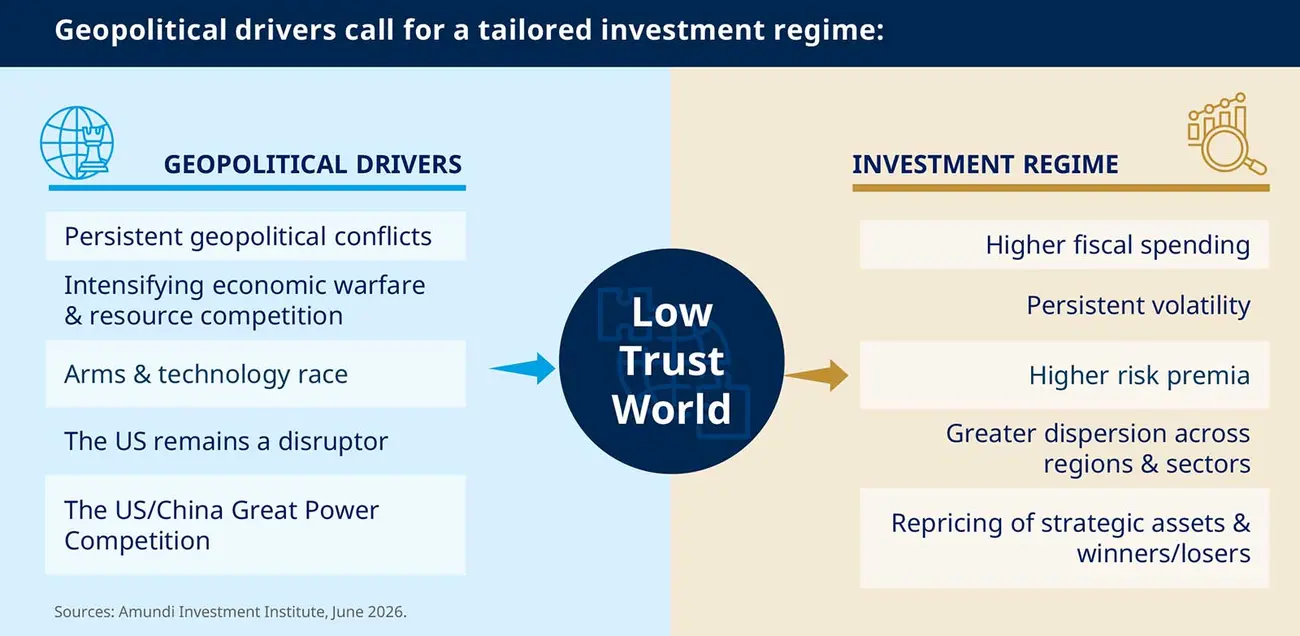

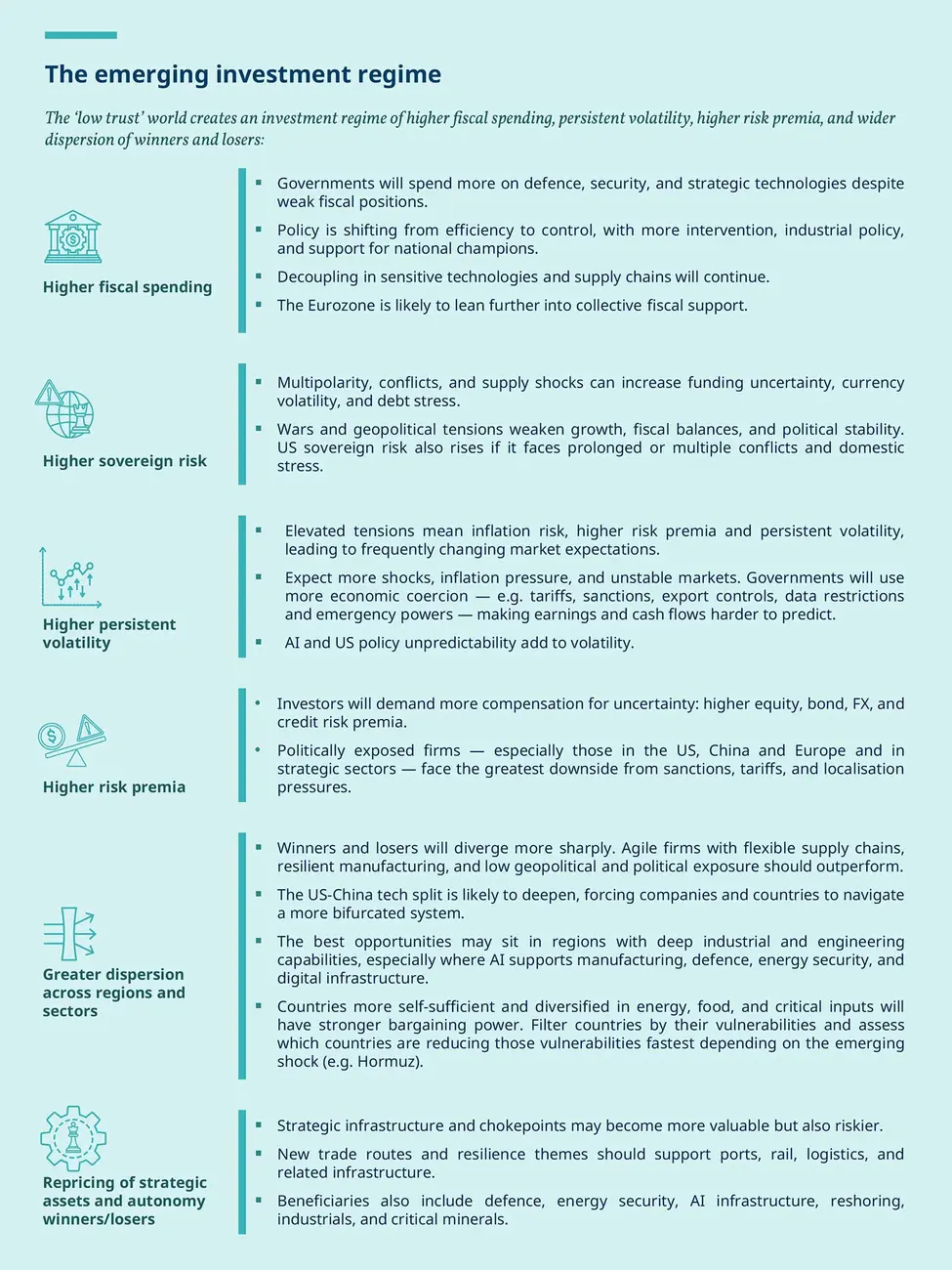

The ‘Low Trust’ World is defining a geopolitically driven investment regime

Elevated tensions may drive persistent volatility, inflation risk, and higher risk premia.

Fiscal spending will remain high as governments invest to increase power and leverage - despite weak fiscal positions.

Returns are becoming more dispersed, with some countries and companies growing much faster than others and some sectors outperforming. This means more divergence in earnings and valuations, and a repricing of strategic assets.

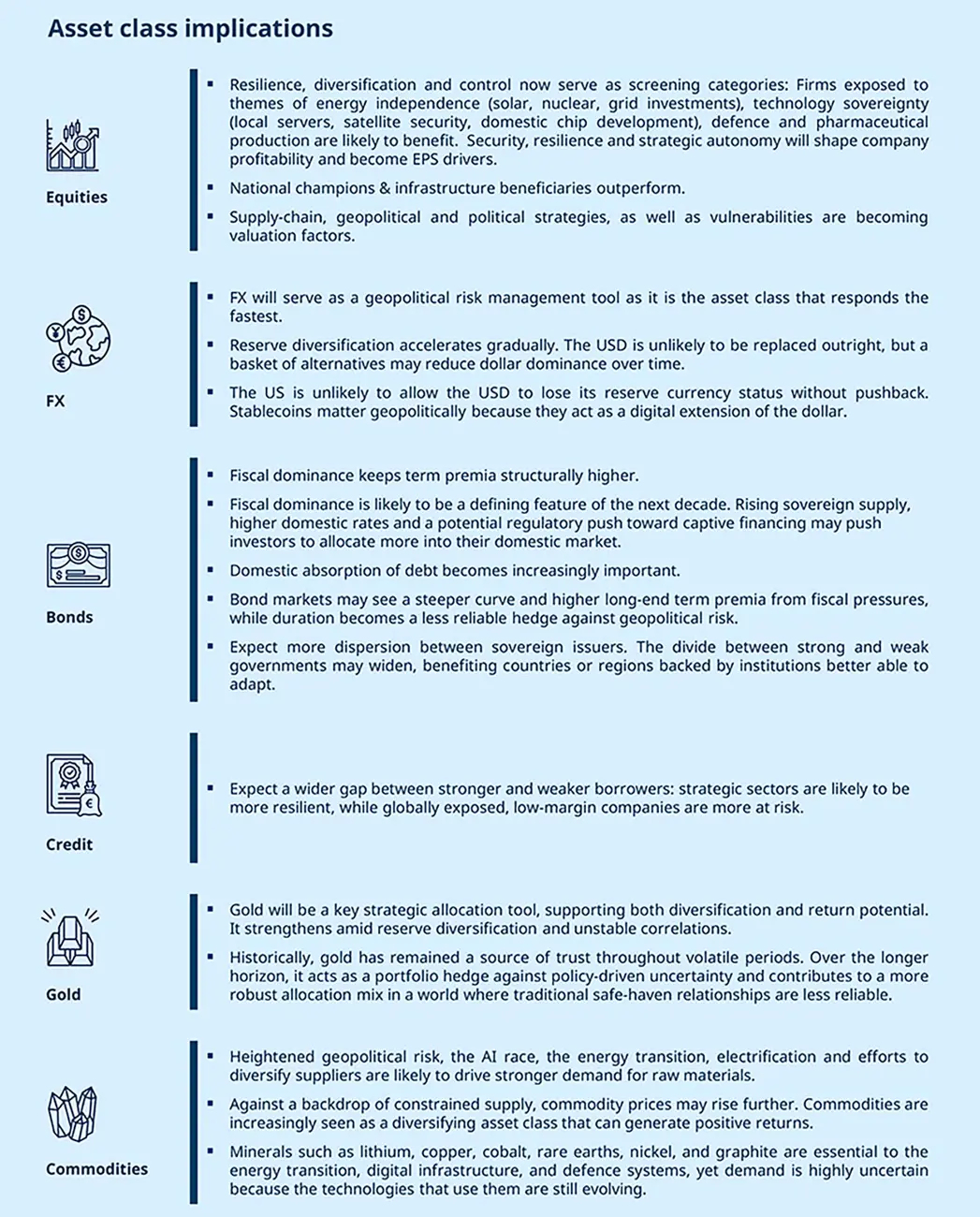

Resilience, diversification, and control are becoming principles of portfolio construction and screening categories. Sectors or companies affected by these dynamics will benefit, including those linked to energy independence (solar, nuclear, grid investments), technology supply chains (local servers, satellite security, domestic chip development, cloud and data sovereignty), defence, food and pharmaceutical production — to name but a few.

Introduction: Welcome to the ‘Low Trust’ World

Over the past few decades, investors operated in an environment of relative stability where the big power plays between countries could often be ignored. Political risk, wars or tumultuous elections mainly affected emerging markets or were treated as temporary shocks to a system geared towards efficiency.

That world is fading. If we were to pick one overarching theme that is shaping the emerging global order, it is the erosion of trust. Realising their vulnerabilities, countries are seeking to reduce external dependencies, while increasing their leverage over others. What counts is not just military or economic power, but also the ability to withstand pain. Efficiency is no longer the dominant economic logic; resilience is.

The nascent ‘low trust’ world is shaped by persistent conflict, economic rivalry, an intensifying arms and technology race and efforts to diversify and rewire supply chains as security and control become central to policymakers around the world.

The dynamics unleashed threaten many things we have taken for granted such as freedom of navigation, trade, borders, energy and connectivity: It only takes a hostile fishing boat dragging an anchor to cut critical underwater communication cables or to lay mines to close a vital waterway.

In this environment, geopolitics is no longer simply a source of episodic volatility. The shift from efficiency to resilience, from global integration to strategic control, and from peace dividend to security premium has consequences for investors.

In a world that remains deeply interconnected, the preparation to navigate potential ruptures is what will shape future investment trends. The winners will be those that are agile and strategic enough to adapt to the new geopolitical realities.

At the same time, geopolitical developments now shape the macro backdrop and capital allocation. Therefore, the ‘low trust’ world requires investors to embed geopolitical analysis throughout the investment process.

Anna ROSENBERG

Volatility is no longer an exception in financial markets; it is the rule. Geopolitical developments now persistently affect the inputs that flow into the investment process.

The evolution of geopolitics & its investment implications

It has been our longstanding view that the level of geopolitical risk would rise for the remainder of this decade. Recent developments have proven this correct. We based our assessment on the evolution of drivers playing out over the past several years — drivers that will continue to unfold. In the following section we outline their likely trajectories and spell out their investment implications.

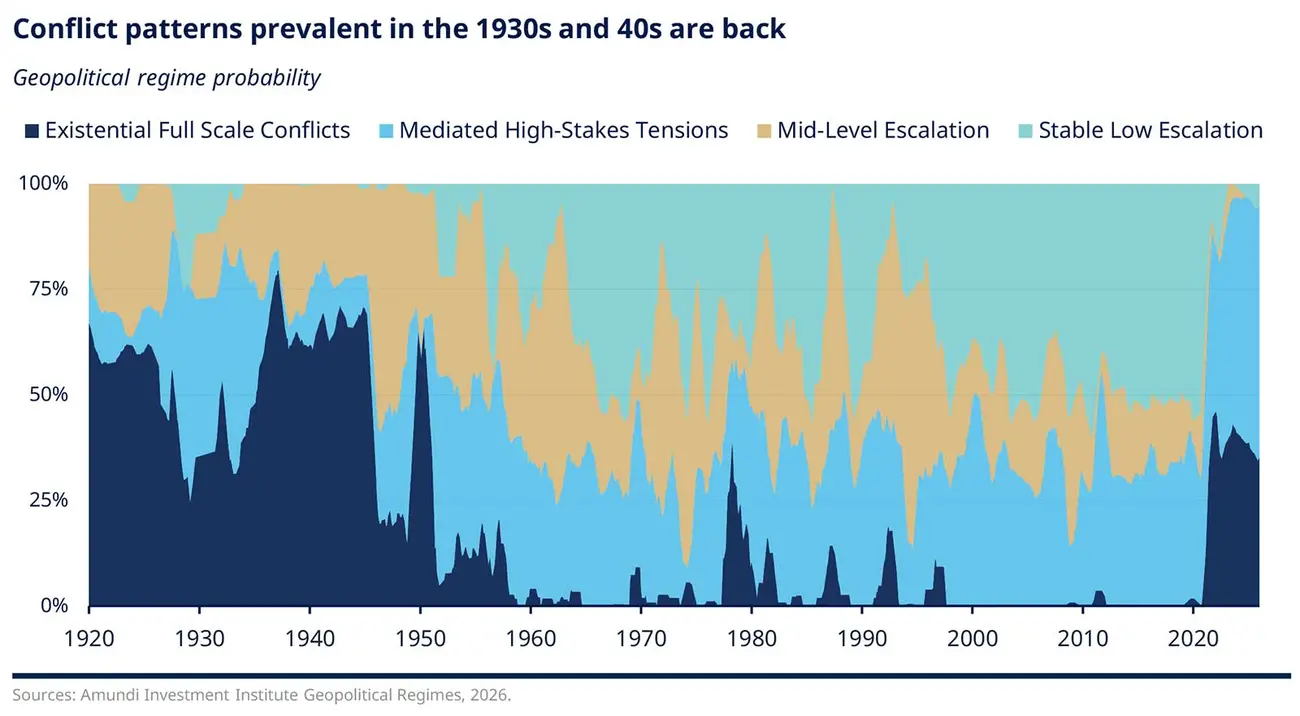

Data shows we are moving back toward a persistently high risk of conflict and volatility

Geopolitical risk is at its highest level since the end of World War II, based on our own internal assessment of the intensity of conflicts and the ability to solve them diplomatically. Our analysis of geopolitical regimes since the onset of the 20th century illustrates the paradigm shift: The relative stability that characterised the post-Second World War era ended at the onset of this decade. We are witnessing the highest number of active conflicts since the end of WW2, while diplomacy is struggling to solve the underlying issues. History teaches us that similar periods saw the emergence of various conflicts and tensions playing out simultaneously. As some actors take advantage of the volatile environment, and as climate change opens new maritime routes and land, expect persistent conflicts, challenges over territory, waterways, ports and maritime chokepoints.

More countries are likely to adopt coercive economic measures, causing more friction

In a ‘low trust’ world, leverage matters and more countries are likely to use theirs to defend interests. More countries will apply broader coercive economic measures: Washington expanded the economic toolkit in 2026 beyond sanctions, export controls and tariffs to include a naval blockade and a strategy of resource denial by targeting Venezuela's oil, thereby removing a major energy supplier to China. China strategically built out a system that has made many countries dependent on its many critical exports and has now implemented an export control mechanism for these that it can apply when it suits its foreign policy goals. The EU created the ‘Anti-Coercion-Instrument’ which allows the bloc to cut off market access.

Natural resources, from energy to critical minerals, will be front and centre of competition and coercion. Various countries are tightening control over critical minerals. For example, Mexico is nationalizing lithium and cancelling licenses, Chile and Bolivia are imposing controls, Indonesia is restricting nickel and bauxite exports, Canada and Australia are implementing tighter foreign direct investment (FDI) regimes. In the Horn of Africa and Gulf of Aden, Middle Eastern powers are vying for access to hydrocarbons, ports, minerals, and arable land. Meanwhile, the US, Russia and China are competing to secure resources in the Arctic.

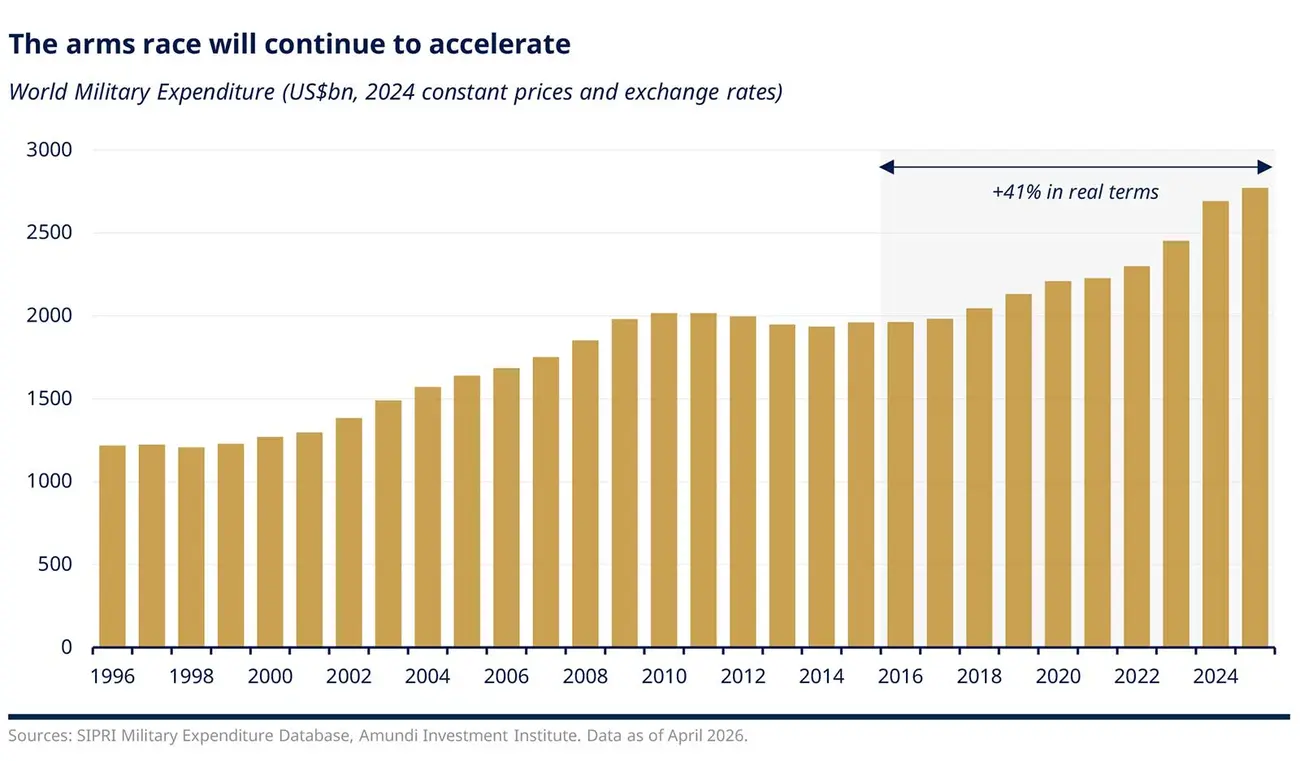

Expect defence spending to remain high, despite strained public finances

The lessons learned from the wars in Ukraine and the Middle East are pushing governments to invest in defence so that they can deter and manage the full spectrum of threats. These encompass ‘traditional’ warfare to cyberwars, grey-zone operations and threats to critical infrastructure (e.g. undersea communication cables, the energy grid) to AI and drones, satellites and space technology. Security spending will move beyond traditional defence spending to cover these sectors too. While a drone may cost a few thousand dollars, the interceptor bringing it down can cost millions. All the while, politicians must keep restive domestic populations happy. Bond markets could come under pressure from bigger deficits and higher borrowing needs. That could keep borrowing costs elevated and make bonds less reliable hedges in periods of stress.

The AI race will continue unrestrained, fuelled by geopolitical rivalries, while regulation and control will be driven by geopolitical concerns

Throughout history, technological innovations increased global interconnectedness by reducing travel time and enabling commerce. However, technological innovations also intensified intra-state rivalries. As AI is taking shape at a time when the rules-based international system is collapsing, AI is likely to intensify current rivalries.

Fear of a ‘winner takes it all’ dynamic is encouraging the US and China to search for ever more powerful models, despite concerns about its impact on societies and its use in warfare. As the US becomes less dependable and scepticism towards China remains high, countries will look for ways to increase their leverage, for example by supporting national companies that provide critical inputs for the AI supply chain. Increasingly, geopolitics will shape AI regulation too. The US government recently moved to limit access to Anthropic’s latest AI models to non-US users, while Dutch authorities halted the takeover of a local firm by a US company over concerns related to data sovereignty.

AI also poses a risk to domestic political stability, with knock-on effects for geopolitics.

Should AI lead to large-scale job losses, social cohesion could be undermined. A large wealth gap benefits political parties that call for wealth redistribution. Governments may try to introduce universal income, yet how to fund it could cause tensions given global taxation of large tech firms has been unsuccessful even in a rules-led international order.

The US will likely remain a disruptor, accelerating diversification and the transition to multipolarity while inadvertently strengthening China

Keen to cement his legacy, the US president will likely continue to pursue an interventionist foreign policy for the remainder of his term. Many of the actions the US president has undertaken have been aimed at halting the decline of the US as a global hegemon. Instead, however, the US has caused allies to increasingly question US leadership and their ties to the US. This dynamic has become apparent in the recent Iran/US war, where at time of writing, Iran is emerging stronger, while Israel — a key US ally — now faces more security risks. As a result, allies will increasingly hedge their bets.

However, there are limits to how much the US administration will turn away from its partners. While US presidents come and go, US core interests have prevailed thus far. Despite voicing threats, the US is likely to remain in NATO — the alliance makes the US stronger. Equally, the US remains engaged in European security. Having military bases in the continent gives it global reach, while reducing the potential threat emerging from a newly re-armed Europe. Keeping global waterways open is another core interest the US will try to protect.

The US will likely seek to expand its influence over the Western Hemisphere. In Latin America, the US aims to weaken Chinese influence and support US-friendly regimes; Cuba is likely a target. US aspirations over Greenland will prevail, but the US will likely seek to win over the island politically rather than militarily because of the risk the latter poses to NATO. And the US will remain embroiled in the Middle East as tensions and risks are likely to persist.

The biggest tensions remain in the South and East China Sea as US core interests compete with China’s. In the short term, the US/China relationship remains in a state of ‘tense understanding’ as both sides realise their mutual dependency. The US relies on China’s rare earths, while China relies on free trade for economic growth and political stability. But this remains a Great Power Competition and the US failure to achieve its military objectives in Iran is likely to embolden China. Tensions are likely to rise alongside intensifying economic competition and the military build-up in the South and East China Sea.

Recent developments have accelerated the transition towards a multipolar system that is considered less stable than a hegemonic system. However, multipolarity also enables diversification as countries enter new alliances and diversify supply chains. This trend will accelerate as the new trade and security deals signed in 2025 begin to have a real-world impact (e.g. the EU/India, EU/Mercosur trade deals).

Ongoing risks in critical trade routes, such as the Strait of Hormuz, will accelerate diversification, while more countries strive to find new suppliers of critical inputs, from rare earths to energy to food. For example, India is deepening its partnership with Brazil for critical minerals and is shifting its energy strategy to suppliers like Saudi Arabia while still buying Russian oil.

The efforts to diversify will also continue to affect the USD. While one sole alternative to the dollar remains elusive, a combination of alternatives is likely to emerge as countries seek to reduce usage of the USD and associated payment systems.

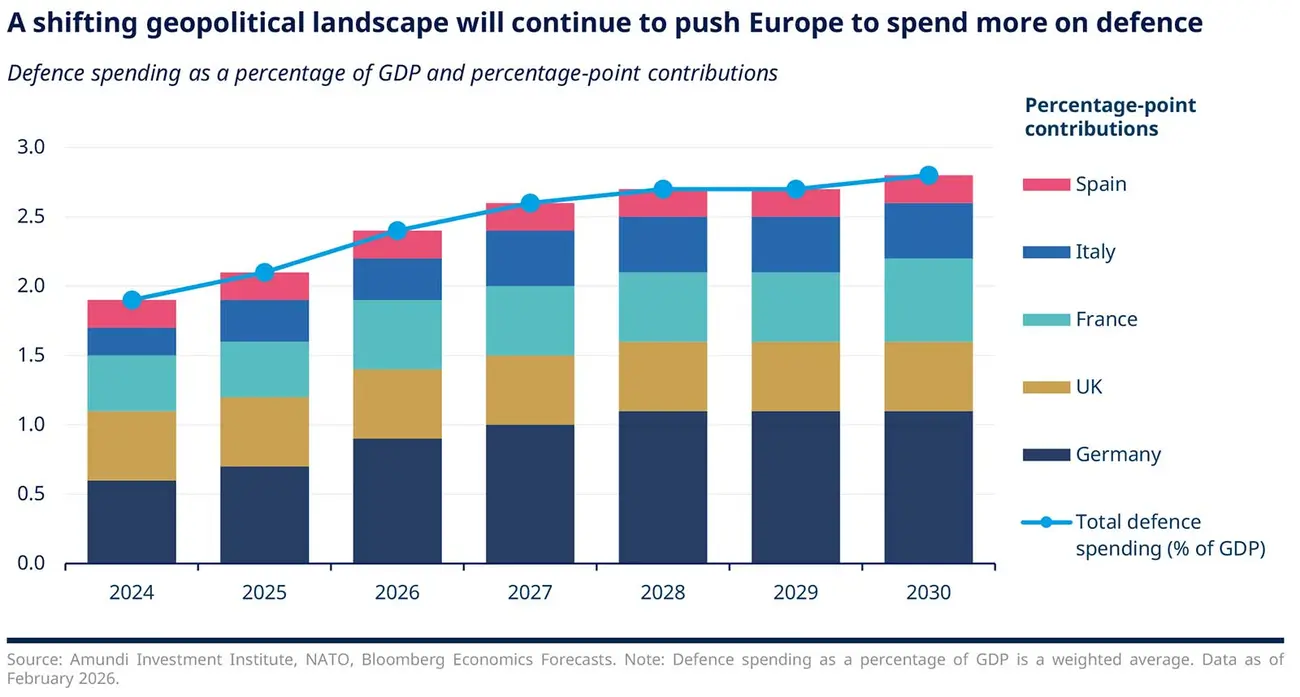

Europe will emerge as a stronger geopolitical player, with trust in its institutions a key advantage

The drivers outlined above have various implications, but most notably the EU — together with the UK and Ukraine — will likely re-emerge as a geopolitical heavyweight. In today’s context, and despite sporadic intra-European tensions, European leaders are more likely to continue to integrate and the military transformation underway is changing the status quo. Germany is re-emerging as a military power. Keen to avoid a repetition of the past, Berlin is channelling defence spending into joint European and NATO projects such as positioning a Bundeswehr brigade in Lithuania. Ukraine, with European investment, has become Europe’s innovation hub for cutting-edge military technology. The Nordics, the Baltics, and Poland are collaborating on defence.

All the while, the threats are likely to remain acute: Russia’s philosophy of war is driven by opportunism, and a ‘low trust’ world is likely to create more opportunity. The Russia/Ukraine war shows few signs of stopping, although the EU and UK strategy of maintaining unity and supporting Ukraine, while slowly eroding Russia’s capabilities to make it more willing to compromise in negotiations, is beginning to bear fruit. But until Europe is militarily strong enough to deter Russia, it will remain vulnerable. That realisation is ensuring that defence spending remains a priority.

Relations with China and the US will remain tense, even as Europe’s security infrastructure remains embedded in NATO. To stand a chance in a world of intensifying power plays, Europe has little choice but to pursue economic cooperation and protectionism and to use its economic might as leverage. While trust is a scarce global resource today, the continent’s institutions still have it — and this will likely be rewarded by investors.

Conclusion: In a ‘Low Trust’ World, resilience is the new efficiency

As we have outlined in this paper, we are amid a regime shift towards a ‘low trust’ world. Governments, policymakers, countries, companies and investors are reassessing vulnerabilities built during decades characterised by efficiency and relative geopolitical stability.

In this environment:

Resilience is like to outperform efficiency

Diversification will likely matter more than optimisation

control and security thmes will reshape capital allocation

Geopolitics will increasingly define winners and losers

The ‘low trust’ world is not a temporary shock. It’s a rupture that calls for a tailored approach which recognises that geopolitics shapes the macro backdrop, leader’s decision-making, emerging investment trends and the assumptions informing the investment process. For investors this means moving beyond traditional frameworks and incorporating geopolitical analysis into the macroeconomic and investment processes, strategic asset allocation, risk management and portfolio construction.

Monica DEFEND

In a ‘low trust’ world, investors must diversify differently: not just by asset class but by geography, FX, supply chain exposure, policy regime, and geopolitical vulnerabilities and opportunities.

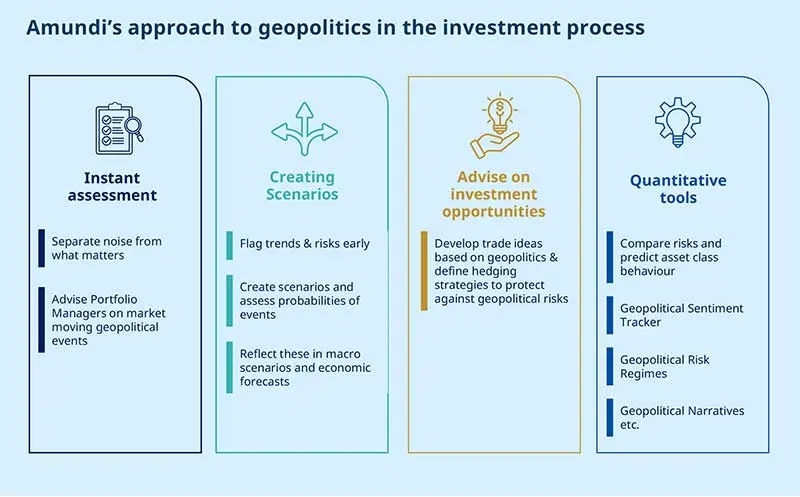

Our approach: turning geopolitical insight into investment action

As geopolitical factors have become more dominant for financial markets, Amundi created an integrated structure and tools to aid our investment process:

Our geopolitical scenario analysis is integrated in our portfolio allocation decision making by ensuring that the views are well articulated and presented to our investment committees.

Equally, our geopolitical expectations are reflected in our macro forecast that feeds back into the investment process.

Further, we have created quantitative tools, such as the Investment Phazer and the Geopolitical Sentiment Tracker, that add quantitative components to our analysis.

Authors