Summary

Diversification* is paramount as investors start to move away from overcrowded areas, taking profits and making room for new IPOs.

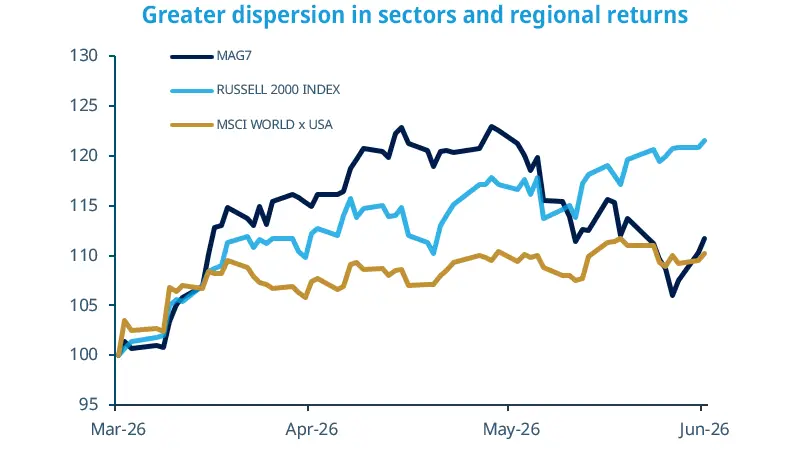

A record quarter for equities

Global equities closed their best quarter since late 2020. Emerging markets remain the strongest- performing area, posting their best quarter since 2009.

Technology and AI-related themes remained the main drivers, but momentum faded in June as investors rotated within the AI-trade and across sectors and geographies.

Looking ahead, we expect greater investor scrutiny and a broader push towards diversification. Selectivity and fundamentals should remain key.

Source: Amundi Investment Institute, Bloomberg, as at 30 June 2026. Indices rebased to 100

Global equities extended their gains last quarter, shrugging off geopolitical risks, shifting expectations for central bank policy and volatile sentiment around the AI trade. The broadening away from crowded trades is a key market theme set to continue. In the US, performance widened as investors rotated out of the so called Magnificent 7 into industrials and defensives, while small caps (Russell 2000 Index) outperformed on the back of resilient growth, employment and consumer spending, which support domestic corporate profits. The same pattern has emerged across regions. European equities outperformed into quarter-end as investors sought to reduce concentration risks and broaden exposure to themes that should benefit from a more investment-led model of growth and a German fiscal push. Other laggard areas, such as emerging markets beyond Asia tech, could benefit from this rotation, offering opportunities also across the entire AI value chain; Latin America is particularly well placed thanks to demand for AI-related raw materials.

This week at a glance

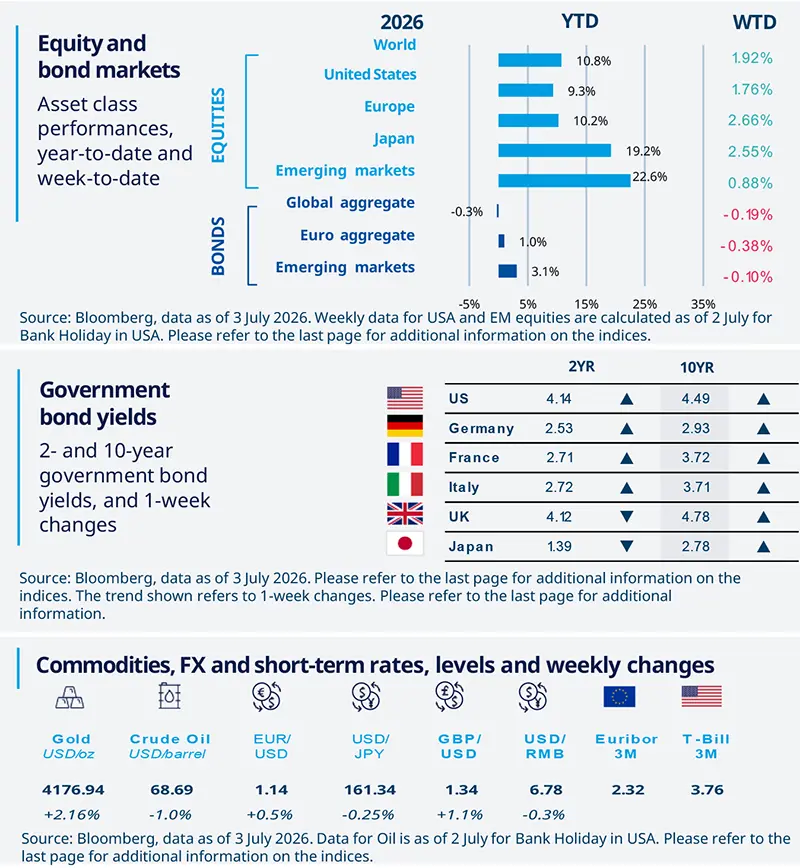

Equities rebounded in the second half of the week after tech losses driven by concerns over valuations and capex. On a weekly basis, Europe led, while emerging markets posted smaller gains. Treasury yields moved in a tight range amid hawkish comments from central bankers and weak labour market data. The dollar weakened and gold rose as investors trimmed bets on Fed interest-rate hikes. Oil fell as tanker traffic through the Strait of Hormuz continued to increase.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 3 July 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US job gains soften in June

Nonfarm payrolls rose by 57,000 in June and revisions subtracted a combined 74,000 from the prior two months. June’s jobs report sent mixed signals boverallut, , pointed to a stable labour market. Payroll growth was a little softer than expected and prior months were revised lower, but the underlying trend remained firm and stayed above most estimates of the breakeven pace. The decline in the unemployment rate to 4.2% from 4,3% was partly driven by lower participation. The June jobs report should keep the Fed on hold.

Europe

Eurozone inflation eases in June

Eurozone inflation eased more than consensus expected as the fragile de-escalation in the Middle East pushed global oil prices lower. Consumer prices rose by 2.8% year on year in June, down from 3.2% in the previous month. Core inflation, which excludes volatile items such as food and energy, also fell more than expected, from 2.6% to 2.4%, while the services component declined to 3.2% from 3.5%. The report reinforced the view that the ECB is likely to raise rates once more this year, but not embark on a full hiking cycle.

Asia

Japan’s Tankan surprises to the upside

The Tankan survey surprised to the upside, showing that business sentiment improved in Q2 despite the ongoing Middle East conflict (the survey cut-off date was 11 June, before the Iran-US deal). The manufacturing index beat expectations, capex plans were revised sharply higher, and inflation expectations continued to rise. Financial conditions remain accommodative, suggesting that BoJ rate hikes so far have had only a limited tightening effect. Taken together, the Q2 Tankan reinforces the case for further BoJ normalisation, with October looking like a likely window for the next rate hike.

Key Dates

EZ Sentix Investor Confidence, PPI and Retail sales; US ISM Services |

US FOMC Meeting Minutes |

China PPI and CPI, Mexico CPI |

Authors