Summary

Although the ECB raised rates amid concerns that inflation will remain above target in the near term, we do not expect it to embark on a full tightening cycle. Nonetheless, the ECB would remain highly attentive to energy prices, and pressures on domestic demand.

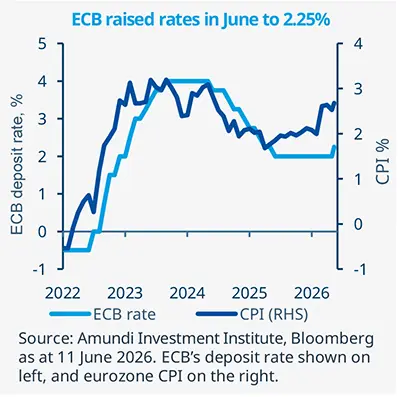

ECB raises rates after almost three years

The ECB raised rates in June in an attempt to curb inflation, in line with our expectations.

The data currently available are insufficient to assess the magnitude or persistence of the shock stemming from the Middle East conflict.

The central bank did not provide clear forward rate guidance and will remain data-dependent before taking any further action.

The ECB’s 25 basis point hike in June confirmed that the Bank is no longer willing to look through the spike in commodity prices. It considers the inflationary pressures generated by the war in the Middle East to require this adjustment in monetary policy. The ECB gave no forward guidance for rates due to the uncertainty associated with the Middle East crisis. We expect the bank will continue to monitor the duration of the Middle East conflict and its effect on other parts of the economy. Additionally, the bank should remain vigilant about wage growth dynamics, inflation expectations, and the pass-through of inflation from input prices to output prices before taking further action. Our view of one more hike this year is reinforced by the Bank’s recent upgrade to its inflation forecasts for the current year. On the other hand, economic activity is likely to remain fragile in the near term, although we do not expect a recession, at a time of heightened uncertainty over the energy shock. Thus, we think the ECB is unlikely to completely ignore pressures on domestic consumption in the eurozone.

This week at a glance

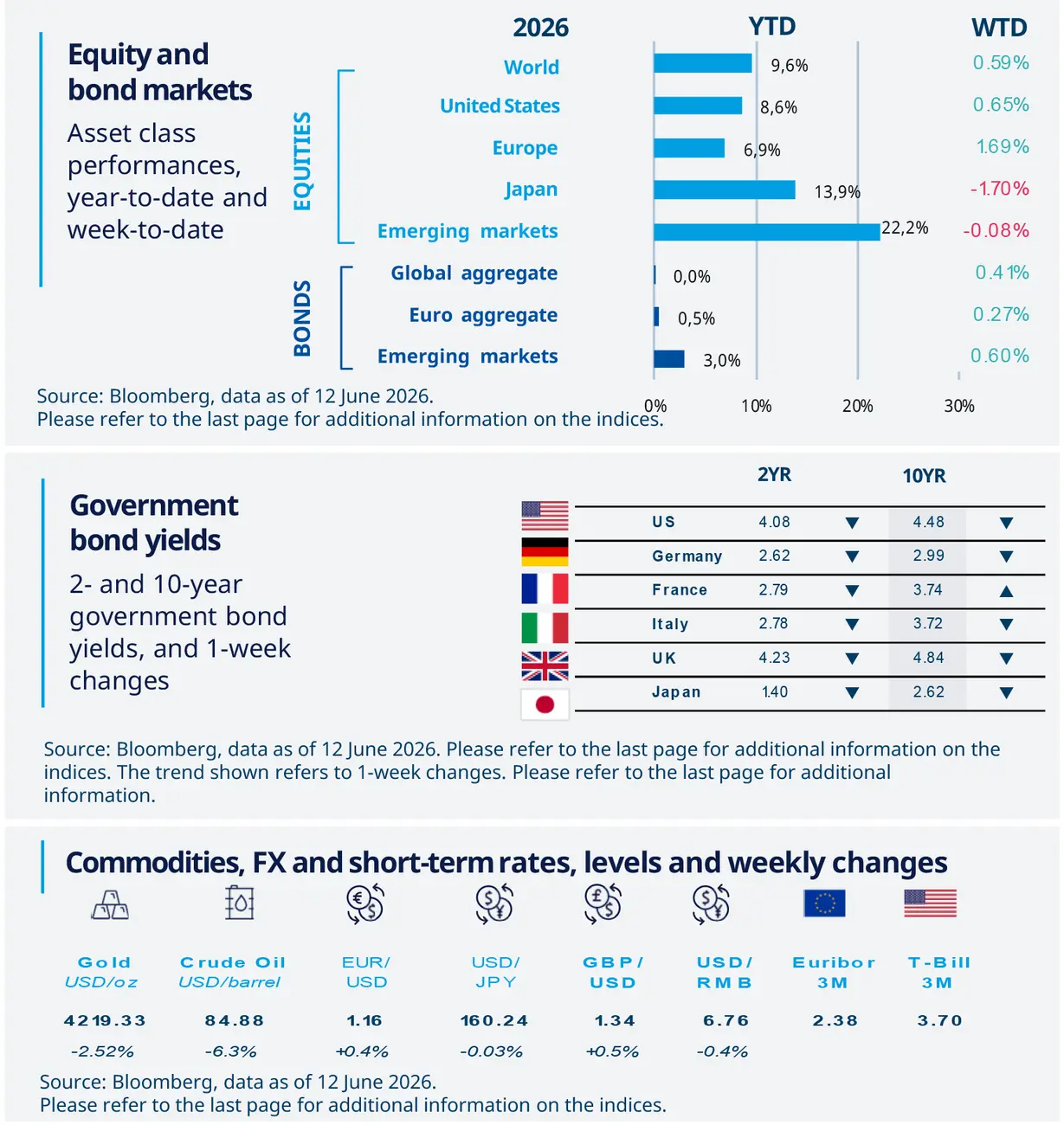

Equity markets were mixed. US and European indices rose amid optimism over a deal between the US and Iran, as well as a rally in stocks linked with the space exploration industry. In contrast, Japanese markets and EM stocks declined. Most bond yields fell, while oil extended its decline on hopes over a US-Iran deal. Gold remained under pressure as US real yield stayed high.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 12 June 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US inflation rises on energy shock

Inflation jumped to 4.2% in May, its highest reading in three years. The increase was largely driven by energy prices, linked to disruptions to oil and gas supply through the Strait of Hormuz. The core index (excluding volatile components) rose 2.9% YoY, close to April’s 2.8%. The PPI printed at 1.1% (mom) for May, with more than half of the monthly advance in producer prices attributable to higher gasoline prices. Overall, the data suggest a supply-driven inflation shock, rather than a broad demand-led acceleration.

Europe

Euro Area growth slightly fragile

The EZ’s Q1 growth was revised down to -0.2% QoQ in the final release but, excluding the data for Ireland the data were decent. Overall, the report showed that domestic demand was already slowing before the conflict. Additionally, the consumer recovery is coming under further pressure from a renewed hit to purchasing power by accelerating inflation. A high savings rate may help cushion the shock, but real wage growth is expected to slow and turn negative in some countries, creating additional strain for consumers.

Asia

South Korea posts exceptional export growth

In the first 10 days of June, exports from Korea, the region’s bellwether exporter, rose 85.9% YoY, suggesting that the semiconductor cycle has continued to strengthen and shows no signs of slowing yet. This surge in exports has boosted corporate profits and, in turn, tax revenues, enabling the government to offset the Iran shock almost entirely through redistributive fiscal measures.

Key Dates

China industrial |

FOMC policy decision, |

Japan CPI, UK retail sales, |

Authors