The global economy is being splintered by worsening relations between America and China. Relying on the typical cyclical playbook may be unwise.

Introduction and aims

As pension investors transition to a new regime, one question has come to the fore: where will the returns come from?

The Great Moderation of the past 25 years was marked by stable economic growth, low interest rates and low inflation. They favoured ‘set-and-forget’ asset allocation. That was shattered by four recent cascading game changers: the severe monetary tightening by key central banks to tackle the inflation spike; worsening conflicts in the Middle East and Ukraine; the rise of populism in the West due to the cost-of-living crisis; and the US–China geopolitical rivalry fragmenting the intricate web of global supply chains. That integration is now seen as a source of risk and insecurity.

On the upside, however, this is also creating opportunities as capital markets adjust to the new regime. With public equity markets in the West flirting with their all-time highs, the search for good risk-adjusted returns is turning the spotlight on two sets of thus far underinvested asset classes.

The first set covers illiquid assets in private markets, benefiting from the recent surge of investment in strategic sectors like AI, defence, renewable energy and infrastructure. Private markets are increasingly seen as providing exposure to innovation while IPO activity remains sluggish, especially in Europe. As such, they are viewed as a most likely source of value creation for the foreseeable future.

The other set covers Asian emerging market assets in the world’s fastest growing region. It accounts for 46% of global GDP, 60% of the world’s population and 60% of expected global growth through 2030, according to the IMF and the World Bank. The centre of gravity of the world economy is shifting towards this region, according to current narratives. Hungry for foreign capital to facilitate energy transition, they are also implementing investor-friendly reforms.

|

|

Hence, the 2024 Amundi–CREATE global pension survey has a twin focus on asset classes in private markets and Asian emerging markets. On a three-year forward view, it covers five questions:

- what are pension plans’ current allocations to these asset classes and how are they likely to change?

- which factors have constrained allocations so far and which ones will likely drive them in future?

- what specific investment benefits are being targeted and to what extent have expectations been met?

- how is the mix of components within each of the broad asset classes likely to change?

- which selection criteria will be used when awarding new mandates to external asset managers?

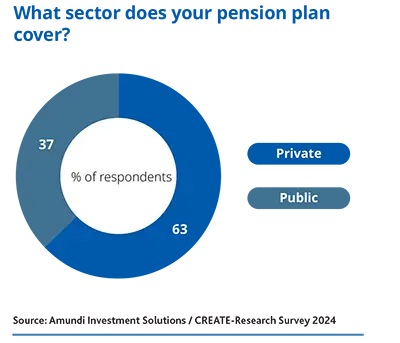

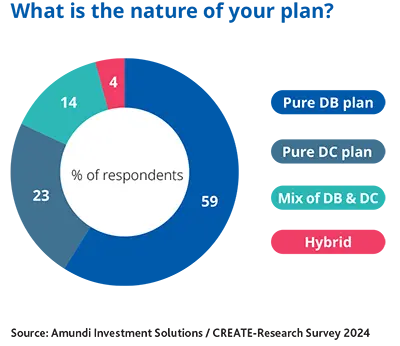

The survey involved 157 pension plans in 13 key jurisdictions, collectively managing €1.97tn of assets. The survey results were bolstered by 30 structured interviews with senior decision makers from respondent organisations. The survey provided the breadth, with interviews adding depth and insight.

Authors