Summary

Macro impact: The Iran conflict and risks to the Strait of Hormuz do not yet warrant a major change to our base case macro outlook. Growth adjustments remain limited, inflation has nudged higher, and central banks are broadly in a wait-and-see mode, with policy rates expected to remain largely stable. However, Europe is more vulnerable to this type of shock, as it faces stronger headwinds from potentially higher inflation and weaker growth. This crisis may further hasten the EU on its path towards strategic autonomy and green energy.

Geopolitical angle: The US and Israel are pursuing core ‘must haves’ by degrading Iran’s military, missiles, and nuclear capabilities, while regime change remains a secondary ‘nice to have’. The key signpost to watch is whether people will take to the streets and if militias will try to seize the opportunity to overthrow a weakened regime.

Investment implications: This is a time for balance, not indiscriminate ‘buy the dip’ or risk aversion. Risk allocation should be diversified and selective, avoiding areas most exposed to leverage, inflation shocks, and AI-driven disruption.

The Iran conflict has prompted us to make targeted adjustments to our macro assumptions, rather than fully change our scenarios. Overall, we have marginally upgraded our global inflation outlook, while growth adjustments remain minimal at this stage.

Monica DEFEND

The war in the Middle East raises downside risks to growth and upside risks to inflation, leading central banks to a wait-and-see approach.

Central Bank policy expectations

Easing bias retained but rate cuts* postponed to September and early 2027. The easing bias is confirmed by an exacerbation of economic bifurcation (more stress on low earners compared to high earners) and subdued labour market. The mild inflation spike will be consistent with the Fed continuing to ease policy rates.

**25 bps each. Source: Amundi Investment Institute.

On hold this year. We do not project any rate cut this year in our central scenario (from a cut earlier). However, the ECB should not hike either, trapped in a policy dilemma combining weak growth and high inflation.

Cuts postponed. We have postponed our rate cut expectations to June and September as the BoE is likely to ignore the mild upward pressure on inflation.

No change. Tightening to continue with a higher sensitivity towards the yen. In the base case, we continue to see the BoJ hiking once by 25bps over the summer. A larger weakening in the yen could trigger a larger hike.

No change to our policy assessment of two cuts starting in May**.

**total 20 bps. Source: Amundi Investment Institute.

No change, we expect the RBI to stay on hold this year.

Beyond the immediate impact, we are also assessing the potential implications should the oil shock prove more prolonged.

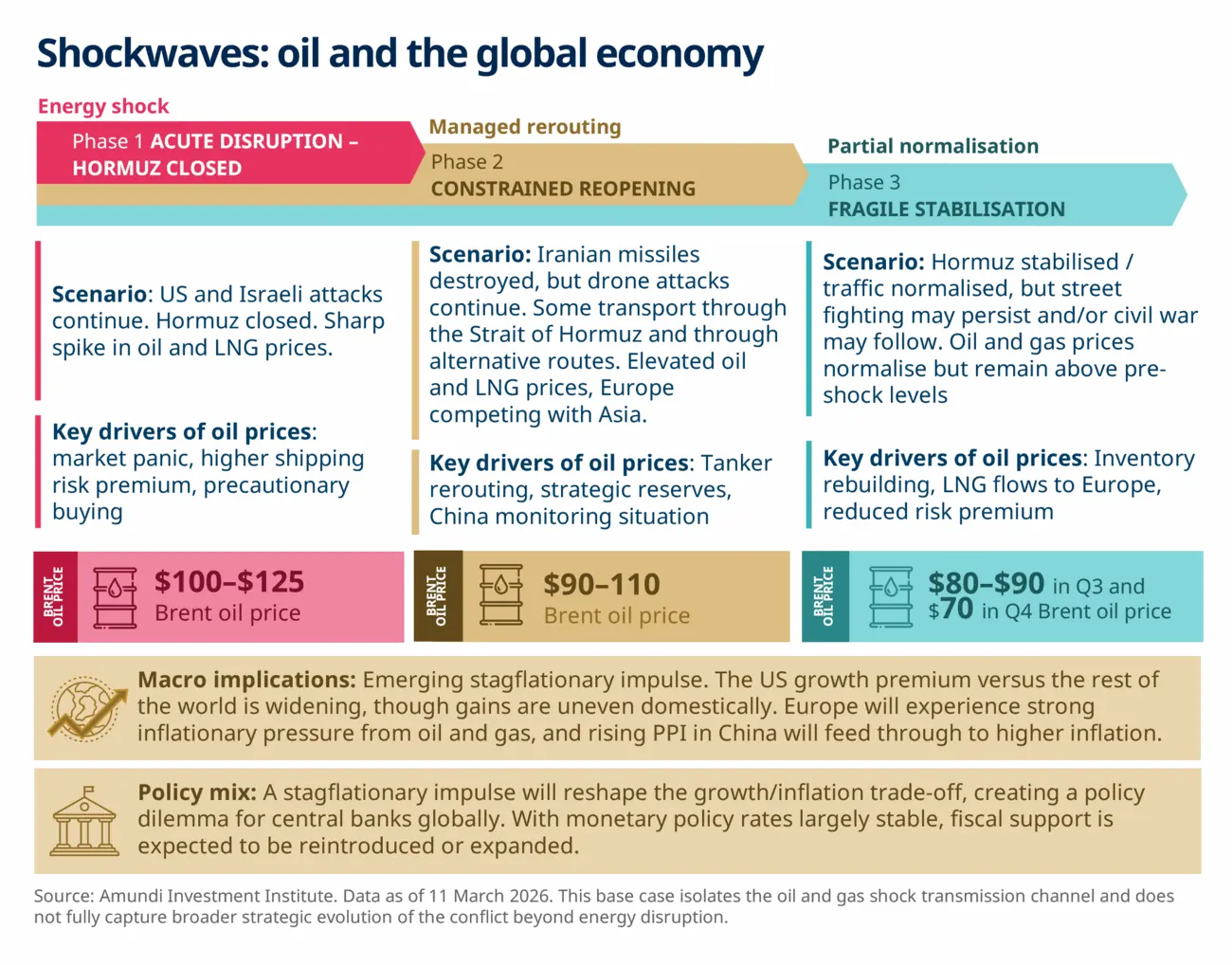

The oil ‘what if’: Amundi oil shock scenario

Oil prices are the central transmission mechanism for the Iran war to seep into the real economy. Hence, the persistence of oil and gas prices at high levels (not the actual level, per se) and the duration for which the Strait of Hormuz remains impassable are two main factors that will determine the economic impact. We outline below the three phases (1. energy shock; 2. managed rerouting; 3. partial normalisation) through which we think the situation in the Strait of Hormuz could evolve in an oil shock scenario.

Phase 1 Energy Shock: The phase of acute disruption in which the Strait remains impassable, traffic is near zero because the US and Israel continue to bomb Iran and the latter retaliates. Brent prices stay between $100-$125/b and LNG prices also surge as shipping risks and insurance premiums rise. Across markets, that translates into risk-off or panic, and precautionary buying of energy.

Phase 2 Managed Rerouting: Constrained reopening of the Strait, some traffic is also rerouted through alternative routes. Iranian missiles are destroyed but drones continue their attacks. Brent prices come down within the range of $90-$110/b but stay elevated (from pre-war levels) as Europe and Asia compete for energy demand. Strategic oil reserves at the country level become crucial to navigate this phase for countries very dependent on the Hormuz supply.

Phase 2 may also include a more extreme scenario that extends beyond a short-lived energy shock and evolves into a more persistent phase of regional disruption.

The Strait of Hormuz will not be fully closed, but traffic and logistics are impaired for a prolonged period through rerouting, higher insurance and freight costs, periodic security incidents, and lingering geopolitical risk premia. Oil and LNG prices stay elevated relative to pre-shock levels, even as most of the stress gradually fades.

In this case, the macro impact is that of a stagflationary impulse, which is strongest in energy importing regions, with inflation staying higher for longer and growth weakening unevenly across economies. Central banks are forced to respond in a more cautious and fragmented manner. While the Fed will look through the inflation spike, the ECB would face a sharper inflation-growth dilemma. Some EM central banks may delay or reduce easing in this case. In this scenario, we have isolated the oil and gas shock transmission channel (to the economy) and do not fully capture broader strategic evolution of the conflict beyond energy disruption.

Phase 3 Partial Normalisation: A fragile stabilisation and normalisation of traffic through the Strait happens three months from now, but protestors and dissenting militias may have taken to the streets in Iran trying to overthrow the regime; a civil war is a possibility too. As long as shipping traffic passes normally through the Strait, this fighting on the streets doesn’t affect Brent (and gas) prices, which stabilise between $80 and $90/b before moving later to $70 (closer to a Global Demand-Supply Fair Value). This would result from rebuilding energy inventories, normalising LNG flows to Europe, and a reduction in risk premiums.

Regional implications of the oil shock

The stagflationary impulse from sustained higher oil prices will have an uneven impact across countries. The US economy is expected to remain more resilient, resulting in a widening growth premium over the rest of the world. However, the impact within the US will vary, with notable differences across sectors and income groups. Europe faces pronounced inflationary pressure from oil and gas, while rising producer prices in China are set to add to global inflation.

Europe is more vulnerable to the type of shocks that we are pencilling in, compared to the US. The region has been aiming for energy autonomy (as part of its strategic autonomy), diversifying its supplier base and its energy needs. This crisis may well turn into an accelerator of higher autonomy and greener energy. In the near term, however, Europe faces stronger headwinds, with higher inflation and weaker growth. This will further reinforce the case for the ECB to remain on hold.

In contrast, in the US we expect a more limited impact on inflation (more flexible and competitive energy market) and growth. However, the oil shock is expected to amplify already existing inequalities: energy-intensive consumption is more relevant for low-income earners. Heading towards the midterm elections in November with mild domestic support for the military action in the Middle East, there will likely be a high incentive to end the strikes and/or to reinforce household support by containing inflation. With a mild impact on growth and relatively stronger impact on inflation, we believe that Fed cuts should be off the table.

In Asia, we see negative impacts on China, Japan, and India. Beyond the available oil reserves, we can’t neglect the relevance of Hormuz for China; however, the policy mix as a percentage of energy consumption has been changing over the years, with electrification increasing and coal declining substantially: the mix can rebalance during a crisis.

How could the war evolve?

Since the onset of the war, the US and Israel have had two distinct desired outcomes: the ‘must haves’ and the ‘nice to haves’. The ‘must haves’ include weakening Iran’s missile and nuclear capabilities, as well as its military and regime apparatus. Regime change, however, remains a ‘nice to have’ for both the US and Israel, although for Israel, regime change has a higher priority than for the US.

By causing severe economic pain, Iran’s military strategy aims at getting the US and Israel to settle for the ‘must haves’ and avoid pursuing regime change. Based on available data, we expect the ‘hot phase of the war’ — the time it takes for the US/Israel to achieve the majority of their ‘must haves’ — to last another 1-2 weeks. That said, the issue of removing Iran’s highly enriched uranium is trickier.

At present, we see three scenarios emerging: a full ceasefire, fighting moving to the streets for a more prolonged conflict, or a full war at the present level of intensity that lasts longer. While the US is now seemingly looking for an off-ramp, it will be difficult for the US alone to end this war as the US president does not control all the forces that have been unleashed. As we have seen in Ukraine, despite Trump’s efforts, it is not easy to end wars.

The key signpost to watch is whether people will take to the streets and militias will try and seize the opportunity to overthrow a weakened regime. This is likely, in our assessment. The Iranian diaspora will likely call upon Iranians to resume protests at home, while separatist Kurdish militias will try their luck, and these efforts will likely be supported by Israel. The key question is when does this happen — immediately after the hot phase, or at a later phase.

If Israel does not succeed with regime change, it would likely prefer Iran to be destabilised, inward-looking and busy with itself. The regime will therefore continue to fight for survival, and we expect sporadic drone attacks in the region to persist.

If the regime survives, the only conclusion it can draw from the current conflict is that it needs a nuclear weapon to protect itself. This means that the diplomatic path to solve the nuclear threat is now even more difficult, making a military solution more acute for Israel and the US.

Investment implications

Global equities are witnessing a typical energy-shock pattern, with a spike in implied volatility, widening risk-premia, and a compression in market beta, as investors temporarily scale back risk budgets amid uncertainty about the persistence and scope of the shock.

Many key oil importers (such as South Korea) have been recent outperformers, and this leaves them more vulnerable to pullbacks, should the uncertainty persist. This is something we see as consistent with the evidence at sector level, where a rotation from financials and more cyclical sectors into energy and defensive names has recently emerged as a consequence of this crisis.

We believe that, beyond the short term, fundamental issues such as the fiscal deficit, high US debt, and high-risk asset valuations in the US are very much in place. Additionally, the unconventional approach of the US President along with a challenging domestic political dynamic persists. Risks around the US tech sector and the private credit space also remain. These challenges reinforce the need for a geographically diversified approach, complementing US exposure with allocations to Europe and Emerging Markets.

Authors