Summary

Rally fatigue: dichotomy between markets and economy too wide

The dichotomy between the real economy and markets is increasing even as the earnings outlook is getting weak, leading us to be sceptical of the risk rally.

The year started with a rally mood amid short covering and the return of retail investors’ risk appetite. There were some supporting reasons for the situation, at least in Europe and China, where lower gas prices and China reopening helped to remove some of the downside economic risks that were on the table last year. However, the rally has gone too far based on assumptions that inflation is falling fast, the job of central banks is done, and the economy is well on track for a soft landing, with no earnings recession.

The tricky part for investors starts now. The bears may not arrive, but some caution from here is necessary. The dichotomy between loose financial conditions and tight lending standards for the real economy is striking. Markets remain priced for perfection, despite high uncertainty and divergences on the economic front. In particular, while we recently upgraded our forecasts for 2023, the devil is in the detail. Regarding the US, our GDP forecast is unchanged, but we see deteriorating quarterly dynamics for the second part of the year. For the Eurozone, we upgraded our GDP projections for 2023, but this was mainly due to carry-over from last year and growth expectations remain flattish. China reopening is clearly a positive for the global economy, but we believe this will mainly support the domestic performance.

Secondly, inflation is declining slowly, but markets see it falling rapidly and the path towards the 2% CB target appears to be long and bumpy. With regard to central banks, we see that the Fed is close to the end of tightening, but the ECB is still hawkish. Finally, appetite for emerging markets is returning, but regarding developed markets, caution prevails.

Against this fragmented backdrop, we think investors should remain cautious but recognise that uncertainty is high on both sides (upside and downside).

Consequently, we updated some of our main convictions as follows:

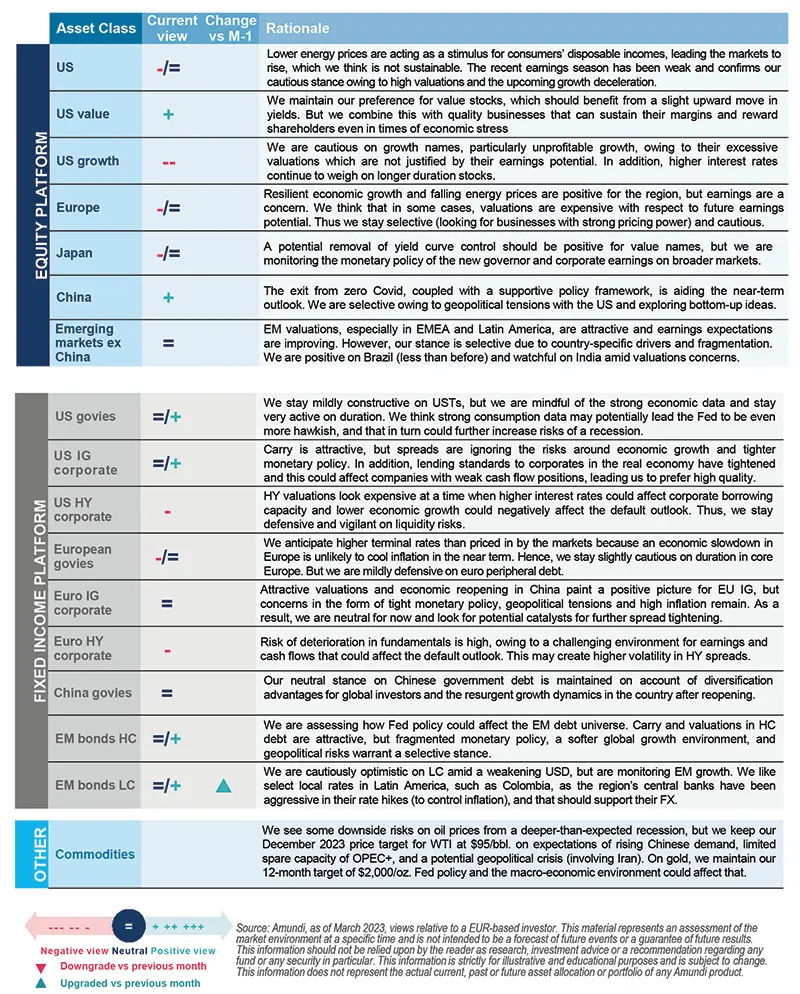

- In cross assets, we stay cautious on equities, as the risk rally may have gone too far, given the pressures on corporate earnings. But, we see a possibility of benefitting from equity upside through options. We think subdued real wage growth is likely to keep demand and consumer spending in the US and Europe weak, eventually affecting earnings. Investors should maintain strong diversification through oil and FX and strengthen protection through equity hedges and gold.

- In bonds, investors should play curve opportunities from diverging monetary policies and favour IG credit. While we stay defensive on duration, mainly core Europe and Japan, we are back to a neutral view on the UK and China. In US fixed income, in contrast, we have a modest positive duration view on expectations of further weakening in the growth outlook, given the tightening in financial conditions over the last year. In credit, we confirm our prudence regarding HY, where the default outlook is deteriorating. We continue to favour IG credit ⎼ in particular, in Europe, where valuations are cheaper than in the US.

- In equities, we are cautious on the US, but prefer value and quality, industrial and financials to tech and consumer discretionary sectors. Although lower energy prices reduce pressure on households and consumers to some extent, the shocks to real wage growth and fiscal drag are substantial and will be more spread out over time. This means that consumption will remain subdued, and the current earnings season provides indications in the form of negative Q4 EPS growth so far for the S&P 500. From a style perspective, investors should combine value stocks with quality and dividend names, which can supplement income. Our overall assessment highlights the importance of identifying companies with strong pricing power.

- EM outlook improving. We have upgraded our view on EM FX now as the USD is weakening on the back of an expected less aggressive Fed this year, and it is likely that peak dollar is behind us. Although we are still neutral to slightly cautious on EM FX, we believe that the asset class can do well this year. Our views are partially moderated by a weak growth outlook for the year. We are more comfortable with local rates in EM, especially in LatAm. On equities, we have increased our positive stance on China and believe that the reopening should be positive for countries that have strong trade relations with China. On India, however, we have taken a cautious stance in the short term on valuations, but the long-term story remains intact.

Three hot questions

|

Monica DEFEND |

We believe a bull steepening of the US yield curve will be a pre-condition for the US equity cycle to start in a sustainable fashion.

1| What are the latest changes to your growth forecasts?

We have downgraded our expectations for Q4 2023 US GDP growth to 0.0% from 0.4%, year-on-year. US growth dynamics are expected to deteriorate in H2 2023, due to investment weakness and slowing private consumption. Eurozone GDP growth in 2023 has been upgraded as we moved progressively to 0.2% from -0.5%, owing to improving incoming data and 2022 carryover effects. However, major headwinds remain and domestic demand is weakening.

Investment consequences

- Equities: confirm our cautious stance on developed market equities.

- Credit: defensive on high yield but constructive on investment grade.

2| What are the prospects for CB rate cuts?

The recent slowdown in US inflation has been the easy part ⎼ any further progress should be more costly in terms of jobs. Against such a backdrop, the Fed should remain cautious and start cutting rates in January 2024. In the Eurozone, we do not foresee a rapid decline in either headline or core inflation.

Investment consequences

- We remain neutral on US rates. We see scope for a deeper curve inversion in the short term, due to more front-loading, while the curve should bull-steepen in the medium term.

- We confirm our cautious stance on euro duration.

3| What triggers could lead to entering equities?

The year-to-date equity rally was triggered by a few factors, including China’s reopening, a less hawkish CB stance, the softening of the EU energy crisis, and the depreciating dollar. We are unsure whether China’s reopening will be enough to offset the negative impulse from slowing US growth. A bull steepening of the US yield curve has always been a pre-condition for the US equity cycle to start in a sustainable fashion.

Investment consequences

- We favour value in both the United States and Europe.

- We are positive on high-dividend stocks, except in Japan, where we focus on value due to the likely upcoming removal of yield-curve controls.

Don’t add risk amid macro uncertainty

|

Francesco SANDRINI |

John O'TOOLE |

Headwinds to economic growth remain and hence without increasing their risk, investors should explore alternative ways to participate in the rally: for instance through derivatives.

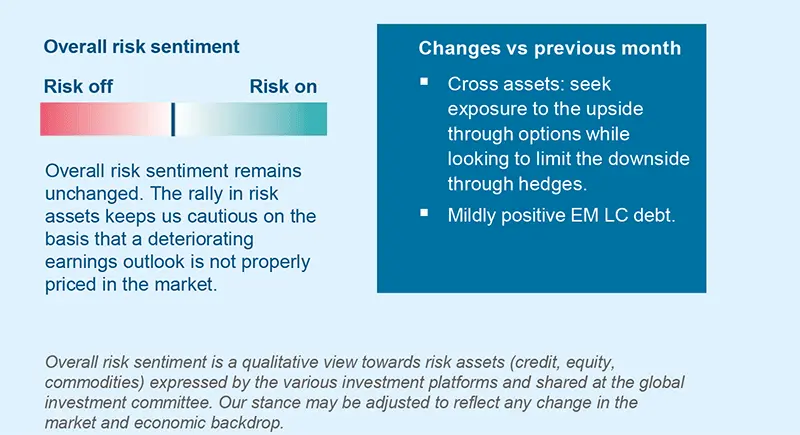

Decelerating inflation, coupled with central banks’ less hawkish stances, is misleading the markets into believing that rising prices will come under control soon. At the same time, financing conditions and lending standards for consumers and corporates in the real economy are tightening and this could affect consumption. This may result in further deterioration in earnings dynamics in a context of expensive valuations. We remain defensive, but exploit opportunities to use derivatives to seek to participate in potential upside without adding risk. Investors should also enhance protection and diversification through FX, commodities and gold.

High conviction ideas

We are cautious on developed market equities (US, Eurozone, Japan). We also observe that changing market volatility could reveal ideas and allow investors to benefit from tactical market movements. In addition, we continue to see relative value opportunities favouring US small caps over expensive large caps, but are assessing how slowing rate hikes could affect this view. In EM equities, we maintain our positive view on China on the back of an improving growth outlook and cheap relative valuations. As far as flows and investor positioning are concerned, China still has room to recover capital flows, given that a lot of money moved away from the country last year.

In fixed income, we keep a positive view on US duration, given the decelerating pace of rate hikes by the Fed and weak growth prospects. But we are active and are monitoring labour markets in terms of job creation and the narrative that the Fed may have to keep rates higher for longer. Elsewhere, we look for opportunities across the globe. For instance, in Japan, we keep our cautious stance on government bonds, but see the potential for the 2Y-10Y curve to steepen in Canada. In Europe, we are positive on 10Y BTP-Bund spreads, which have been resilient to repricing of terminal rates following the ECB’s hawkish views. China’s economic reopening and a decline in energy prices should help the Italian economy, supporting public finances and BTPs. In corporate credit, we stay cautious on EU HY as we believe the credit rally has gone too far and is not in line with our risk scenario. Further, the large amount of supply, though well received by the market, needs to be digested and we are already seeing profit-taking in some segments. Looking ahead, we expect credit flows to be less supportive of spreads.

The FX pillar allows us to play our tactical as well long-term views. Lower energy prices would mitigate the effects of the cost-of-living crisis in Europe, aiding near-term growth. This makes us positive on the EUR vs the GBP. We have a positive stance on the JPY vs the EUR as the yen could benefit from still-weak global growth. We also stay positive on the NOK/CAD for valuation reasons. In EM, we are now constructive on the ZAR/USD. The rand offers an attractive risk/return profile, and we believe the political uncertainty embedded in the FX is excessive.

Risks and hedging

Diversification and portfolio protection remain two of our key objectives and we continue to use commodities (oil, gold) and financial derivatives to achieve that. We think structural imbalances, China reopening, and geopolitical risks (Iran tensions a major risk) could provide a fillip to oil. We also think investors should keep hedges in HY credit and strengthen protection on US equities.

Balancing attractive credit yields with selection needs

| Amaury D'ORSAY Head of Fixed Income |

Yerlan SYZDYKOV Global Head of Emerging Markets |

Kenneth J. TAUBES CIO of US Investment Management |

Yields in credit markets are attractive, but higher funding costs and a slowing economic backdrop call for a selective approach.

Overall assessment

Markets are backing a soft-landing scenario where they do not see a recession and prices are back to central bank targets. We think, however, there is ample uncertainty around labour markets, consumption and corporate earnings. Funding costs in the real economy are also tight. It is difficult for interest rates in the economy to fall without policy cuts by central banks and this looks unlikely in the near term as inflation is still high, even though the pace is declining. We do not expect the Fed to start rate cuts before January 2024 and the ECB is unlikely to cut rates any time soon. Hence, investors should seek to continue to benefit from the attractive yield environment in credit, but prefer high-quality credit, and explore select EM debt as the environment for the latter improves while staying cautious on high yield.

Global and European fixed income

We remain active on duration, with a slightly cautious stance particularly in core Europe and Japan, but upgraded our view on the UK and China duration to neutral. We are also exploring curves across geographies and now see potential for curve steepening in the US, Europe and Canada. On euro peripheral debt, we keep a marginally defensive stance overall. In light of a mixed picture on earnings and growth, we stay very selective in credit and maintain our mild positive stance mainly in IG and subordinated financials, among others. But as far as HY is concerned, we think investors should hedge tactically, owing to concerns on potential defaults. On the other hand, we are vigilant in the covered bonds segment.

US fixed income

We acknowledge that economic data are uneven and there is a possibility that the Fed may tighten policy to a point where the economy weakens. But yields repricing could also happen on the upside if inflation remains high. Thus, with a constructive view for now, we stay very active on duration, vigilant on Fed rhetoric, and think that timing is important. TIPS also look attractive in the intermediate range. On securitised credit, we are positive but believe the recent performance could provide a window to take advantage of spread tightening and alter the stance to be more conservative in future, in line with slowing growth. In corporate credit, we remain selective, with a preference for financials over non-financials and industrials, and IG over HY. Overall, investors should consider taking profits where market rallies present opportunities, and in HY maintain low beta.

EM bonds

Movements in US rates and policy are affecting the environment for EM debt, leading us to be very vigilant. We see opportunities in HC, local rates and FX. However, we are selective, as geopolitical and country-specific risks persist. We are constructive on commodity exporters (Brazil, Mexico, South Africa, Indonesia), thanks to China’s reopening. Interestingly, countries, such as Colombia, where CBs have been proactive, look attractive.

FX

We are positive on select high-carry EM FX, such as the MXN, BRL, IDR and ZAR. However, we balance this view through a constructive stance on safe-haven FX, such as the JPY, even as we stay neutral on the USD. Another major risk on our radar is the escalation of the Russia-Ukraine war, which could negatively affect the PLN and CZK.

Valuation dispersion supports value opportunities

| Kasper ELMGREEN Head of Equities |

Yerlan SYZDYKOV Global Head of Emerging Markets |

Kenneth J. TAUBES CIO of US Investment Management |

Higher dispersion in valuations leads to potential stock opportunities, in particular, in the value space.

Overall assessment

Markets have been rallying on the back of a receding energy crisis, China reopening, and a semblance of peaking central bank hawkishness, even as earnings season has been subdued so far. In the US, consensus expectations for 2023 operating earnings and profit margins look implausible, given concerns on consumption and the deceleration in growth. In Europe, an expected slowdown in earnings is confirmed, despite some near-term improvement in the economy. Thus, instead of rooting for markets, investors should explore businesses that can sustain margins and reward shareholders, but offer attractive valuations. We believe such businesses can be identified by strong bottom-up analysis and by combining quality and value investing in developed and emerging markets.

European equities

Based on a balanced style, we explore quality cyclical businesses and defensive stocks, such as consumer staples and pharmaceutical companies. However, given the current environment in which prices in some cyclical sectors have run ahead of their fundamentals, we think investors should consider moving out of them to defensive segments with better risk/reward profiles. In particular, we trimmed our favourable view on financials (still positive though) a little and upgraded pharmaceuticals. Nonetheless, we remain constructive on retail banks, owing to the beneficial effects of high interest rates on their net interest margins. We also like industrial companies that are facilitating the energy transition. With regard to staples, we maintain a constructive stance, selecting names with strong pricing power and robust balance sheets that can provide a shield in times of rising rates. Conversely, we are cautious on utility companies and the technology sector.

US equities

This year’s rally is more a case of multiples expansion, making us cautious overall as valuations are expensive in some cases. Accordingly, we think investors should avoid risky, high beta names that are now excessively dependent on an unpredictable economic cycle. In contrast, we prefer businesses committed to returning cash to shareholders: for example, among defensives. Here, we focus on names that show reasonable valuations even if this means going beyond traditional defensives. Two such examples are health care equipment & services and life science tools sectors. But we see very little value in staples, utilities and real estate. At the other end, in cyclicals, our highest conviction sectors are energy and banks. We also like capital goods & materials among cyclicals, but prefer idiosyncratic stories that should be able to outgrow the cycle. However, the rebound witnessed in cyclicals since last October has made consumer discretionary and industrial names more exposed to the risk of an economic contraction.

EM equities

We maintain a cautiously optimistic outlook on the back of China reopening, reasonably attractive valuations, and earnings dynamics. However, investors should stay selective and focus on fundamentals. Our main convictions are China and Brazil, but regarding the latter, we are less positive than before owing to political volatility. We see some valuation concerns in India, but the long-term story looks intact. From a sector perspective, we are positive on discretionary and real estate, and remain cautious on health care.

Amundi asset class views

Definitions & Abbreviations

-

ADR: A security that represents shares of non-US companies that are held by a US depositary bank outside the US. They allow US investors to invest in non-US companies and give non-US companies access to US financial markets.

-

Agency mortgage-backed security: Agency MBS are created by one of three agencies: Government National Mortgage Association, Federal National Mortgage and Federal Home Loan Mortgage Corp. Securities issued by any of these three agencies are referred to as agency MBS. Beta: Beta is a risk measure related to market volatility, with 1 being equal to market volatility and less than 1 being less volatile than the market.

-

Breakeven inflation: The difference between the nominal yield on a fixed-rate investment and the real yield on an inflation-linked investment of similar maturity and credit quality.

-

Carry: Carry is the return of holding a bond to maturity by earning yield versus holding cash. Core + is synonymous with ‘growth and income’ in the stock market and is associated with a low-to-moderate risk profile. Core strategy is synonymous with ‘income’ in the stock market.

-

Correlation: The degree of association between two or more variables; in finance, it is the degree to which assets or asset class prices have moved in relation to each other. Correlation is expressed by a correlation coefficient that ranges from -1 (always move in opposite direction) through 0 (absolutely independent) to 1 (always move in the same direction). Credit spread: The differential between the yield on a credit bond and the Treasury yield. The option-adjusted spread is a measure of the spread adjusted to take into consideration the possible embedded options. Currency abbreviations: USD – US dollar, BRL – Brazilian real, JPY – Japanese yen, GBP – British pound sterling, EUR – Euro, CAD – Canadian dollar, SEK – Swedish krona, NOK – Norwegian krone, CHF – Swiss Franc, NZD – New Zealand dollar, AUD – Australian dollar, CNY – Chinese Renminbi, CLP – Chilean Peso, MXN – Mexican Peso, IDR – Indonesian Rupiah, RUB – Russian Ruble, ZAR – South African Rand, TRY – Turkish lira, KRW – South Korean Won, THB – Thai Baht, HUF – Hungarian Forint.

-

Curve flattening: A flattening yield curve may be a result of long-term interest rates falling more than short-term interest rates or short-term rates increasing more than long-term rates.

-

Curve steepening: A steepening yield curve may be a result of long-term interest rates rising more than short-term interest rates or short-term rates dropping more than long-term rates.

-

Curve inversion: When long-term interest rates drop below short-term rates, indicating that investors are moving money away from short-term bonds.

-

Cyclical vs. defensive sectors: Cyclical companies are companies whose profit and stock prices are highly correlated with economic fluctuations. Defensive stocks, on the contrary, are less correlated to economic cycles. MSCI GICS cyclical sectors are: consumer discretionary, financial, real estate, industrials, information technology and materials. Defensive sectors are: consumer staples, energy, healthcare, telecommunications services and utilities.

-

Duration: A measure of the sensitivity of the price (the value of principal) of a fixed income investment to a change in interest rates, expressed as a number of years. High growth stocks: A high growth stock is anticipated to grow at a rate significantly above the average growth for the market. Liquidity: The capacity to buy or sell assets quickly enough to prevent or minimise a loss. P/E ratio: The price-to-earnings ratio (P/E ratio) is the ratio for valuing a company that measures its current share price relative to its per-share earnings (EPS).

-

QE: Quantitative easing (QE) is a type of monetary policy used by central banks to stimulate the economy by buying financial assets from commercial banks and other financial institutions.

-

Quality investing: This means to capture the performance of quality growth stocks by identifying stocks with: 1) A high return on equity (ROE); 2) Stable year-over-year earnings growth; and 3) Low financial leverage.

-

Quantitative tightening (QT): The opposite of QE, QT is a contractionary monetary policy aimed to decrease the liquidity in the economy. It simply means that a CB reduces the pace of reinvestment of proceeds from maturing government bonds. It also means that the CB may increase interest rates as a tool to curb money supply.

-

TIPS: A Treasury Inflation-Protected Security is a Treasury bond that is indexed to an inflationary gauge to protect investors from a decline in the purchasing power of their money.

-

Value style: This refers to purchasing stocks at relatively low prices, as indicated by low price-to-earnings, price-to-book and price-to-sales ratios, and high dividend yields. Sectors with a dominance of value style: energy, financials, telecom, utilities, real estate.

-

Volatility: A statistical measure of the dispersion of returns for a given security or market index. Usually, the higher the volatility, the riskier the security/market.

-

Yield curve control: YCC involves targeting a longer-term interest rate by a central bank, then buying or selling as many bonds as necessary to hit that rate target. This approach is dramatically different from any central bank’s typical way of managing a country’s economic growth and inflation, which is by setting a key short-term interest rate.

Authors