Summary

Space dreams versus Earth reality

Over the last month, central banks have taken an increasingly hawkish turn that has forced markets to start reassessing the AI trade’s remarkable momentum. As inflation continues to rise, policymakers have remained cautious despite positive headlines around a US/Iran ceasefire deal.

Optimism around the AI trade has been the main driver of risk assets, with momentum stocks leading. But due to rising uncertainty on potential future hikes, markets have started to question whether AI’s elevated valuations can remain justified, particularly in a more uncertain interest-rate environment with increasing IPO supply. Rotations have already started to materialise, as investors take profits and broaden exposure into less crowded areas of the market.

Looking ahead, concerns around AI profitability, valuations and concentration risks are likely to persist. Capex overspending and lacklustre results remain key risks for US hyperscalers, especially as the recent rally in memory-chip makers may be showing signs of excess. Well-backed IPOs can help support the market, but more players and more metrics for assessing the AI space will increase the scrutiny of current leaders and could drive broader diversification. Against this backdrop, we still see growth holding, but not strongly enough to offset rising macro costs and broadening price pressures.

Shipping disruptions in the crucial Strait of Hormuz are expected to ease over the second half of this year, even though the deal is fragile and some geopolitical premium on oil prices will likely persist. Oil prices have fallen from their peak, remaining above pre-war levels. The US economy should remain resilient, while Europe looks more exposed, given its strong external dependence on oil and gas at a time of low inventories.

Central banks in focus. The ECB is reacting to incoming data and adjusting policy to inflation pressures. We expect one more hike this year, but visibility remains low, with much depending on how far inflation deviates from target and for how long. The Fed is expected to remain on hold this year, although the risk of rate hikes could increase if higher energy costs feed into broader prices and economic growth accelerates.

A scenario of fragile de-escalation in the Middle East. The next six months will test the resilience of our scenario, which assumes a fragile de-escalation of the Middle East crisis and a reopening of the Strait of Hormuz, although the path to a stable deal remains uncertain. Any re-escalation of the conflict may weigh on growth, tighten financial conditions, and put pressure on equities and bonds, while supporting commodities and gold as safe-haven hedges.

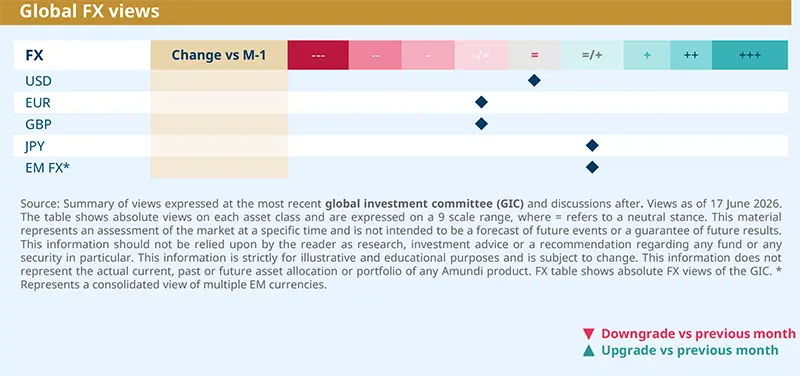

Tactical appeal for the USD, but structural USD weakness is likely to continue. While we believe the long-term case for USD weakness remains intact, amid resilient growth relative to the rest of the world, ongoing inflation pressures and a hawkish Fed, some resilience in the near term is possible.

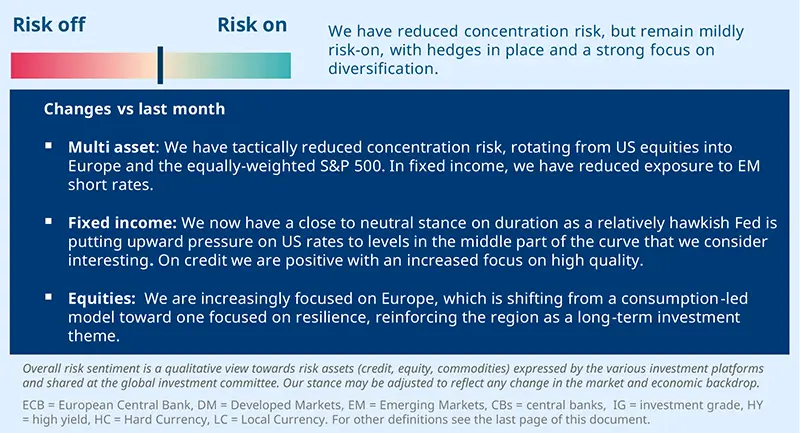

In conclusion, the less benign economic backdrop is, for now, offset by liquidity and solid earnings growth. We therefore maintain a cautious risk-on stance, recently further trimmed down, with hedges in place and a focus on diversification away from concentration risk.

Diversification is paramount as investors start to move away from overcrowded areas, taking profits and making room for new IPOs.”

| Amundi Investment Institute: A new Fed era under Wash |

Fed focusing on price stability and task forces. At his first meeting as Chair, Kevin Warsh was explicit that the FOMC will prioritise price stability. He has signalled a new monetary policy regime by announcing five task forces. These will examine the Fed’s framework for inflation analysis, productivity, communications, data sources, and, most importantly, the balance sheet. The latter has significant implications for market liquidity and the US dollar, given its enormous size. The focus on inflation remains paramount. Assessing inflation pressures. Recent data have already highlighted an increase in producer prices and headline inflation, while core inflation remains relatively benign. Core goods prices have fallen, as price declines have spread across many goods categories previously boosted by tariffs, and core services have risen largely due to the shelter component, which may moderate going forward. PPI dynamics and the price component of the ISM and PMI need to be monitored, as they are at the early stage of pass-through. |

Monica DEFEND

Broad-based price pressures are now showing up across the economy, not just in energy. How quickly these costs pass through will matter for corporate margins and consumers’ real incomes.

Overall, in assessing where to invest, we should look beyond short-term headlines and focus on structural resilience, pricing power, and the ability of companies to absorb shocks — qualities that can be found across regions and sectors. Our convictions across asset classes are outlined below:

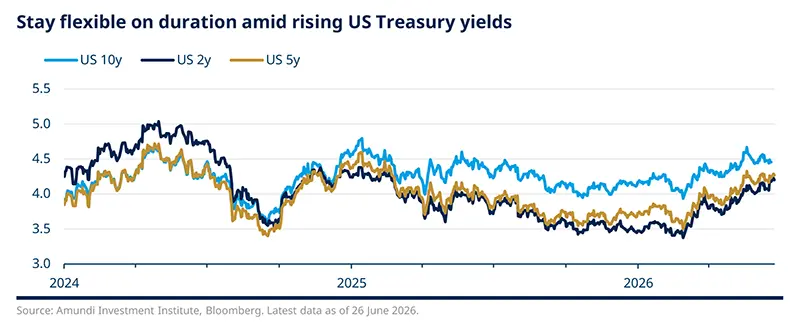

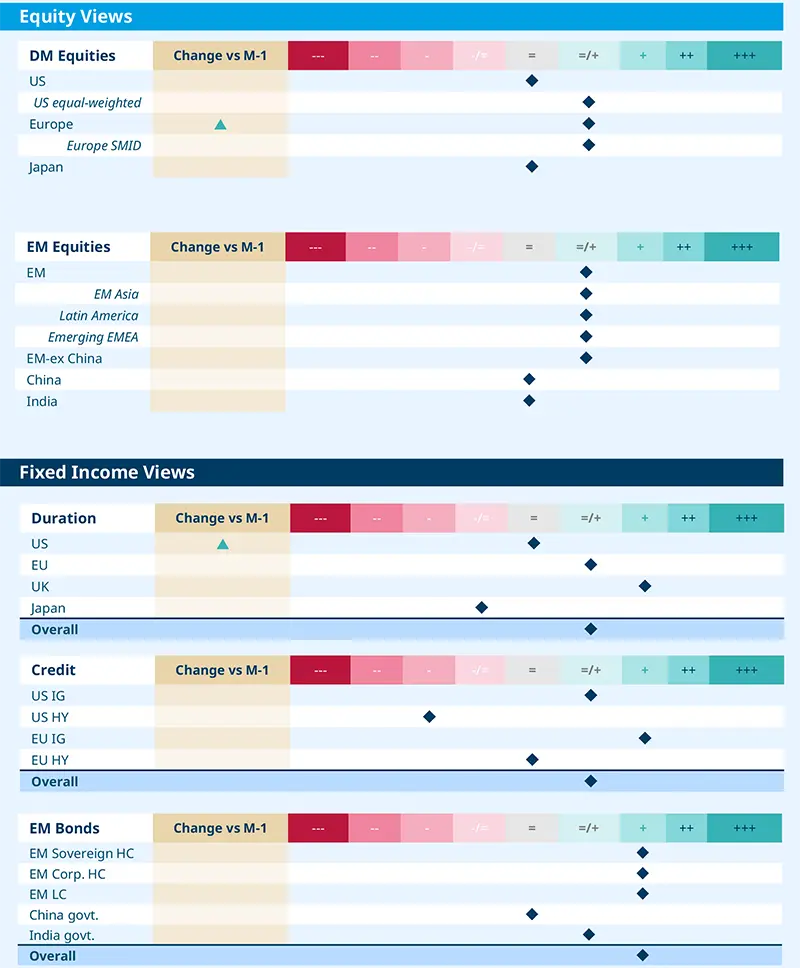

In fixed income, we maintain our slightly cautious, close to neutral stance on US duration, given resilient labour data, sticky inflation and a more hawkish Fed. In Europe, even if the ECB hikes rates this year, we do not see a full-fledged hiking cycle, which supports the front end of the curve; here we favour peripheral debt over core. In the UK, we do not expect a full hiking cycle and remain constructive on duration, particularly at the short end, although fiscal risks warrant caution. High-quality credit still offers attractive yields while we remain constructive on EM debt, especially in Latin America.

In equities, we maintain a balanced approach, focusing on resilient businesses and strong balance sheets, with exposure in attractive defensive sectors, such as consumer staples and healthcare, and quality cyclical stocks in industrials and materials.

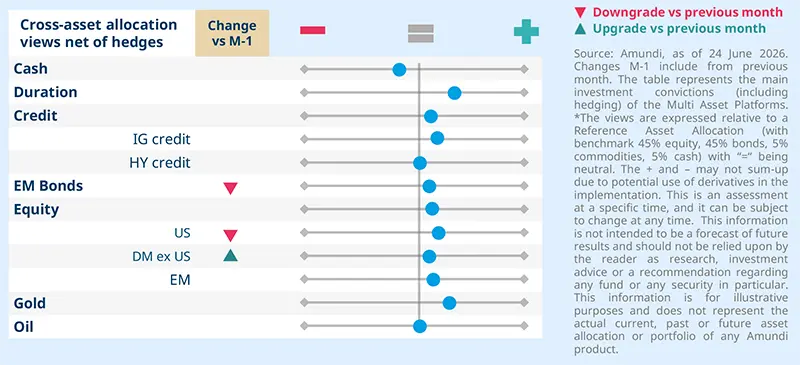

In multi asset, we maintain a slightly pro-risk stance, but we have reduced concentration risk by trimming exposure to US equities and diversifying into Europe and into the equally-weighted S&P 500. In fixed income, we remain positive on European duration and European investment grade credit. We have marginally reduced exposure to EM short rates.

We remain mildly constructive on risk, with a stronger emphasis on diversification to reduce concentration risks. Focus is on selectivity and fundamentals, with a preference for resilience to momentum.

FIXED INCOME

Balancing inflation and growth risks

Amaury D’ORSAY |

Under a “fragile de-escalation" scenario, inflation is likely to remain above central banks’ targets for longer, with rising risks of second-round effects, particularly in Europe, where the growth outlook remains fragile. In the EU, in particular, we think markets are currently underestimating growth risks and, consequently, we do not expect a full-fledged hiking cycle by the central banks (ECB, BOE), which makes the short end of the curves attractive

In the US, robust labour data, high headline inflation and a relatively hawkish Fed are putting upward pressure on US rates, to levels that we consider interesting in the middle part of the curve.

For the US, we have a neutral stance on duration, seeing value in the 5-year tenor, and continue to expect curve steepening. In the Euro Area, we are positive on the short end of the curve, as markets have yet to fully price in deteriorating growth. We favour peripheral over core.

In the UK, we do not expect a hiking cycle and remain positive on duration, particularly at the short end, as valuations are more attractive. We remain aware of the fiscal risks.

In Asia, we remain cautious on Japanese bonds.

- We remain constructive on credit overall, as fundamentals remain robust and the search for yield continues to support the asset class.

- We continue to favour EU IG, supported by strong fundamentals and valuations. We are slightly positive on US IG due to inflation shock resilience. At a sector level, we prefer financials over non-financials.

- We keep our preference for subordinated over high yield.

We maintain a constructive view on EM debt. Overall, liquidity conditions remain favourable, although Fed policy is a key factor to monitor.

We are positive on EM hard currency debt, with selective opportunities in the corporate market to playing the technology and green transition themes.

Local currency bonds offer strong carry but we favour a selective approach country-wise, rather than a broad exposure, with a tilt towards Latin American commodity exporters.

EQUITIES

An industrial play for Europe

Barry GLAVIN |

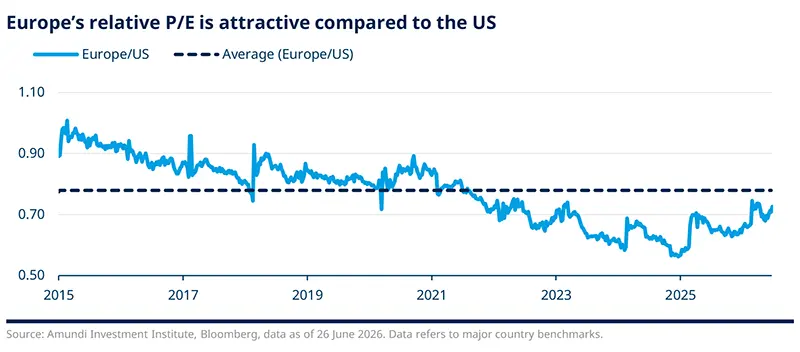

Markets have remained supported by earnings growth, helping to offset concerns over rising US yields. Looking ahead, monetary policy actions and policy stance will be key factors to monitor. Strategically, we continue to see high valuation and concentration risks in the US. Hence, we favour Europe, Japan and EM. Europe, in particular, is shifting from a consumption-led model toward one focused on resilience, reinforcing the region as a long-duration investment theme.

In Japan, the equity market outlook remains constructive, with earnings momentum driven by banks and AI-related stocks. Emerging markets are also supported by their appeal as a source of diversification amid geopolitical and economic uncertainty.

Using a balanced approach, we focus on resilient businesses with strong balance sheets, particularly in consumer staples, industrials and materials.

In Europe, we have added exposure to food ingredients companies, which offer above-GDP growth, non-cyclical demand and attractive valuations. By contrast, we have reduced exposure to the European technology sector, after its strong performance. We favour companies exposed to the energy transition, rising electricity demand from AI and data centres, and infrastructure spending, particularly in industrials, capital goods, utilities and construction stocks.

In Japan, the equity market outlook remains constructive. We like small- and mid-cap stocks exposed to supply-chain resilience, AI and infrastructure.

EM equity valuations remain attractive. Successful IPOs in the tech space could support spending on chips and memories, giving a boost to EM tech stocks. However, volatility could remain high as markets are concentrated.

We maintain a neutral stance on India, as valuations are still demanding, its status as a commodity importer and its limited exposure to the AI theme. We could mildly increase our stance amid easing oil pressure.

We remain neutral on China, as its earnings outlook remains uncertain due to overcapacity in many industries and unclear real estate data.

We maintain a positive view on Latin America. In Brazil, earnings and profitability remain high, although elections in October will be key to watch.

MULTI-ASSET

Mildly pro-risk, with an emphasis on selectivity

Francesco SANDRINI CIO Italy & Global Head of Multi-Asset | John O’TOOLE Global Head - CIO Solutions |

May was positive for risk assets, but the macro backdrop weakened slightly. Growth is becoming more uneven while inflation is showing more clearly in the data across the US, the Euro Area and the UK, leaving central banks less comfortable. Against this backdrop, the tone remains mildly pro-risk, with greater selectivity.

We remain mildly positive on equities, supported by strong earnings, but have reduced concentration risk by lowering our exposure to US equities and diversifying into Europe and the equally-weighted S&P 500. European equities remain under-owned and have lagged the US, but we see potential for a rebound in H2. Given persistent uncertainty, we continue to maintain protection on the US and the Euro Area.

In fixed income, we remain long US 5-year duration, as this part of the curve still looks attractive. In Europe, we maintain a long-duration bias via Bunds and Schatz. While the ECB is likely to hike rates once more this year, we think it would not completely ignore weakening consumption and growth. In Euro peripherals, BTPs remain attractive, as Italy still appears comparatively stable. However, we remain short 10-year JGBs, given Japan’s policy normalisation, higher energy costs, yen weakness and rising inflation risks. Finally, we remain constructive on EU IG credit, given attractive valuations, demand from yield buyers and positive seasonality. On EM, we have reduced the stance on short-term rates, following the recent move lower.

On FX, USD structural weakness is more likely over the long term; in the near term the currency could find support from a more hawkish Fed. We are positive on AUD/USD to express our bearish view on the US dollar, and remain exposed to the commodity-sensitive story. We are also positive on JPY and NOK versus EUR. The yen will benefit if the economic growth environment worsens, the NOK will gain from Norway’s energy exposure.

VIEWS

Amundi views by asset classes

Definitions & Abbreviations

Currency abbreviations: USD – US dollar, BRL – Brazilian real, JPY – Japanese yen, GBP – British pound sterling, EUR – Euro, CAD – Canadian dollar, SEK – Swedish krona, NOK – Norwegian krone, CHF – Swiss Franc, NZD – New Zealand dollar, AUD – Australian dollar, CNY – Chinese Renminbi, CLP – Chilean Peso, MXN – Mexican Peso, IDR – Indonesian Rupiah, RUB – Russian Ruble, ZAR – South African Rand, TRY – Turkish lira, KRW – South Korean Won, THB – Thai Baht, HUF – Hungarian Forint.

Authors