Summary

Europe’s strategic autonomy is about securing long-term economic resilience, diversifying the region’s external dependencies and enhancing competitiveness. This will open-up long-term investment opportunities across sectors.

- The Munich Security Conference emphasized that strategic autonomy is central to European security.

- Strategic autonomy means reducing dependencies, safeguarding long-term economic resilience and preserving policy space in an increasingly unstable world.

These measures should bolster Europe’s economic prospects, broadening the appeal of European assets.

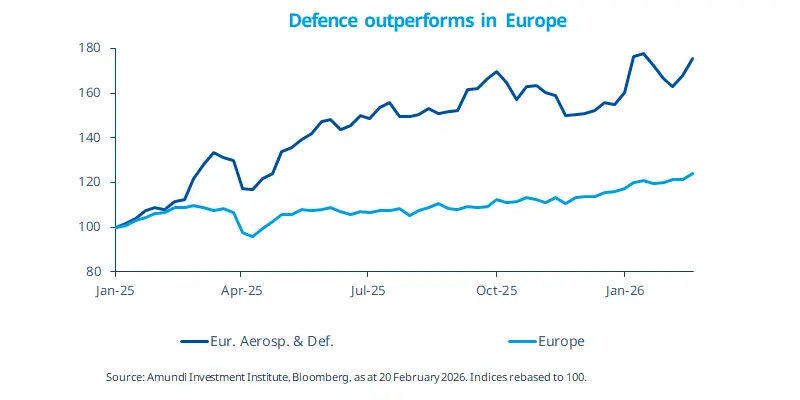

Since the start of the year, successive EU meetings — most recently the Munich Security Conference and an informal EU summit — have highlighted the new security paradigm centred on strategic autonomy. Priorities include reducing security fragmentation, reversing the EU’s declining share in key innovative sectors; cutting energy vulnerability; securing critical raw materials; and strengthening financial stability. Delivering this agenda requires the full policy toolkit: from industrial policy (i.e., EU’s IAA) to fiscal stimulus (i.e., in Germany). Markets are realising this and the defence index outperformance may be an early sign.

The ECB’s new liquidity framework, announced by Christine Lagarde at the Munich Conference, is a signal that the ECB is framing euro liquidity as part of Europe’s geopolitical architecture. More liquid European assets would enhance financial stability, resilience and the Euro’s international role. If implemented, these steps could help unlock Europe's economic potential.

This week at a glance

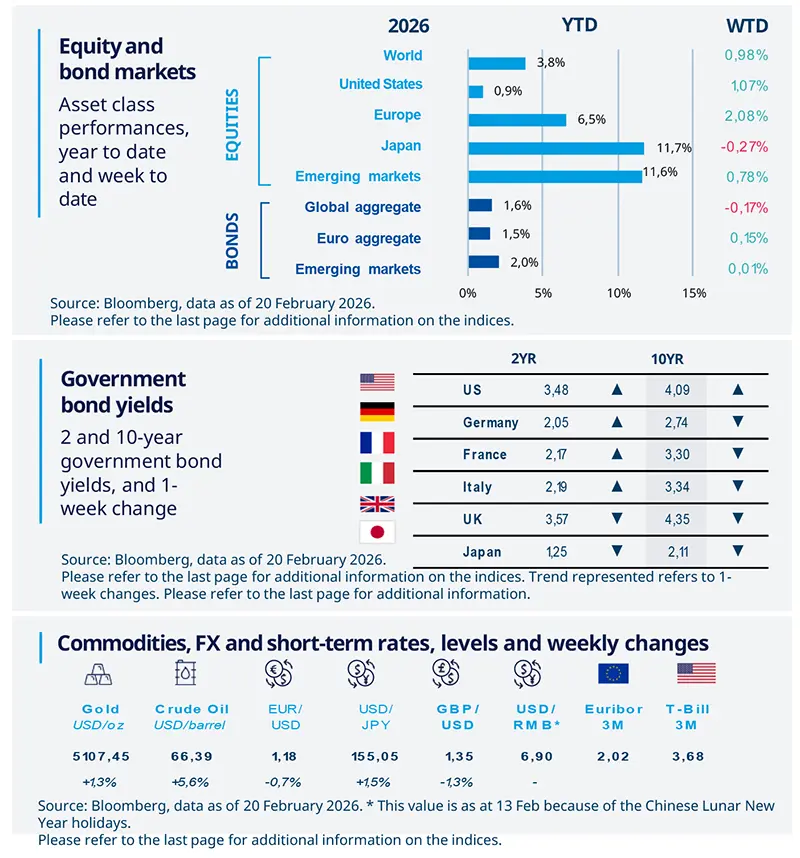

Global equities rose amid easing jitters about AI disruptions and positive US data. The U.S. Supreme Court’s decision on tariffs has led to some uncertainty. Concerns over Middle East tensions were reflected in commodities: oil approached a six‑month high on supply fears and gold rose. In the bond market, positive US macro data pushed Treasury yields slightly higher.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 20 February 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US industrial output in a steady momentum

Industrial output rose 0.7% MoM in January, confirming a steady factory momentum alongside weather-driven energy demand. Manufacturing was the main contributor, with broad gains in durables and non-durable goods. Utilities surged on cold-weather electricity demand, while mining edged down. Capacity utilization ticked up but remains below its long-term average. Overall, this supports our view of stronger momentum in the US economy.

Europe

UK Inflation shows signs of easing

Inflation eased to about 3% YoY in January, largely owing to lower fuel prices and favourable base effects. Inflation excluding volatile components was broadly unchanged. Services inflation surprised on the upside, diminishing the prospect of an immediate March rate cut. Nonetheless, in view of the MPC’s dovish stance, signs of labour market softening and the normalisation of inflation, we forecast reductions in policy rates later in the year.

Asia

Japan GDP disappointed

Japan’s GDP expanded just 0.2% QoQ in Q4, following a 2.6% decline in Q3. The composition was more constructive: private consumption was up for a seventh consecutive quarter despite elevated inflation, business investment rebounded, while real exports continued to fall. With Japanese Prime Minister Takaichi’s fiscal measures expected to lower inflation and restore real‑wage growth, and with sentiment improving, a cyclical recovery is possible.

Key dates

Germany IFO, Mexico GDP |

US Consumer Confidence, EZ CPIK CPI |

Japan retail sales, industrial production; India GDP, US PPI |

Authors