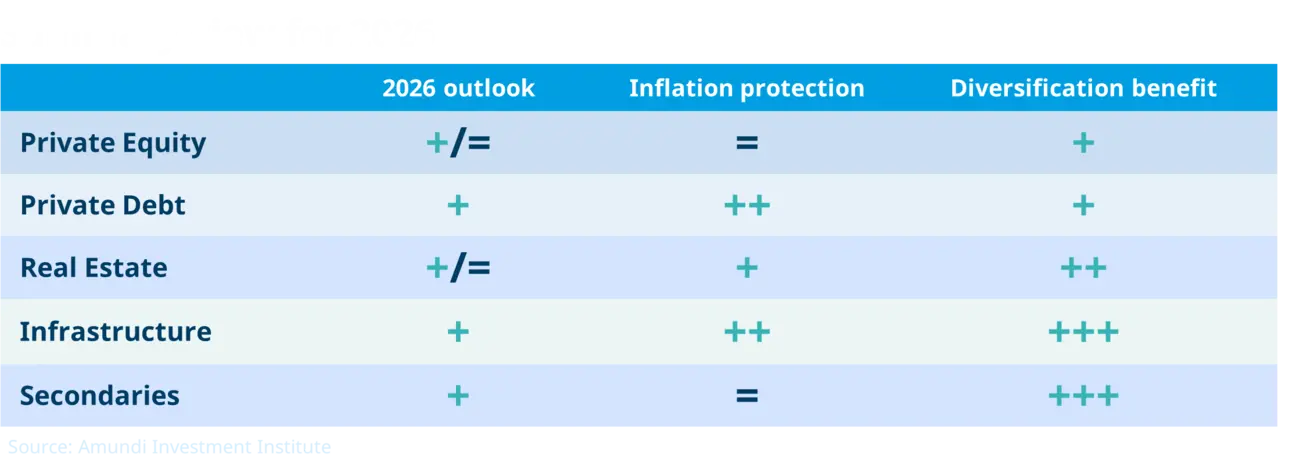

Summary

10 themes for private assets in 2026

A resilient but uneven backdrop favours private markets. As liquidity solutions and transparency improve and deal flow recovers, privates will increasingly compete with listed markets – but outcomes will hinge on sector selection, execution and capital‑structure design.

Our base‑case macro assumes resilient growth, low inflation, mildly accommodative central banks and firmer corporate activity. Given current Middle East uncertainty, we see two alternatives: a short, transitory energy spike (up to ~3 months) with limited impact on private assets; or a prolonged stagflationary energy shock (~6–9 months) that would prompt a flight to quality – slower exits and a delayed private equity recovery, a tilt to secured direct lending in private debt, stronger demand for contracted, inflation‑protected infrastructure, and a focus on prime, income‑generating real estate. In relative terms, such a shock could enhance privates’ appeal versus listed markets by offering greater downside protection in stressed cycles.

Demand for private assets is intact despite the noise: investors still want privates for diversification and outcomes. What makes private assets attractive is their long‑term performance; over time, they have delivered superior net returns after allowing for the cost of illiquidity.

They also offer liquidity‑substitution value, which reduces forced selling and dampens short‑term volatility, alongside alternative return engines and access to non‑public opportunities. The private market universe is heterogeneous, spanning contract‑like, income‑generating strategies to distressed strategies, which seek outsized returns at much higher risk. Privates offer a unique combination of high risk/reward niches alongside more stable income, produced from alternate drivers. That blend allows portfolios to hold steady income while harvesting cyclical upside, which is particularly appealing from a diversification perspective.

Privates are in transition along the classic innovation curve (as hedge funds, mutual funds and investment trusts were before them). The recent strains could signal the natural middle phase of this curve.

Typically, the innovation curve moves from an initial exploration period with high alpha and volatility, through a golden age of attractive, more stable returns, into a consolidation phase where broad adoption compresses the edge and focus shifts to risk management and regulation.

Eventually, a new alpha equilibrium emerges, with robust but reduced alpha, before strategies become commoditised. There are signs that privates may now be moving beyond consolidation, setting the stage for renewed growth.

The US remains the gravitational centre of private markets due to scale and depth. Europe has materially increased its share of private investment, accounting for roughly 34% of global commitments as of Q3 2025, while Asia is growing fast but remains fragmented.

Innovation is accelerating: products and processes are changing fast. They are the new plumbing that will define winners. In particular, liquidity engineering – through secondaries, evergreens, and other wrappers – is re‑pricing illiquidity, shifting negotiating power, and changing how returns are split.

After a couple of years of mixed trends, a recovery is underway. It is uneven and gradual because multiple supply-and-demand and structural frictions clogged the realisation pipeline in 2022–25. That clog is now easing, but past patterns suggest normalisation takes time for vintages to work through – not weeks.

Investors are increasingly requiring evidence of realised outcomes. A thinner illiquidity premium today heightens selectivity and shifts the focus to corporate fundamentals over financial engineering. The adjustment is underway: the market is becoming more disciplined, moving away from weaker structures, rewarding execution and governance. Managers are far more hands-on and favour buy‑and‑build approaches. The winners will be managers who combine sector expertise, permanent operating capability and credible liquidity solutions. Recovery is real but gradual. Patience and operational rigour will drive returns.

Private debt is maturing: as it broadens its client base and deepens its ties to banks, it must improve its valuation and liquidity management. Liquidity remains benign and most exposure sits in senior, secured, floating-rate direct lending – the backbone for yield and liability matching. In the US, AI, renewables, and reshoring push specialists into higher yield niches (ABS, specialty finance). In Europe, mid-market lending and SME refinancing (for consolidation or founder succession) drive growth. Across regions, selectivity, underwriting skill and alignment will beat scale bought at the expense of discipline.

Infrastructure sits at the intersection of the main themes and stands to benefit. Projects offering predictable, contract‑style cash flows or supporting the energy and digital transition remain most desirable. Renewables with storage, grid and transmission upgrades, and long‑term contracted digital infrastructure stand out for their stable revenues and strong demand. Transition enablers and social infrastructure offer potential but carry higher risk and complexity. Overall, projects that rely on a single, volatile merchant price will be riskier for big institutional investors amid elevated rates and tighter construction markets, so selectivity will be key.

Most of the repricing in real estate is likely behind us. Real estate is stabilising, and innovation is widening access to the asset class. But this is a selective stabilisation, not a broad boom: performance should depend less on yield compression and more on asset quality, income resilience and redevelopment upside. This environment favours a cautious re‑allocation towards logistics, data centres and high quality residential assets. We currently believe that the overall performance of real estate will be less driven by market yield compression than in the previous cycle, which reinforces the importance of rental income and market rent growth.

Key risks for privates in 2026 are rising real yields, regulatory and tax uncertainty, and competition for top‑tier deals – amplified by AI volatility and geopolitics. As private markets scale and deepen links with banks, reinsurers and non‑banks, shocks could also become more systemic. Banks fund private markets and often concentrate exposures with a handful of large counterparties; insurers also frequently cede private risk to reinsurers or offshore SPVs that themselves hold private assets (often managed by the same sponsors). Private‑asset valuations are model‑based and infrequent, and funding chains are opaque. Consequently, private‑market stress can trigger a liquidity “cliff” – rapid margin and collateral calls, forced asset sales and non‑linear losses that cascade across banks, insurers, other non‑banks, and the securities‑finance plumbing.

Selective, opportunistic alpha is re-emerging in private equity and real estate as the recovery proceeds.

In 2026, private markets should benefit from resilient growth and moderating rates, but alpha will depend less on market direction and more on selectivity, execution, and disciplined capital allocation.

Macro trends in 2026 that will matter for private assets

Favourable leverage conditions and activity dynamics should support private markets overall, but a clear divergence is emerging between high growth sectors (tech, cloud, logistics, select healthcare, renewables) and laggards (hospitality, traditional retail, some office markets, low margin SMEs). We expect asymmetric flows, funding conditions, valuations and exit windows across sectors: many micro‑cycles, not one uniform market.

A prolonged stagflationary shock from the Middle East escalation, not our base case, could trigger a flight to quality—slower exits, delayed PE recovery, a shift to secured direct lending, stronger demand for contracted and inflation‑protected infrastructure, and a focus on prime, income‑generating real estate.

Modest monetary easing followed by a plateau should reduce immediate refinancing stress but keeps discount‑rate sensitivity front‑of‑mind for valuations and makes it critical for long‑dated, capex‑heavy projects, such as greenfield projects whose cash flows are far in the future and thus highly sensitive to rates.

The AI boom continues to broaden downstream and regionally. It creates productivity upside but also raises doubts about profitability, valuations, and cannibalisation. For private investors, Artificial Intelligence (AI) acts as a sourcing and operations multiplier, not an automatic Internal Rate of Return (IRR) booster.

Political and geopolitical noise increases ahead of US midterms. This could bring potential regulatory and tax noise, especially in consumption-sensitive sectors. Private assets (PA) are not disconnected from geopolitical risk, but impacts tend to be lagged and smoothed. They are more sensitive to financial and economic uncertainties. Periods of stress can create opportunities (around Europe’s push for strategic autonomy for instance) and typically increase secondaries activity for opportunistic buyers.

A mid-cycle phase in credit is emerging. Credit spreads could slowly erode with more differentiation across borrowers, but without major shocks – a dynamic that would benefit private debt (PD) and parts of infrastructure (Infra) where underwriting and security selection matter more than index moves.

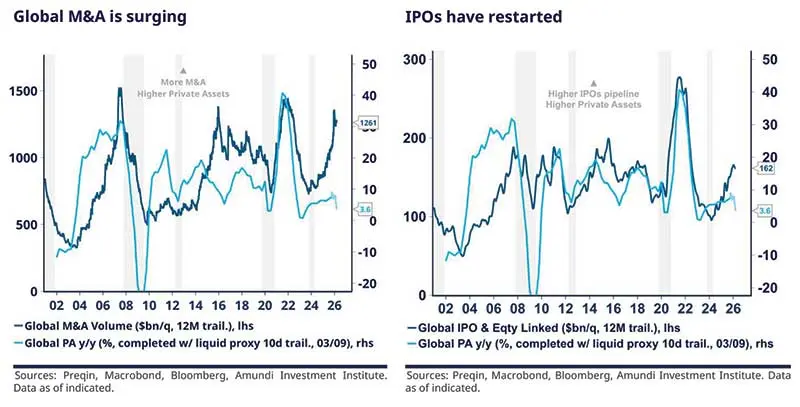

Accelerating corporate activity is reopening M&A and IPO pipeline. Strategic bidders are returning, sponsor‑to‑sponsor transactions and carve‑outs are rising, all supportive of exits for well‑positioned General Partners (GP). Given low corporate leverage on average, companies have room to re-leverage prudently.

Private equity: gradual recovery

From pause to purpose

Multiple frictions clogged the realisation pipeline from 2022 to 2025. Rapid fundraising outpaced buyer capacity while IPO windows and strategic M&A narrowed. High pre‑2022 entry prices and rapid rate hikes made exits harder and refinancing costlier. GP‑led continuations and private credit funding preserved NAVs but delayed DPI, while staffing, tougher governance, and regulatory scrutiny slowed decisions. As a result, confidence weakened and capital concentrated, hitting mid‑tier and emerging managers hardest.

However, the picture is more nuanced. Some segments have remained resilient, and part of the issue reflects one-off Covid-era distortions. Fundraising is not down evenly but has instead concentrated in the top quartile of managers, whether defined by performance or scale. Performance is also polarised: high‑quality deals continue to hold up, while turnaround and distressed still deliver, albeit across a more selective set of opportunities. Meanwhile, liquidity innovations have absorbed some pressure even though they do not solve the DPI problem entirely.

At the same time, large pensions, insurers and SWFs are long‑term allocators with planned allocations to alternatives, making them unlikely to materially reallocate away from PE in response to short‑term softness. Likewise, doubts about valuations may be overstated: secondary pricing shows limited discounts, while liquid proxies help triangulate NAVs without revealing broad gaps.

A handful of stressed vintages were magnified by the post‑Covid rebound, and as those distortions unwind, the path to orderly realisations strengthens. PE underperformance is also common when public cyclical assets rally, and private returns typically lag when the cycle firms.

| Three paradoxes that shape the backdrop |

Abundant liquidity yet scarce distribution. Secondary discounts sit in the single digits, the illiquidity premium is currently below 2% (based on our estimates), and global liquidity remains abundant, yet distributions are delayed. This is not a lack of buyers but a timing/quality mismatch: buyers want contracted, high‑quality cash flows while many sellers seek faster liquidity. This suggests the headline illiquidity premium understates heterogeneity in liquidity across the market. |

Demand expressed yet capital withheld. Many surveyed allocators say they target larger private allocations but are pausing new commitments until DPI visibility improves. Stated intent exists; actual commitments lag. |

A cross‑market cap on confidence. PE’s recovery is constrained by the same ambivalence that holds back public markets. Despite short-term tailwinds, political and policy uncertainty in many DM countries combined with multiple longer term tail risks (public debt, inequalities, geopolitics, to name a few) limit conviction and slow PE recovery. |

These paradoxes point to a market reset – not a lasting pause – where headline liquidity and modest average discounts mask a wider tail. They favour managers who demonstrate realised outcomes, treat liquidity engineering as a durable toolkit rather than a cure, and build disciplined capacity to harvest opportunities while protecting downside against macro shocks. |

Improving outlook: fundamentals point to a gradual pickup

Our PE indicator – built from the pulse in business formation, SME revenue and profits, capex/M&A momentum, productivity changes, private valuation signals, corporate risk appetite, and tracking the real SME economic fabric, not public markets – is a leading cue for PE deal‑flow and performance.

It shows that PE is healing from the supply/exit clog while deal flow revives, but the process is gradual and vintage re‑rating takes time.

An improved playbook for value creation

The consolidation phase is changing how managers generate returns. With entry multiples relatively high and public/private convergence more limited, “buy cheap, sell at a higher multiple” is no longer the default path to IRR. Realised returns will instead come from growing the earnings base: operational improvements, pricing power, add-on acquisitions, and solutions to preserve downside while enhancing upside. Execution, liquidity engineering and deep sector knowledge – not multiple re-rating – will be the primary alpha sources. In other words, managers are much more hands‑on, favouring buy‑and‑build approaches. Consistent with this shift, PE activity is now dominated by smaller targeted transactions (add-ons, carve‑outs, trade sales) that outnumber large buyout or growth deals.

AI, in particular, now dominates in the VC/PE funnel (half of the incremental deal volume is AI‑linked) and produces both rich opportunities (huge markets, operational uplift) and risks (valuation, concentration, obsolescence, cannibalisation). AI investments will be a key test of managers’ selection and governance discipline in 2026.

Private debt: maturing, more selective

The market mood is ambivalent but constructive

Recent headline defaults focused attention on originator risk. These cases stemmed from leveraged‑loan‑style financings, aggressive structuring or accounting, and complex off‑balance sheet schemes – not classic private lending. That underscores a common market labelling issue: the term “private credit” is often used loosely, even when involving listed/syndicated structures. Our analysis shows most of these failures were idiosyncratic; the vast majority of private‑debt loans are senior, secured and floating‑rate.

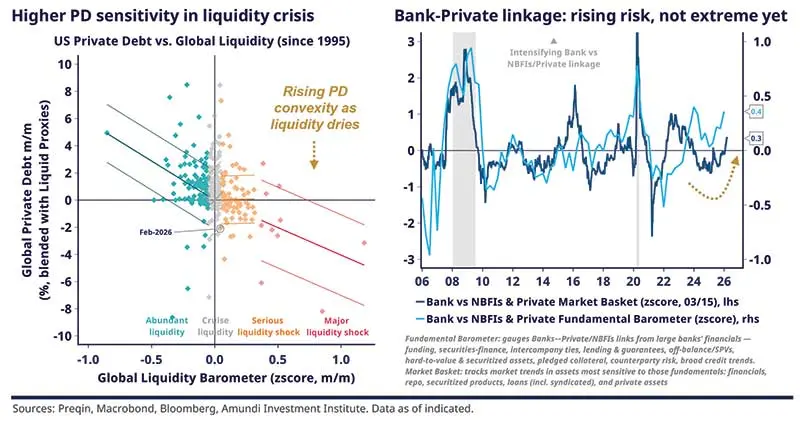

Recent redemption suspensions expose two core vulnerabilities. First, liquidity mismatch: managers couldn’t quickly sell illiquid assets to meet large redemptions, driven in part by a shift toward more liquidity‑sensitive clients. Second, valuation uncertainty: PD valuations depend on models with hard‑to‑estimate assumptions, borrower transparency is limited, investments are often complex – so marks are inherently uncertain and can lag in reflecting borrower deterioration. Those factors interact, especially when liquidity tightens: uncertain marks can trigger redemptions, which can force sales at lower prices. The left graph shows that PD’s sensitivity to liquidity grows more convex as liquidity dries up. Conditions are benign today, but as PD scales and broadens its client base, stronger liquidity controls, tighter valuation processes, and stricter underwriting are required.

Cross-exposures with banks. As privates expand, they increasingly overlap with banks, which provide funding and intermediation – bridge financing, margin lending, direct lending, partnerships. Scrutiny is rising because private failures could affect banks more sharply than before and propagate more broadly. We monitor this risk: our models flag it as material but not systemic yet, given privates’ relative size and the limited realised losses to date.

Large private rounds in AI/tech raise concentration and equity cushion risk if capex or margin promises don’t materialise. This is legitimate to watch, in our view, but not a reason to panic. Many AI firms successfully monetised early demand and show strong headline profitability, even though those profits are increasingly concentrated and don’t fully convert to cash – amplified by leverage, the capital structure, and/or optimistic capex conversion. PD managers will need more selectivity (recovery expectations, stronger covenants), but risk looks manageable at this stage. This theme tends to be more US-centric and not central in Europe.

Concern that PD will underdeliver as flows surge is understandable, but dry powder is not unusually high. The true test is underwriting discipline and workout capability, not flows alone. Performance will be manager specific: winners will combine strong origination, industrialised monitoring, tight documentation and credible recovery playbooks. We expect some performance erosion as the asset class scales, but we’re early in the PD expansion. Meanwhile, liquidity, securitisation and document progress will reduce risk, maintaining a sound risk/reward mix.

Although not our base case, a sharper downside is possible: if AI optimism falters materially and/or a prolonged Middle East energy shock produces stagflation and tighter credit, liquidity mismatches and valuation uncertainty could lead to widening PD marks and stress in refinancing channels.

Direct lending will continue to dominate

Direct lending will remain the backbone of private credit. Senior, secured, floating‑rate loans meet persistent borrower demand, replace bank capacity and deliver predictable, contract‑like cash flows attractive to large institutional buyers. In the US, compression of vanilla yields and more funding needs from AI/data, cloud, renewables, reshoring – which require large up‑front capex, long development windows and material execution or technology risk – are pushing specialist managers into higher‑return segments including: late-stage growth and venture debt, specialty finance (receivables, inventory, equipment), project and real asset lending, structured credit (private loan CLOs) and opportunistic/distressed credit. By contrast, European direct‑lending markets remain more focused on sponsor‑backed mid‑market financings, SME refinancing (often to enable consolidation or founder succession), and traditional corporate lending (the AI/cloud/reshoring narrative is far less prominent there).

A favourable alignment of macro planets

Relatively easing monetary conditions should relieve borrower cashflow strain and reduce refinancing stress, while floating rate exposure provides protection if rates surprise higher. PD will also benefit from a build-up in corporate activity and rising M&A.

Spreads have compressed but remain higher than most listed alternatives. Meanwhile, investors will continue to recognise much more cautious private credit risk management than in government debt. Selectivity will be critical, made easier as we expect credit markets to enter a more differentiating phase of the cycle, yet without major shocks.

Overall, with rising flows, returns will become more idiosyncratic and manager‑dependent: selection, underwriting rigour, covenant strength, sponsor quality and operational expertise will matter most. Private debt is graduating from yield hunting to credit craft: alpha will accrue to managers who can underwrite and monitor over those who merely deploy capital. This means favouring managers who prioritise disciplined deployment over AuM growth and demonstrate alignment (meaningful GP commit, co‑invest access, conservative incentive structures). In the next phase, skill and alignment will beat scale bought at the expense of discipline.

Infrastructure: at the crossroads of many opportunities

Brown assets face transition and regulatory risk

Old, high‑carbon assets (e.g. unabated gas or coal plants) face accelerating transition and regulatory risk. The most attractive near‑term opportunities are brown‑to‑green conversions and repowering (e.g. replacing plants’ old turbines or adding battery storage to solar parks). These upgrades are faster and cheaper than building greenfield from scratch, which involves long construction delays.

Greenfield projects need diversified revenue stacks

The best projects combine several income streams (e.g. a long‑term power contract + payments for grid services + capacity payments). Projects that rely on a single, volatile merchant price (e.g. selling power at spot market prices) are riskier for big institutional investors, amid still elevated rates and tighter construction markets.

Financing structure is decisive

Finance is a key differentiator. Deals including debt that adjusts with inflation, junior capital that absorbs first losses, and public or development‑bank support have a better chance to get done.

Political and regulatory uncertainty creates opportunities

Political and regulatory uncertainty makes deals harder to close and manage, which increases the value of GPs with deep local networks, permitting experience, and hands‑on asset management. Some large institutional investors are shifting from direct ownership to co‑investing or partnership models, seeking to share risk with experienced sponsors.

Inflation sensitivity improves nominal returns when revenues are protected

Assets with contractually indexed or contracted cash flows are increasingly valued for their inflation correlation, because lenders are willing to provide long‑dated, fixed‑rate financing against revenue streams that reprice with inflation. That cheaper, stable debt raises expected nominal returns and eases liquidity pressure for investors. By contrast, uncontracted merchant assets remain more rate and merchant price sensitive.

Digital infrastructure: a growth play whose risk depends on asset quality

Data centres, fibre, and cell towers are in steady demand because of AI, cloud computing and 5G. But not all projects are equal – location, power availability, and long‑term contracts with big customers are the factors that separate institutional assets from commodity plays. Lower‑quality projects are far more cyclical, exposed to rate, financing and liquidity shocks, and to AI/tech risks.

Execution frictions will remain the hidden return killer

Even well‑modelled projects can fail to deliver if contractors underperform, supply chains delay critical components, or permits get held up. Instead, contractor creditworthiness, solid contracts and insurance guarantees make the difference.

Real estate: green shoots of recovery but fragmented

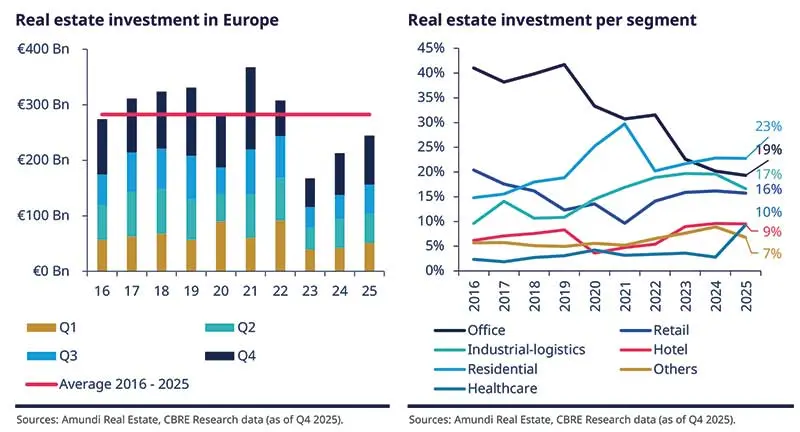

In Europe, a recovery in investments but a slow market

In 2022, the sudden end of the "lower for longer" period, a relatively long phase of low or even negative interest rates, led real estate market yields to adjust upwards to reflect the new higher‑rate environment. The resulting decline in real estate values allowed for some market rebalancing alongside heightened caution from investors.

Since then, the volumes invested in real estate in Europe have picked up, but market activity remains subdued. For example, nearly €245bn was invested in real estate during 2025 in Europe, the highest volume in three years. Nevertheless, activity remains c. 15% below the ten-year average and c. 33% below the 2021 peak. We believe that the repricing carried out in recent years supports a continued, albeit slow, investment recovery in 2026, especially as the ECB and the Fed may reduce their key interest rates.

Continued diversification of acquisitions

We expect investors will continue to diversify their portfolios across asset classes, as they have done for the last several years, with the aim of achieving a more balanced exposure and limiting idiosyncratic risk. Offices, for example, have been particularly affected in recent years.

Ongoing portfolio diversification in Europe can help limit volatility in portfolio performance, although it may forego sector-specific alpha. We think such diversification should not be done without keeping in mind the market depth of the various asset classes as well as the fundamentals of each asset.

Diversification can also help capture different underlying trends. For instance, hotels with international clientele can benefit from economic drivers that differ from those of the local economy, while healthcare can benefit from ageing demographics, which are expected to support demand for care and underpin the asset class.

Diversification also lets investors benefit from varying asset characteristics. Hotels and healthcare assets often feature longer leases, which can attract certain investors. Hotel investments offer several structures: holding only the real estate (leasing the asset) or participating in the business via a management contract. The latter provides greater exposure to the hotel's operating model and can foster potential value creation, although it may be more volatile.

Markets remain highly segmented

Investors will likely remain very selective in their asset picking in 2026, particularly regarding offices. These multi-speed investment markets are explained by the segmentation of leasing markets, favouring established and centrally located markets rather than peripherally located offices, some values of which have further declined in 2025 due to yield decompression, such as in the first ring of the Paris region, where there is oversupply. Early and limited signs of occupiers’ interest shifting towards the periphery, where rents are lower, as observed in the Paris region, will be worth monitoring in 2026.

More broadly, amid recent rises in office vacancy rates – averaging 9% across a sample of 28 European markets at the end of 2025 – and in the logistics sector, choices of micro‑location and assets remain critical. This is particularly the case given Amundi Investment Institute's expectation that GDP growth in the euro area will remain positive but slow in 2026. The Institute also expects disinflation, which could constrain the indexation of passing rents.

Particular attention to fundamentals in an uncertain environment

A continued stabilisation in eurozone prime yields, with some declines depending on the market, appears likely given Amundi Investment Institute’s current forecast for 10‑year government bonds in Europe, which are expected to be stable year on year by end-2026.

Because the gap with prime yields in some countries, such as France, is relatively small, market yield risk appears to be rising, especially in the event of a political crisis. Decreases in value may occur, especially for non‑prime locations with high vacancy rates. Overall, we believe that, on average, most of the repricing has already taken place.

We currently believe that the overall performance of real estate will be less driven by market yield compression than in the previous cycle, which reinforces the importance of rental income and market rent growth in overall performance. This feature may favour value‑added strategies if managers target double‑digit potential returns, but careful attention must be paid to leasing fundamentals. A focus on fundamentals and business plans is also key for assets whose cash flows are closely linked to operational management, such as healthcare and hotels.

Beyond tenant analysis, we believe particular attention should be paid to building characteristics, like their flexibility and capacity to meet today’s and likely tomorrow’s occupier needs. Assets with high land value or redevelopment potential and markets with strong leasing fundamentals (facilitating quick reletting) are likely to be at an advantage.

Furthermore, given the megatrend of climate change and increasing demands for building resilience, these considerations should be incorporated into capex plans and investment policies.

Key risks for private assets in 2026

In 2026, the largest tail risk doesn’t come from a single shock but from overlapping stresses – rising rates, tighter credit, liquidity mismatches, policy/regulatory shifts and geopolitical strain – whose intersection can amplify stresses and produce non‑linear outcomes.

| Interest‑rate and real‑yield risk: higher real yields compress valuations across PE/RE/Infra and raise refinancing costs for levered deals. |

| Competition for high-quality deals: pressure to distribute and demand for institutional-grade assets exceed immediate supply, eroding expected returns. |

| Tech/AI volatility risk: high valuations and concentration can trigger outsized repricing if capex conversion disappoints or if parts of the AI value chain are ruptured or cannibalised. |

| Liquidity mismatch, valuation uncertainty, and portfolio concentration: as retailisation and liquidity innovations expand, mismatches between fund liabilities and illiquid assets, private valuation uncertainty and concentrated positions can turn a localised stress into a portfolio‑level event. |

| Linkages with banks and other financial institutions: banks fund private markets and often concentrate exposures with a handful of large counterparties; insurers also frequently cede private risk to reinsurers or offshore SPVs that themselves hold private assets (often managed by the same sponsors). Private‑asset valuations are model‑based and infrequent, and funding chains are opaque. Consequently, private‑market stress can trigger a liquidity “cliff” – rapid margin and collateral calls, forced asset sales and non‑linear losses that cascade across banks, insurers, other non‑banks, and the securities‑finance plumbing. |

| Political and geopolitical risks: sanctions, trade restrictions, scrutiny of foreign direct investment, nationalisation or subsidy reversals can block deals or erase returns, especially cross‑border. Although not our base case, prolonged uncertainty in the Middle East could lead to a stagflationary energy shock, which could slow exit strategies, deteriorate public and private credit conditions, and put pressure on riskier infrastructure and real estate projects. |

| Regulation and tax: rule changes or reinterpretations (fund structures, SWF/treaty shifts, token/retail regimes) can change economics, force restructurings or make vehicles unusable. |

| Secondary market concentration risk: dry powder is concentrated in a small number of permanent-capital institutions with lower liquidity constraints (pension, insurance, family offices). Their dominance of top-tier secondaries may compress discounts (permanent sellers have time to wait for buyers, while permanent buyers can afford to buy low-discount assets), reduce transaction volumes, or push other players into lower-quality opportunities. |

Authors