Summary

The US earnings season reinforces our view of a broadening rally into real‑economy, signalling an ongoing — albeit non-linear — rotation towards these sectors.

The US technology sector is leading earnings growth for Q4 but markets are no longer giving a free pass to these businesses.

Secondly, earnings growth is broadening and is no longer concentrated in a small number of technology firms.

Although the reporting season was positive, market concerns persist about AI-distruption and the monetization of AI-investment.

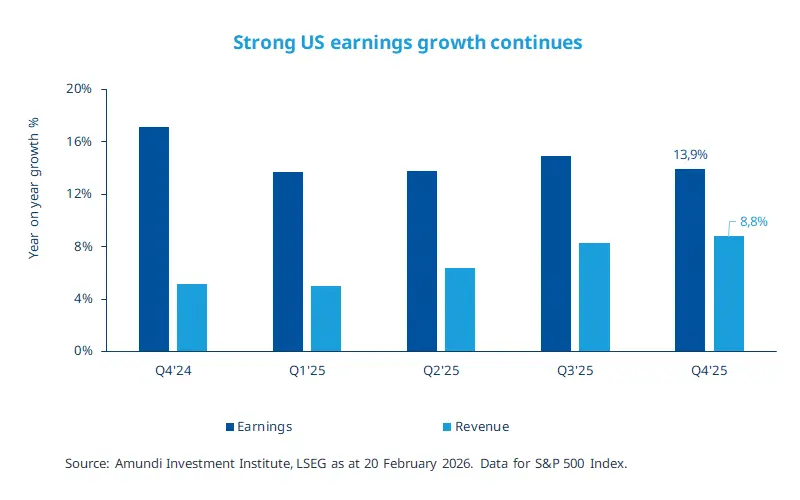

US equities saw another strong reporting season for the three months (Q4) ended 31 December 2025, with blended (actual earnings of companies that have reported results plus estimated earnings of those yet to report) earnings growth of about 14% year-on-year, as on 20 February 2026. While this earnings growth is slightly below what we saw in Q3, it is much higher than the estimate at the start of the reporting season (about 9%). Information technology is once again leading but there are continued signs of earnings broadening with strong results from the industrials, financials and communication services. In Europe, the reporting season has been relatively muted, with no growth at the index level. But more companies are yet to report earnings in Europe. Financials once again have had a strong quarter with meaningful upgrades, whereas the cyclical consumer sector continues to be a drag.

This week at a glance

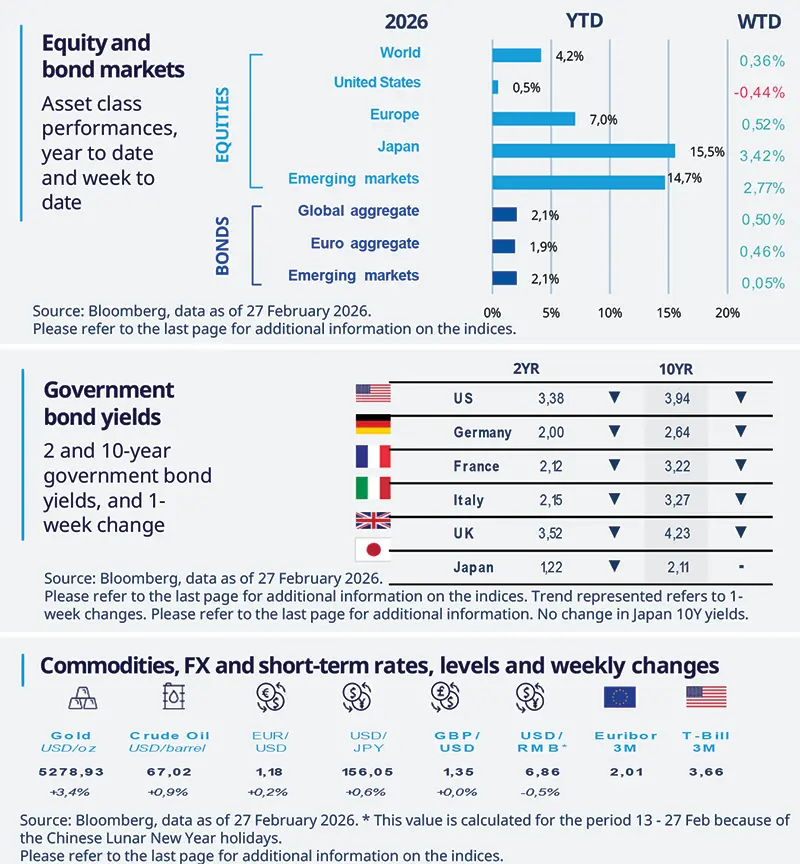

Global equities rose broadly, with markets favouring regions such as Japan, EM and Europe. Japan was buoyed by expectations of fiscal expansion and the nomination of two dovish members to the board of the Bank of Japan. Concerns about the sustainability of AI‑related spending weighed on US stocks. In fixed income, government bond yields eased slightly, while gold extended its gains.

Equity and bond markets (chart)

Source: Bloomberg. Markets are represented by the following indices: World Equities = MSCI AC World Index (USD) United States = S&P 500 (USD), Europe = Europe Stoxx 600 (EUR), Japan = TOPIX (YEN), Emerging Markets = MSCI Emerging (USD), Global Aggregate = Bloomberg Global Aggregate USD Euro Aggregate = Bloomberg Euro Aggregate (EUR), Emerging = JPM EMBI Global Diversified (USD).

All indices are calculated on spot prices and are gross of fees and taxation.

Government bond yields (table), Commodities, FX and short-term rates.

Source: Bloomberg, data as of 27 February 2026. The chart shows the price of gold.

Diversification does not guarantee a profit or protect against a loss.

Amundi Investment Institute Macro Focus

Americas

US CEOs upbeat on Capex, Hiring weakness persist

The CEO Confidence Indicator rose in Q4 to its strongest level since Q1 2025. The main driver was the capital spending plans indicator, which climbed to a four-year high, bolstered by tax reliefs. A large share of CEOs said they have passed, or intend to pass, costs on to customers, while a smaller share said they absorbed them. On the labour front, hiring plans remain low and skills shortage persists.

Europe

EU Sentiment Slips

The European Commission’s Sentiment Index fell in January but remained at a high level. The decline was driven by services and construction; industry dipped slightly and consumer confidence edged up from a low base. Employment expectations loosened but expectations of the selling price for services stayed high. The survey supports the ECB’s policy stance, though a weaker labour market may signal rate cuts later this year, in line with our expectations.

Asia

A slower monetary normalization in Japan

The Japanese government has nominated two dovish economists for the Bank of Japan’s Policy Board. The nominees, Toichiro Asada and Ayano Sato, have previously backed policies aimed to boost growth and reflation. Their appointments may reinforce a more accommodative monetary policy stance, signaling slower normalization under Prime Minister Takaichi and supporting our view of a June hike, while markets expect April.

Key dates

EZ PMI, Germany Retail Sales, Turkey GDP, US ISM Manufacturing |

China PMI, EZ PMI Services and Composite, US ISM Services |

EZ GPD, US Retail Sales and Non Farm Payrolls, South Korea CPI, Brazil Industrial Production |

Authors