Summary

The Amundi Investment Institute, in partnership with Crédit Agricole du Languedoc, the University of Montpellier, and Montpellier Business School (MBS), has forged a unique collaboration dedicated to advancing our understanding of individual investors’ financial preferences and needs. This partnership combines academic rigor with practical insights from the financial industry, creating a rich foundation for exploring the evolving landscape of retail investment behavior.

Our approach is multi-faceted and comprehensive. It includes conducting regular, large-scale surveys to capture retail investors’ appetite and attitudes toward various investment strategies; performing quantitative analyses to uncover patterns in consumption and savings behavior; and implementing innovative online experiments to test the effectiveness of different incentives aimed at developing investment participation. A particular emphasis is placed on responsible investment behavior, reflecting the growing importance of sustainable finance in individual decision-making.

These research initiatives are conducted in close collaboration with the CSR and responsible investment, sales and marketing teams at Crédit Agricole Languedoc and Amundi. This integrated effort ensures that our findings are not only academically robust but also directly relevant and actionable for financial institutions seeking to better serve their clients.

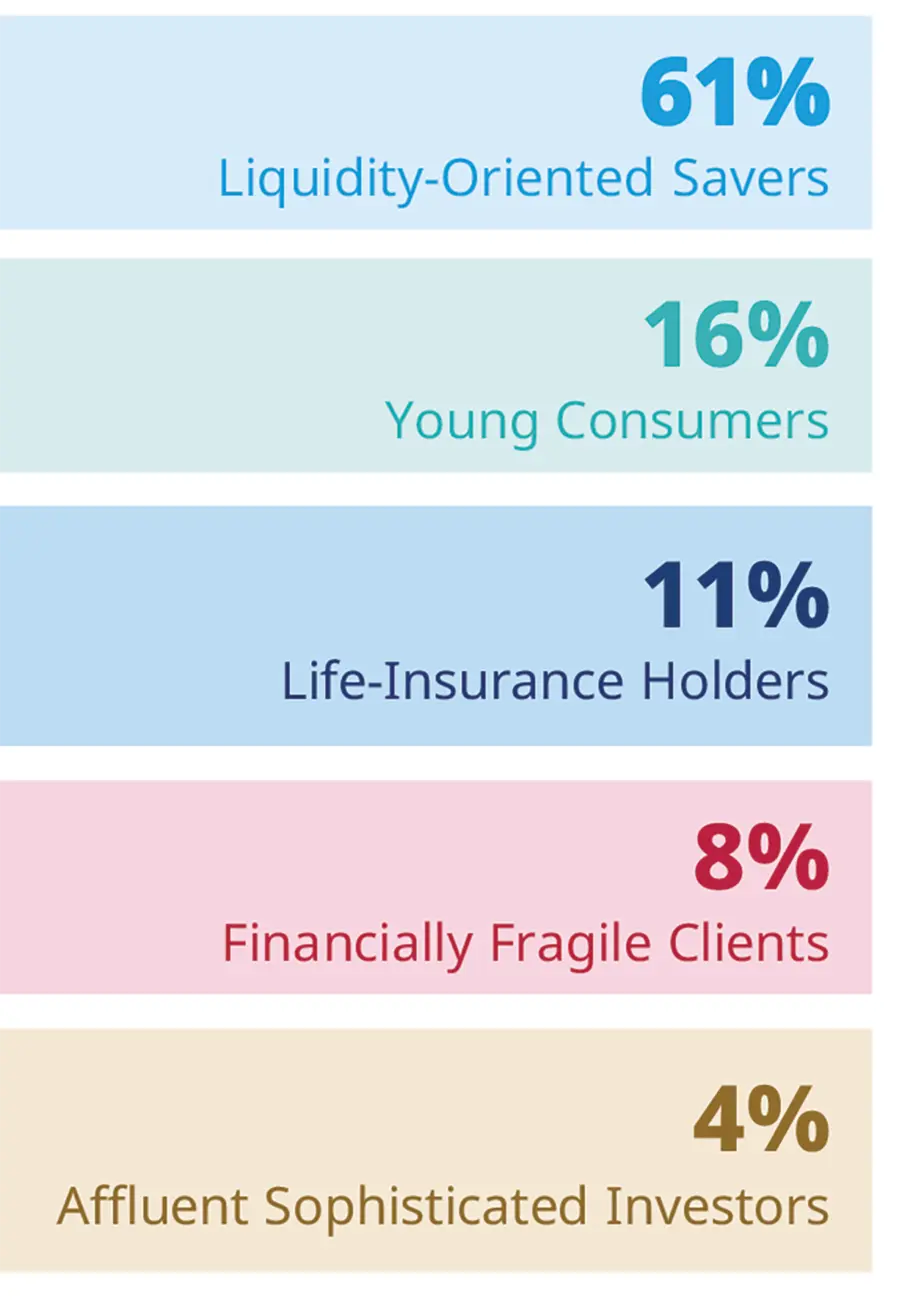

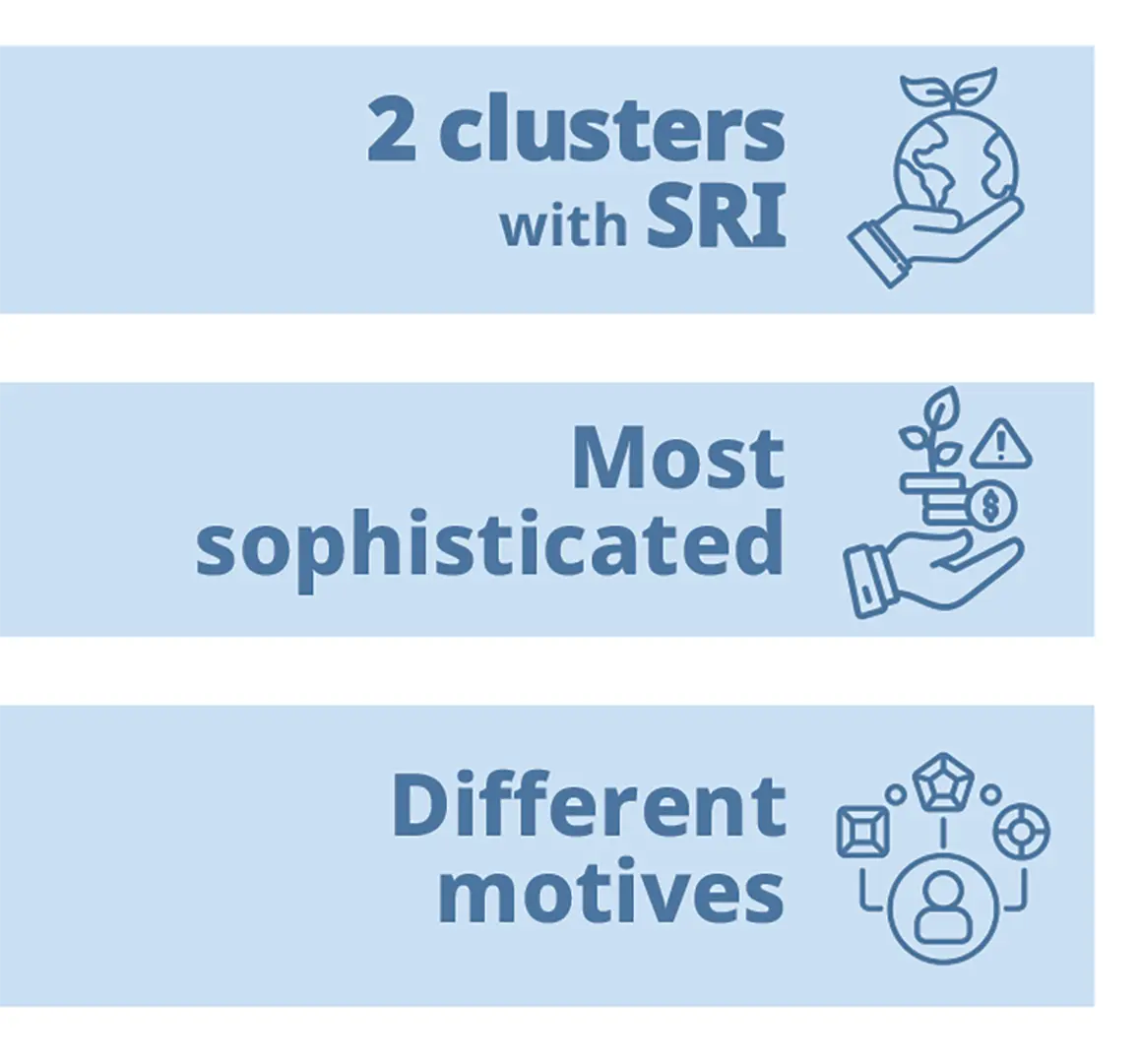

We are pleased to share the second chapter of this ongoing research endeavor. Using granular administrative data matched with survey responses, we cluster retail investors to uncover both observed and unobserved dimensions of their financial behavior, including financial sophistication, expectations, risk and socially responsible preferences. We identify five distinct investor segments that differ markedly in demographics, consumption patterns, and investment choices: affluent sophisticated investors, life-insurance holders, liquidity-oriented savers, young consumers, and financially fragile clients. Only the first two clusters allocate a significant share of their investment portfolio to socially responsible investment (SRI) funds, though their motivations differ: affluent sophisticated investors combine financial and impact considerations, while life-insurance holders are more impact-driven.

Overall, the results highlight substantial heterogeneity among retail investors and suggest that more differentiated product offerings and tailored communication strategies could better meet the needs of each segment. We aim to support financial institutions in better tailoring their advisory services and product offerings to meet evolving client demands in a rapidly changing market.

Abstract

Using a randomly selected sample of 50,000 clients of Crédit Agricole Languedoc, we identify 12,902 investors and analyze their financial behavior using granular administrative data.

The dataset covers several dimensions, including demographic characteristics (age and gender), consumption patterns based on bank card transactions, financial activity such as account inflows, loans, savings and financial wealth, and detailed investment holdings in CTO, PEA, PERI, and life-insurance portfolios. Together, these data provide a comprehensive view of clients’ financial situation, saving behavior, and portfolio allocation.

In addition, 1,080 clients from the sample participated in an online survey on investment practices. The survey complements the administrative data by capturing information that is typically unobservable in banking records, including risk tolerance, social and sustainability preferences, expectations about financial markets, and beliefs about socially responsible investment (SRI). It also provides insights into investors’ financial sophistication, portfolio management approaches, sources of financial advice, and motivations for engaging in SRI.

By combining detailed administrative records with survey responses, the analysis provides a richer understanding of retail investor behavior and the heterogeneity of investment practices across clients. In particular, we identified five clusters of retail clients—Affluent Sophisticated Investors (4%), Life-Insurance Holders (11%), Liquidity-Oriented Savers (61%), Young Consumers (16%), and Financially Fragile Clients (8%)—that are distinct in their demographic characteristics, financial sophistication, expectations, and consumption and investment behaviors.

Survey highlights

|

|

We identify five clusters that are different in their demographic characteristics, consumption and investment behaviors:

|

|

|

|

Conclusion

In a clustering analysis of French retail banking clients, we identified five clusters of savers: affluent sophisticated investors, life insurance holders, liquidity-oriented savers, young consumers, and financially fragile clients. Due to their distinct characteristics and behaviors, aligning product offerings and communication strategies with each cluster strengthens client engagement and improves the relevance of investment solutions across saver segments. A differentiated approach—ranging from advanced strategies for experienced investors to accessible and educational solutions for less engaged clients—can help foster broader participation in investing while supporting investors’ diverse financial goals and preferences, including responsible investment.

Download the full report

Author