We don’t expect a 2022-style inflation shock, but we recognise that 2026 is no longer a normal inflation environment. In this regime, bonds may be less reliable as an equity hedge and portfolio construction needs broader inflation protection: selective risk assets, carry over duration, real and private assets, commodities and gold.

With the last major inflation shock in 2022, H1 2026 has provided another example of renewed inflationary pressure, this time driven by an energy supply shock stemming from the conflict in Iran. These episodes confirm our long-term view that inflation is becoming more structural and less linear, driven by geopolitical fragmentation, stronger commodity demand linked to the green transition, AI and infrastructure and repeated supply-side disruptions. While 2022 was an extreme event, with inflation fuelled by a powerful mix of pandemic-era stimulus, supply chain bottlenecks and energy prices, 2026 is not an extreme inflation shock, but it still marks a meaningful shift compared to our original assumption of a normal inflationary backdrop.

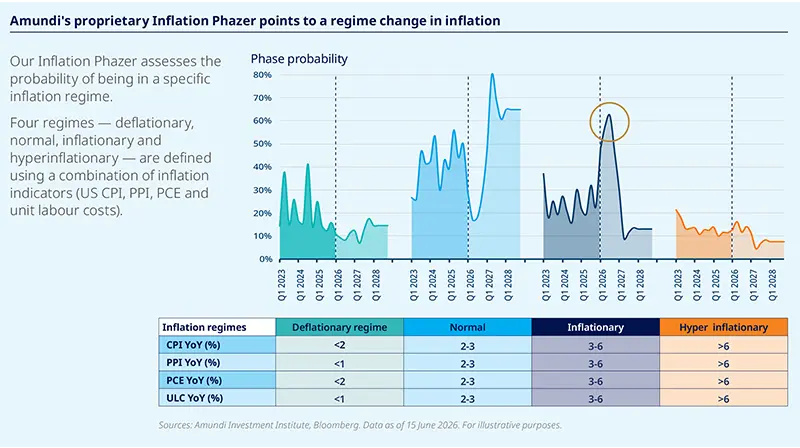

Our proprietary model, Inflation Phazer, now points to an inflationary regime, with US CPI above 3% as the most likely backdrop for the remainder of the year. A return to a normal regime phase is more likely from Q2 2027 as the spike in energy prices fades. This does not mean a repeat of the 2022 shock, but it signals that inflation is likely to remain high and persistent enough to shape central bank reaction functions, market behaviour and portfolio diversification.

The investment implications are significant: monetary policy is likely to remain less dovish/turn more hawkish, while rate volatility should stay elevated and term premium may evolve in a less linear way across bond markets.

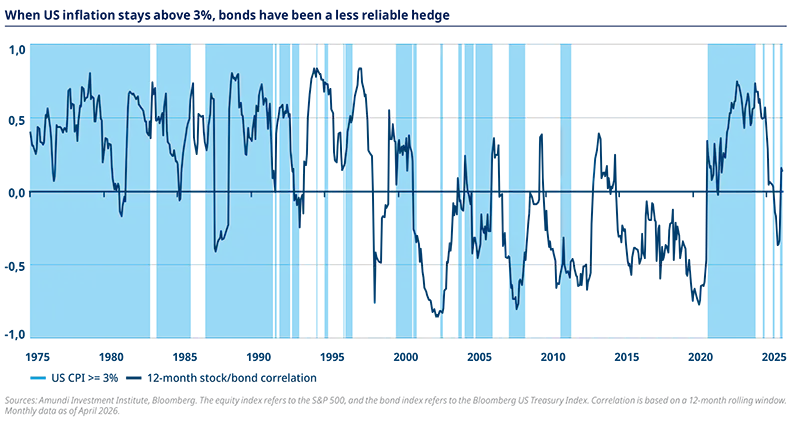

As a result, the duration component of a traditional balanced portfolio may prove less effective as a diversifier, particularly because bonds may not necessarily remain negatively correlated with risk assets during inflation-driven market stress (see figure above). Inflationary shocks push yields higher at a time when risk assets come under pressure, turning the bondequity correlation positive and supporting the case for broader diversification beyond duration.

At the same time, continued shortages of certain commodities and minerals, together with structural demand for AI and infrastructure development should support selected real assets and inflationsensitive exposure. A more difficult monetary policy backdrop, alongside high public debt trajectories and central banks’ diversification away from dollar-based assets should continue to support demand for gold and precious metals at a solid pace.

In H2 2026, if the global economy remains resilient in an inflationary environment, then it calls for maintaining exposure to risk assets with stronger hedges. In equities, the most inflation-resilient areas are in industrials, infrastructure, and companies with strong pricing power. In fixed income, carry appears preferable to duration. We also believe that gold and commodities more broadly will play a more reliable role in portfolio diversification to enhance resilience.

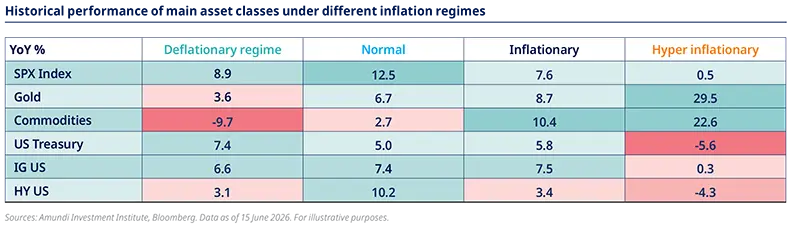

Inflationary regime matters: asset class performance changes materially when the regime moves from normal to inflationary and cash becomes a structural decision. Gold and commodities have historically offered stronger relative performance, while the role of bonds depends on the source and persistence of inflation.

With contributions from Laura Fiorot,

Head of Investment Insights & Client

Divisions, Amundi Investment Institute

Authors