Summary

Asia’s diverse populations face a common challenge; how to tackle the continent’s retirement question. Longer life expectancies and demographic shifts raise concerns about the financial sustainability of Asia’s pension systems and what measures can be taken to address the coverage gap. It is against this backdrop that Amundi carried out research into pension provision in five Asian markets.

Our research, conducted in partnership with consultancy Crisil Coalition Greenwich and based on interviews with participants4 of the personal pension ecosystem in Singapore, Hong Kong, Taiwan, Thailand, and Malaysia, paints a retirement landscape that is evolving rapidly against a backdrop of growing wealth and higher living standards. Rapidly ageing populations and low birthrates across the region further accentuate the real or perceived inadequacies of state and workplace pension systems of even robust pension system such as Singapore’s. This will likely fuel the development of personal pensions as well as of post-retirement asset management solutions.

Currently the asset base for personal, pillar 3, pensions, is small at US$40 bn. However rising awareness about pension inadequacy and structural gaps with respect to post-retirement asset and income management suggest retirement assets both in and out of pension accounts is likely to grow significantly going forward. The actual rate of growth in each market will ultimately depend on local factors including available workplace schemes and contribution caps.

Coverage inadequacy

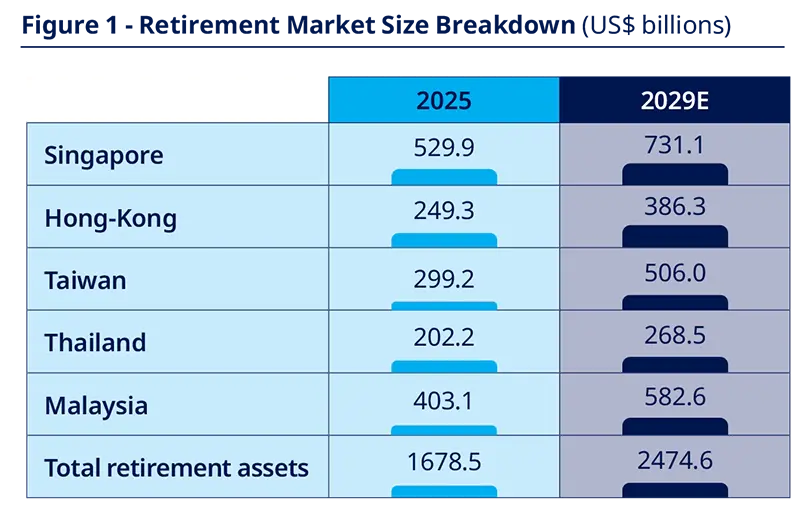

According to our tally, regional retirement assets across state (1st pillar), workplace (2nd pillar) and personal (3rd pillar) pensions continued their long-term growth in 2025 with an annual increase of 9% to reach US$1.7 trillion. These retirement assets could reach US$2.5 trillion by 2029 on the back of the ongoing rise in household wealth, pension reforms and rising awareness about the importance of retirement saving and planning.

Mandatory workplace retirement schemes remain the backbone in most countries, accounting for 90% of the retirement assets in the region. Yet, this sizeable asset base—held in investment & insurance products, as well as in guaranteed deposits with an outsized proportion located in tiny, high-income Singapore (see box 1)—hardly translate into high income replacement across the region. Replacement rate percentages are in the low forties for all markets in the region, except for Singapore whose 60% replacement rate aligns with the OECD average.

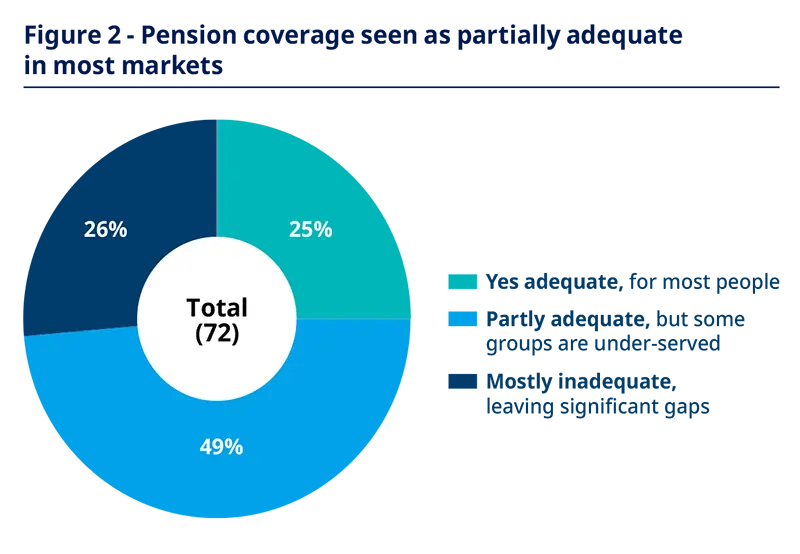

This gap in replacement rates helps explain why Singapore is the only market where pension coverage is viewed by market participants as being mostly adequate5. In all other markets, including Hong Kong with the broad coverage offered by the Mandatory Provident Fund (MPF, US$200 billion), most local interviewees consider pension coverage to be either only partly adequate or mostly inadequate3. Interviewees reported structural pension gaps as well as significant shortfalls for middle income, self-employed, and mass-affluent segments.

Filling the gap

For now, assets held in personal pension accounts6 are not sufficient to fill this the adequacy gap—but this could change. At the end of 2025, personal pension assets amounted to no more than US$40 bn. Growth in this segment has varied across markets, reflecting differences in tax incentives, financial literacy, and product availability. Singapore and Hong Kong show relatively strong growth, supported by established savings incentives and higher levels of financial awareness. Taiwan and Malaysia also report positive momentum as policies are introduced to encourage personal retirement savings.

Assuming growth in line with the overall retirement markets, personal pension plan assets could reach over US$60 billion by 2029. However, interviews with market participants suggest that such a like-for-like growth estimate may significantly understate the current and future size of personal pensions in the region as workers 1) seek solutions to convert their accumulated retirement assets into post-retirement income, often outside pension accounts; and 2) increase their retirement-related investments at a faster growth rate than their overall savings.

First, limiting the definition of personal pension assets to those held through official personal pension schemes is probably restrictive, particularly in Asia, where multi-asset income funds generate much enthusiasm and can be used as a decumulation management tool, especially in jurisdictions that allow for the distribution of capital. Enlarging the definition of personal pension assets to assets that can be used throughout the retirement journey, and using multi-asset income funds as a proxy, adds as much as US$ 95 billion to existing personal pensions assets. This highlights a sizeable and evolving asset base beyond government-led personal pension structures, even assuming that only part of these investments is earmarked for retirement management purposes.

Second, survey respondents across markets generally expect overall retirement allocations to increase over one to three years from the current modest allocation of financial assets to retirement savings, estimated at <20% in most markets. Most respondents anticipate a modest increase rather than a significant shift, suggesting a gradual strengthening in focus on retirement planning. Markets such as Taiwan and Malaysia show relatively stronger expectations for increased allocations, reflecting growing awareness of retirement income challenges and demographic pressures. By contrast, some markets expect allocations to remain broadly stable, indicating that structural factors such as highly institutionalised pension systems (Singapore, Hong Kong) or competing financial priorities may limit near-term changes.

Personal pension adoption

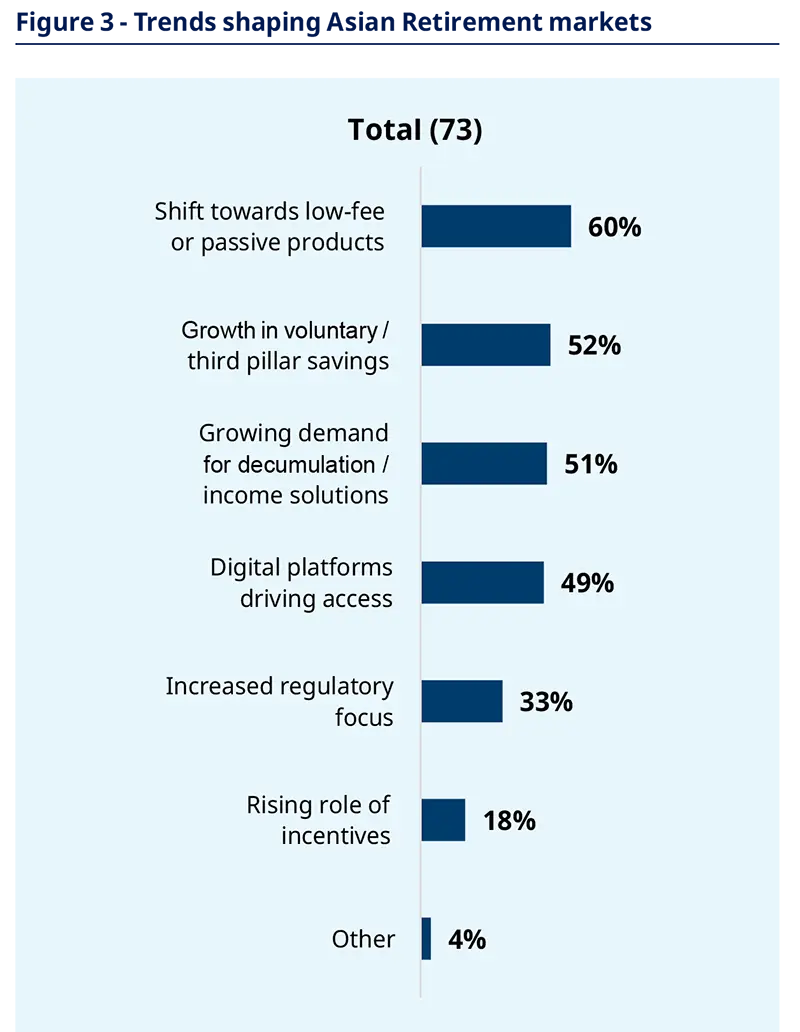

Most of this rising retirement tide will be absorbed by workers maxing out their workplace or mandatory contribution cap. Nonetheless, the results of our survey suggest that a meaningful share will likely flow into personal pension schemes, which could grow at an even faster rate from a relatively low base. In this regard,

market participants across the region identify the growth in third pillar savings (52%, with the highest rate in Taiwan, Malaysia, and Thailand – Figure 3), as a key structural trend shaping retirement markets in the region going forward, just after the incorporation of low fees or passive products into retirement solutions (60%).

The main reasons for such flows will vary by market, but may include self-employed workers who may not have access to a workplace pension, individuals wanting to save beyond their workplace scheme contribution limits, or those wishing to diversify their investments away from the options available in their workplace scheme into more flexible or enticing investment solutions offered by personal pension schemes.

Personal pension products may also include solutions aimed at addressing gaps in income adequacy. These can help workers manage pension balances that tend to be communicated in total asset terms rather than as a clear projection of future retirement income, leaving individuals fundamentally uncertain about their true ability to sustain the level of spending they will need throughout retirement.

This challenge is particularly acute in Asia, where early withdrawals, housing needs, and longevity risk increase uncertainty on postretirement income. An ability to dynamically process data from various sources and easily generate personalised investment plans, as used by digitally enabled distributors, could play a central role in helping investors develop an overall view of their retirement-related savings and accessing decumulation options.

For personal retirement savings, digital banks appear to possess a structural advantage. They benefit from controlling high-frequency customer touchpoints, behavioural data, and engagement triggers, and their platforms can encourage engagement through contribution nudges, default pathways, and planning tools that can be embedded seamlessly into everyday financial activity. Where effectively designed, these capabilities can support more consistent and sustained retirement saving behaviour than traditional, episodic advisory interactions. This type of digital engagement is a model that could also be adopted by workplace pension schemes to improve engagement in workplace pensions.

Lifecycle risk management is another potential driver of growth in personal pensions, especially as many existing Asian pension systems still rely on relatively static asset allocation approaches. These completely lack the sophisticated, dynamic sequencing of risk required as individuals transition from the wealth accumulation phase into the decumulation phase. Singapore’s recent decision to deploy a lifecycle investment option in its second pillar CPF7 schemes is an approach we may see popularised throughout the regions’ pension systems.

4. 73 interviews with industry participants including insurers, banks, asset managers and wealth managers, with most respondents holding senior management, investment or product leadership roles.

5. Answer given to the question “In your view, is the pension coverage in your country sufficient?” An adequate pension coverage corresponds to the delivery of the income needed to maintain a satisfactory living throughout retirement for the population at large.

6. Personal pension accounts included in the analysis include investment accounts with specific retirement-related tax treatment ad defined by each government, as well as some accounts designed for longterm, outcome-specific investing (i.e. which would fall under the World Bank’s definition of the “4th pillar” of a retirement system). This includes Malaysia’s PRS, Singapore’s SRS, Thailand’s Retail Mutual Funds, Hong Kong’s Public Annuity Scheme, as well as Taiwan’s ISA (not tax-advantaged).

7. Central Provident Fund, the mandatory social security savings scheme in Singapore

With contributions from Ken Yap,

Head of Investment Management

APAC ex. Japan, Crisil Coalition Greenwich

Authors