Summary

- Emmanuel Macron won French presidential elections: In Sunday's second-round runoff, Macron defeated far-right National Front leader Marine Le Pen by 58.5% to 41.5%, confirming his leader in the most recent polls. However, the outcome in the second round was much narrower than in 2017 and the abstention rate was put at 28%, the highest in 50 years.

- French and European Union implications: The challenge for Macron over the next five years is to strengthen the French economy and its competitiveness, based on its better position than for other Eurozone countries, due to the low dependence on Russian gas, as well as deal with significant dissatisfaction with the political class. In this regard, the need to maintain a parliamentary majority in the legislative elections planned for June will be crucial for implementing his economic policy. On the European front, the re-election of the French president reinforces his vision of a sovereign Europe, with more unified EU foreign and defence policies plus further energy independence going forward.

- Investment implications: Although Macron’s win had been somewhat anticipated by the markets, the election outcome has removed a key risk. For fixed income, the reduction of political uncertainty could tighten OAT bond yields by around 10 bps vs. Bund. The re-election is also positive for the EURUSD exchange rate, as well as for French equities, which offer a compelling valuation on relative value.

What are the key takeaways from the second round of French presidential elections?

Emmanuel Macron won the presidential election with a strong lead (58.5%), a much better result than the latest polls predicted at the end of last week. However, the low turnout (72%), the lowest level since 1969, puts this victory into perspective.

Above all, this victory is a great success for Europe and a guarantee of stability for the Eurozone. Macron made it clear that this election was a referendum on Europe. European integration will continue: the president will seek to strengthen the Franco-German relationship and more generally European institutions. In this regard, Macron intends to respect tradition by quickly visiting Berlin to meet with German Chancellor Olaf Scholz. The absence of a change of course should also reassure all NATO countries regarding France's foreign policy.

The president-elect must now obtain a majority in parliament during the parliamentary elections on 12 and 19 June. Whether a majority emerges will ultimately determine economic policy and the reform agenda.

What has been the market’s reaction?

Although there was some short position building on French debt and the CAC40 in early April, after the first round of the elections, markets were already pricing in a Macron victory. Last week, French equities outperformed the rest of Europe and bonds did as well to some extent, with the OAT-Bund spread tightening. Therefore, investors were clearly unhedged against the risk of Le Pen becoming president and it is unlikely that we will see big moves on the back of Sunday’s result. Moreover, the second round turned out to be battle between pro- or anti-EU sentiment. The election outcome thus strengthens Eurozone prospects, with more integration likely going forward.

However, we will now see a second step in the French political cycle with the lower house (Assemblée Nationale) two-round local elections. These will either lead to a majority for the re-elected president or result in a coalition situation. Many outcomes, including no majority for Macron’s party, or a strong result for the far left (Jean-Luc Mélenchon) or far right (Le Pen), could be sources of a renewed uncertainty.

Yet over the short term, markets will be more impacted by the ongoing situation in Ukraine, with the risk of a prolonged high-intensity conflict, and deterioration in the pandemic in China. Both could threaten the global economic cycle.

Macron’s victory is a guarantee of stability for the Eurozone and European integration will continue.

How might this result impact the upcoming Parliamentary elections in June, and what could be the consequences for governability and French reforms?

Macron announced shift in focus between the two rounds, promising to consult more on the major orientations of his policy (pensions, education, health). The constitution of his next government will also send a strong signal that will foreshadow a possible enlargement of the presidential majority to other political sensitivities (republicans, greens or even social democrats). A re-ordering of the French political landscape is under way. Macron will probably seek to form a coalition. In order to do so, candidates of different sensibilities will probably be presented under the banner of the presidential majority during the parliamentary elections.

We believe that the institutional logic will continue to prevail. In the past, the elected president has always obtained a majority in parliament. It should be borne in mind that the electoral base of the parliamentary elections is in fact very different from that of the presidential elections: the turnout is always lower, especially for the parties that lost the presidential elections, which should ultimately benefit Macron’s party.

However, we point to several issues:

- Macron won by a much lower percentage than in 2017 (66.1%).

- The far right won almost a third of votes in the first round, which is unprecedented in the history of the Fifth Republic.

- The growing fragmentation of the political landscape is therefore an increasingly difficult challenge. For many voters, this election was above all a rejection of the extreme right, not a vote of support for re-elected president’s programme.

Thus, contrary to the logic of the Fifth Republic and the logic of the voting system, voters can use the "third round" (i.e. parliamentary elections) to balance their sometimes "constrained" choice in the second round.

- It should be remembered that the winning parties (in the first round) are not those that have deep roots in areas and hold mandates at the local level. Given the structure of the voting system, it is very likely that the "anti-system parties" (Mélenchon on the far left, and Le Pen and Éric Zemmour on the far right), although representing a majority of voters, will find themselves with very little representation in the lower house, which could fuel anger and resentment.

- The president has a very limited time to absorb the remnants of the traditional parties at the local level through a coalition.

- A hung parliament could result, with significant social risks that could limit the ability to carry out reforms.

However, this risk seems to us to be rather low for the reasons mentioned above.

What are the first expected reforms?

On the substance, Emmanuel Macron has defined several priority areas (purchasing power, health, education). At the very top of the list is the fight for purchasing power, which was the dominant theme of the election. Macron promised to pass an exceptional law this summer that would force companies whose profits allow it to pay an "employee dividend" either via profit-sharing or via the payment of a “purchasing power bonus”. The idea is simple: to ensure that employees benefit more from phases of economic recovery in the same way as shareholders do. An increase in public sector wages is also expected as well as a rise in the minimum full rate pension to €1,100/month (compared to €980 currently).

On the issue of pensions, Macron will favour consultation: the project now consists of pushing back the retirement age by four months per year to reach age 64 in 2027-2028, and possibly 65 by 2031.

In short, the "new method" put forward by Macron is more participatory, with the declared will to implement a more inclusive economic policy and to accelerate the energy transition.

Upcoming elections could result in a hung parliament, limiting the ability to carry out reforms.

What could the impact be on European common matters: strategic autonomy, energy independence, military expenditure?

Emmanuel Macron’s pro-European manifesto clearly showed support for more European integration and an enhanced European autonomy in an evolving geopolitical context. Macron wants to “ensure the power of Europe” with a focus on energy, technology and defence.

As is the case since it took over the rotating presidency of the EU, France wants to ensure energy self-sufficiency by accelerating decarbonisation and deployment of clean energy to reduce dependence on imported coal, gas and oil. This situation has become an emergency for several European countries, which rely heavily on Russian gas and oil imports.

Europe’s technological autonomy was mentioned often by Macron during his campaign. He calls for more investments to support European champions and more protection in the most strategic areas. France will push for the development of critical technology infrastructure, such as a European "cloud" and a constellation of satellites.

Since his Sorbonne speech in 2017, the French president has called for European strategic sovereignty. A first step is to ensure strategic autonomy through the definition of a common doctrine, and a significant strengthening of the capabilities of European armies and their coordination. An alignment of EU countries’ defence budgets to 2% of GDP would significantly increase total European military spending (from €40bn to €60bn per year).

Macron wants to ‘ensure the power of Europe’ with a focus on energy, technology and defence.

Do you see any impact on the key structural reforms at a European level?

In addition to the topics mentioned earlier (energy, technology, defence), there are several key reforms Europe needs to implement which President Macron highlighted as priorities, including new fiscal rules, a renewed common energy market, and a new governance of the EU.

Fiscal rules as they are defined today (3% deficit, 60% debt/GDP and 1/20th rule, which requires that 1/20th of “excess debt” be eliminated per year convergence) look unachievable for several countries, including France. Moreover, complying with these rules could lead to a prolonged recession and probably deflation. Lastly, they do not fit with the specificities of individual country fundamentals (or even groups of countries). Therefore, they need to be amended to secure stability for the monetary union and the credibility of European institutions. France’s newly re-elected president will certainly push for such reforms.

The common energy market has shown its limits, with tensions in the electricity market in Q4 2021 post Covid-19 and now due to the war in Ukraine. The market mechanism, which was designed to ensure price competition and stability, is falling short of its second objective. As they don’t incentivise public investment and national energy strategies, the energy market rules look unsuited for the massive and long-term investments required by the energy transition. While Germany is suffering from its past decision on nuclear and its dependency on Russian gas, France has an important role to play in this area.

Lastly, European institutions will have to evolve if the 27 members want to welcome Ukraine as well as countries of ex-Yugoslavia. With the Eurozone at its core, the European Union probably needs to reform its decision-making process (veto, composition of the EC) to avoid gridlocks and political stalemate. Tensions with Hungary and Poland are good examples in that context. President Macron is calling for a reform of Schengen with new rules and means to protect European borders. These are challenging topics, which require a new treaty from the EU that a French president freed from further electoral objectives (he cannot run for a third term) could contribute to solving.

Macron has highlighted some European top priorities, including new fiscal rules, a renewed common energy market, and a new governance structure for the EU.

On the fixed income side, how do you see the demand for French OATs evolving and where are opportunities for investors?

As already slightly anticipated by the markets, the OAT has begun a retracement vs the Bund from 55bp on the 10Y to 45bp on Friday evening, correcting about two-thirds of the widening which occurred in anticipation of the election result. The reduction of political uncertainty should help the spread to return to the 40bp region, which is likely to attract Asia investors, notably Japanese ones, after several months of limited exposure to OATs in favor of USTs (10Y OAT 1Y FX hedged into JPY offer a good pick-up vs JGBs and USTs). OATs should also benefit from redemptions and coupon payments on Monday, 25 April (around €42bn regarding two bonds maturities).

On the negative side, we are unlikely to see bigger compressions as the end of APP will lead to lower liquidity in the system and the outcome of parliamentary elections is not clear yet, given the next rounds occur on 12 and 19 June and Macron’s party lacks local anchorage as opposed to more traditional parties.

The reduction of political uncertainty should help the spread between the OAT vs the Bund to return to the 40bp region.

What are the opportunities and risks of investing in French equities?

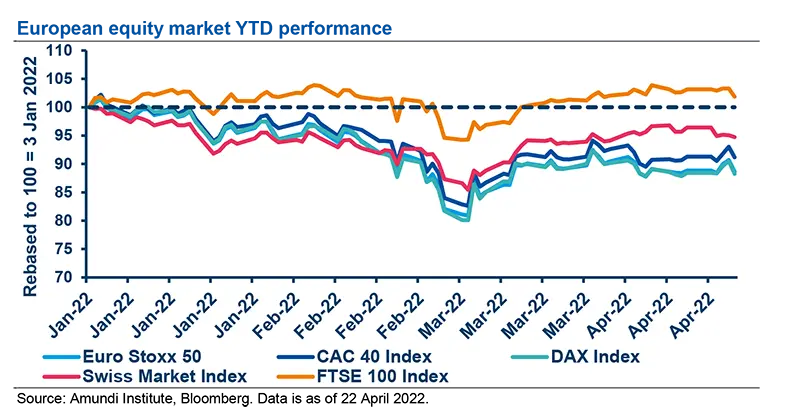

French equities (CAC 40) are more cyclical than other European markets, such as Switzerland (SMI) or the UK (FTSE 100). Opportunities relate to valuation and the heavier representation of companies with strong pricing power, such as the luxury sector. The risks relate to the economic slowdown, whether regarding the energy crisis or monetary tightening. We also see upside risks, as France is one of the few European countries that instituted reforms over the past four years. Secondly, the CAC 40 index is well balanced in terms of weights between banks, cyclicals and services. Only around 15% of the activity of CAC 40 companies occurs in France. Furthermore, there has been a decent flow of lending data and a definite improvement in services. There is room for sentiment to improve given the discrepancy between consumer expectations and economic strength. France does not have the huge income gap seen among other economies and it has a much better energy mix than its European peers such as Germany and Italy.

How could the election of Macron impact the French stock market?

The re-election of Emmanuel Macron will mean the status quo will remain, removing a tail risk, even though there is a sense of division in the country that may hinder the reform agenda, along with growing fears on the level of the French debt, which will limit the capacity to act. French large-cap stocks have outperformed the rest of Europe in the five years of Macron's first presidency and could thus regain some of their losses after the re-election. However, global drivers are likely to prevail over domestic ones – in particular, exposure to China and to the Russia-Ukraine war. The more domestic-oriented small caps could benefit from hope of further structural reforms and higher investment which would boost competitiveness. Macron’s second term should be positive for the relative performance of French equities and the EUR/USD. Investors could play the French cycle through financials, infrastructure and industrial sectors.

Macron’s second term should be positive for the relative performance of French equities and the EUR/USD. Valuation for French equities remains attractive.

What can French equities bring to a global equity portfolio, with a particular focus on ESG?

France’s CAC 40 emissions data are dominated by fossil fuels, manufacturing and material production. The 2021 index temperature scores show that France was aligned with a 2.7°C temperature increase, a better result than Canada (+3.1°C), the UK (+3.1°C), Japan, as well as the United States (+3.0°C). France is on par with Italy while Germany is doing marginally better (+2.2°C). The French index shows the lowest rate of companies without climate targets, a good start for companies to outperform in this regard. Aside from this general remark, French equities offer undisputed exposure to the energy transition, with a rich panel of companies positively active in the construction sector, including building and electric material producers. Despite some negatives, the luxury sector generally performs better in ESG rankings than mainstream retail companies. The French index also offers a fair exposure to hydrogen mobility. Combining enhanced transparency and lower carbon emissions, French companies are well perceived by the traditional ESG rating agencies used by many investors. French companies enjoy enhanced transparency, as since Grenelle II (2010)1 , French ESG disclosure obligations have been more stringent than those of other EU member states.

For instance, French companies are required to have their non-financial reporting audited by a third party, which is not the case currently at the EU level under the Non-Financial Reporting Directive (NFRD). Consequently, French companies are usually more transparent than their EU counterparts. This is valued by traditional ESG rating agencies, as their methodologies have significant ‘transparency bias’. With regard to reducing carbon emissions, due to the role of nuclear energy in the French energy mix, French companies with a significant share of their operations in France – and more broadly French companies overall – have lower Scope 2 emissions than their German counterparts, for instance, which rely on coal and natural gas as sources of electricity generation. Considering the weight of climate- and energy-related metrics in the methodologies of traditional ESG rating agencies, French companies are likely to be attractive from an ESG perspective.

Global investors should look at French companies as an ESG opportunity

Definitions

- Basis points: One basis point is a unit of measure equal to one one-hundredth of one percentage point (0.01%).

- Cyclical vs. defensive sectors: Cyclical companies are companies whose profit and stock prices are highly correlated with economic fluctuations. Defensive stocks are less correlated to economic cycles. Cyclicals sectors are consumer discretionary, financial, real estate, industrials, information technology, and materials, while defensive sectors are consumer staples, energy, healthcare, telecommunications services, and utilities.

- Quantitative easing (QE): QE is a monetary policy instrument used by central banks to stimulate the economy by buying financial assets from commercial banks and other financial institutions.

- Spread: The difference between two prices or interest rates.

______________________

1 "Grenelle II" is the French law (adopted in July 2010) that sets objectives on sustainable development, complementing a law passed previously known as "Grenelle I".

Authors