Summary

Central Bank Watch

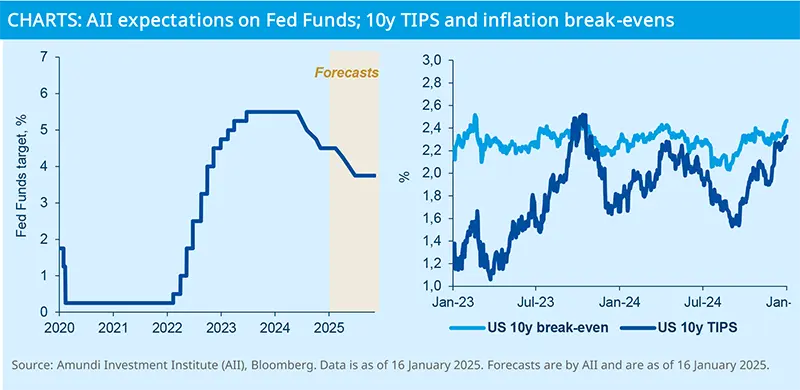

The Fed’s dilemma

Recent inflation numbers are in line with a short pause in the path towards the Fed’s target, yet bond yields have moved sharply higher since the Fed’s big cut. Medium-term inflation expectations – including FOMC member expectations – have moved higher (see chart), but most of the increase in ten-year yields since the election reflects a rise in real rates.

The Fed expects inflation about 30bp higher at the end of 2025 (at 2.5%), which implicitly incorporates some changes in policy under Trump, especially tariffs and fiscal easing. Market pricing is volatile and sensitive to monthly inflation outcomes. We expect three cuts to take the policy rate to 3.75% by the end of this year, as we believe the US economy will slow towards potential growth just below 2%, with higher real rates and tariffs weighing on growth.

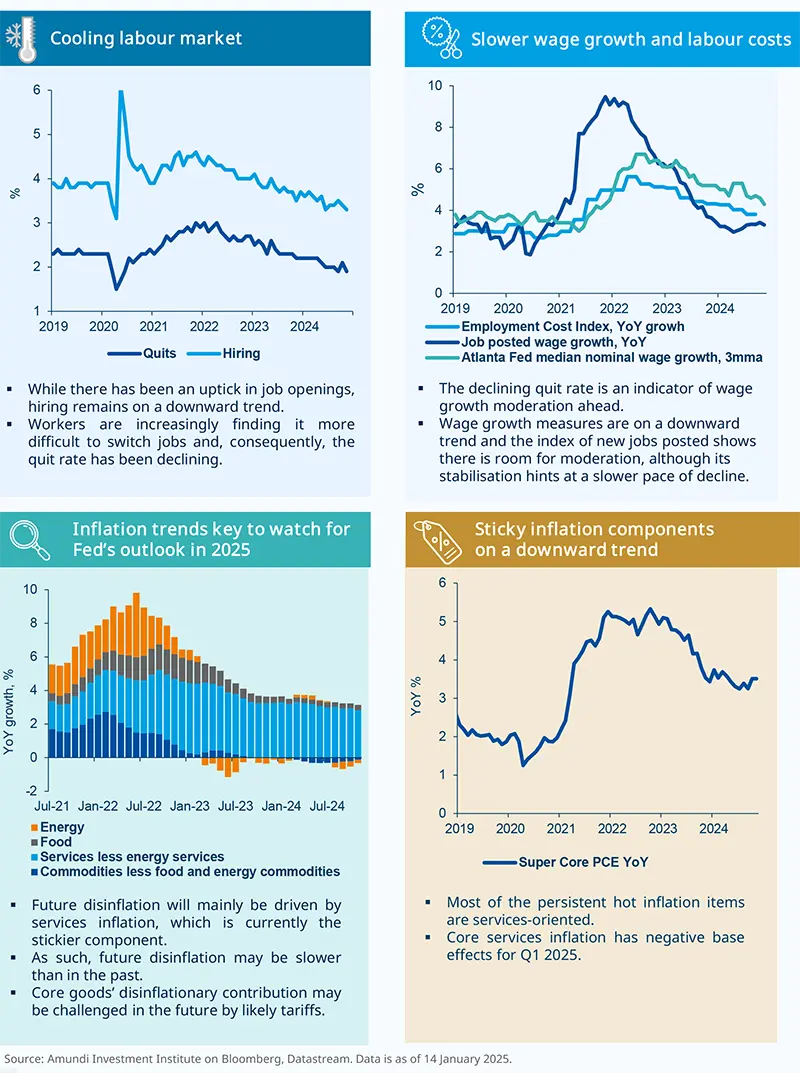

The US labour market is gradually rebalancing and wage growth does not pose a risk to inflation. Labour demand has been weakening, with fewer openings, lower quit rates, and an increase in temporary jobs. Labour cost indicators – hours worked, wages of new hires – are also moderating. And aggregate wage growth of 4 percent supported by productivity growth.

Higher real bond yields, will be a key headwind to growth and asset prices. The fiscal deficit – expected to be 6% of GDP this year – and associated debt issuance is the more likely reason for higher real rates, and higher term premia – the additional compensation investors require both for holding more debt and for higher inflation uncertainty. Breakeven inflation rates have moved marginally higher (inflation swaps indicate similarly). But real rates and term premia have moved more, with the latter at 10-year highs. This is more worrying.

We expect three 25bp cuts by the end of this year, taking the policy rate to 3.75%.

A slower US disinflationary process moving ahead

Main and alternative scenarios

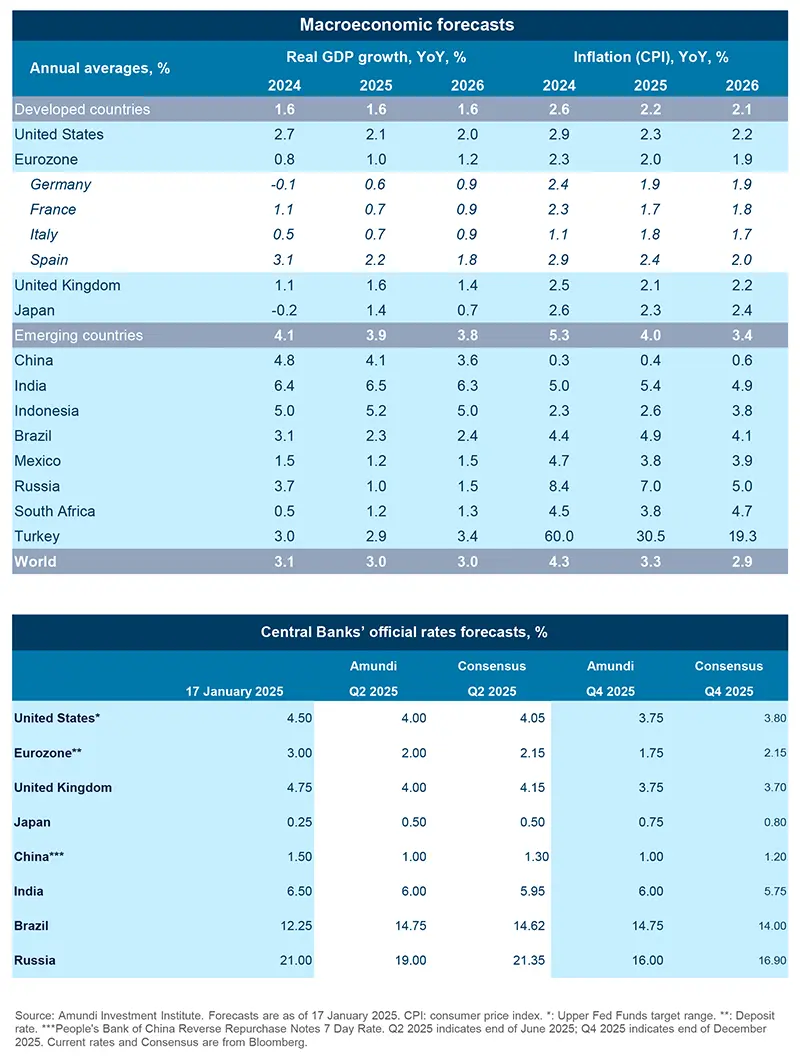

Macroeconomic forecasts

Authors