Summary

A relief rally, excess optimism overdone

Markets have seen some relief in a year that overall is likely to be remembered as among the most challenging for investors. But the negative trend reverted somewhat with gains for the S&P 500 and select Treasury Indices. This recent market move has been supported by an alignment of stars on various fronts: (1) US inflation on a downward path, wherein we believe the market rally and the exuberance is excessive, as the Fed will remain focused on the inflation target and it is too early to claim victory there; (2) the earnings season was bad but not as bad as feared; (3) China’s Covid policy relaxation, which has happened earlier than expected, but full reopening will be in 2024; and (4) geopolitical uncertainty, with regard to which there has been some pause after elections – in the US, the mid-terms saw no major surprises and were quickly digested by the market, which reacted well to a divided government that should deter populist policies. Internationally, we can expect more on the US/China tensions front. In the UK, the new PM is changing the fiscal policy stance, with the focus now on tax increases and spending cuts.

These developments lead us to keep an overall cautious view entering 2023, but to tactically play some short-term opportunities within an overall well-diversified approach. In detail:

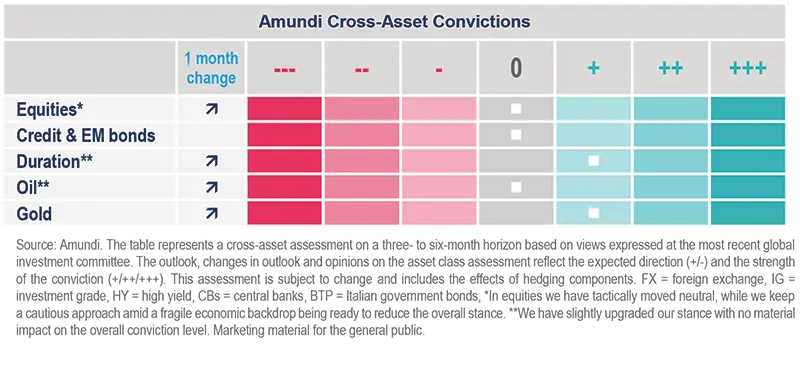

- From a cross-asset perspective, we have in recent weeks moved towards neutrality in equities. In particular, we have reduced our negative stance in European equities while remaining overall cautious with hedges in place. We have balanced this move by increasing sources of diversification, adding a positive view on oil and gold, and slightly increasing our duration stance on US Treasuries (UST). We remain ready to adjust this stance, as we recognise that the economic outlook is highly uncertain.

- The “bonds are back” theme was supported by the soft inflation reading that led to one of the strongest one-day rallies in Treasury history. However, an active duration stance remains key. Markets are interpreting any indication of lower-than-expected price rises turning into a potential dovish stance by the Fed, which, instead, is likely to wait for inflation to come in below expectations for some time before pivoting. Thus, we remain very active on duration, with currently a positive view through USTs and a keen eye on inflation and growth numbers. US inflation also reverberated in European core yields, where we maintain a close to neutral view, looking out for opportunities across curves.

- The “bonds are back” theme is playing out also in the credit market, with the focus staying on quality. Credit spreads have tightened since mid-October in the US and more so in Europe. However, we remain cautious on risky, low-quality debt of companies, which show a tendency to increase leverage. While corporate defaults are stable at this stage and strong company fundamentals are creating an improvement in credit ratings, it is important to note that ratings and defaults lag economic cycles. Thus, we do not see any convincing reasons to increase risks. Already, corporate cash levels, though still robust, are falling, and this is especially the case for low-rated issuers that would have difficulty raising capital during times when they need it most. Hence, companies’ refinancing needs, their capacity to meet capital needs internally, and CB stances are crucial factors to watch before we alter our stance. At a regional level, though, we continue to prefer the US to Europe.

- Our stance on EM LC debt remains a bit cautious, but we see value in HC debt of select countries. We think the opportunity to increase risks in EM debt hasn’t come yet, as the Fed’s dovish pivot – a key factor for the EM debt outlook – still looks elusive. Having said that, early 2023 could provide some entry points. Regarding China, we expect a gradual reopening in 2023, and the pace will impact growth. In Latin America, we are cautiously optimistic on Brazil, which has been a strong performer in EM this year. But, we are closely following how Lula’s policies affect the country’s financial position.

- In equities, we are tactically trying to capture opportunities while keeping a focus on bottom-up selection. We see the current move as a bear market rally. To assess it as a cyclical bottom for equities, we would need to see improvement in earnings and a Fed dovish tilt, but we are not there yet. In our view, US earnings expectations for next year are still high, given the dual effect of a growth slowdown and the still-strengthening dollar. In Europe, the situation is equally tricky, as some positive signs are emerging, but we need to see some progress on corporate margins and consumption before we are convinced that we are out of the woods. As a result, we stay vigilant in Europe and the US as we explore opportunities in value, quality, dividends, and the small-cap space, particularly in the US. Chinese stocks are highly volatile currently, relying heavily on news flow on zero-Covid policies and economic reopening despite attractive valuations. So, we keep a neutral stance and stay ready to re-enter when earnings fundamentals and economic growth are easier to evaluate.

Big picture in short

US inflation: decelerating but way above Fed comfort levels

|

Monica DEFEND |

Annalisa USARDI, CFA |

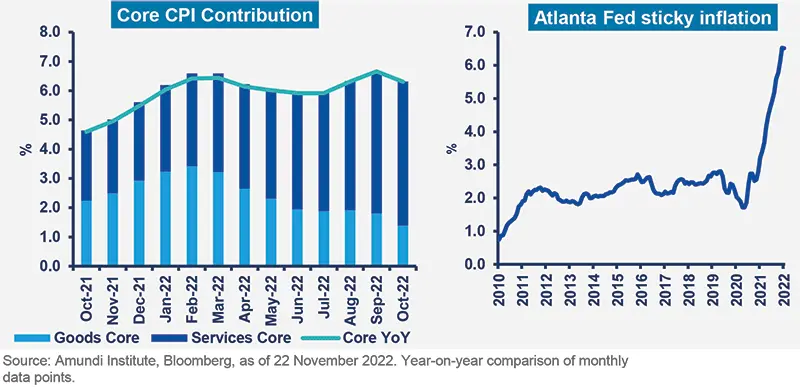

The US inflation outlook remains the key driver of market sentiment at this stage. A weaker-than-expected US CPI reading in October, up 7.7% from the previous year (the smallest year-over-year reading since February 2022), seemed to confirm that the peak is likely behind us and prompted a strong market reaction. The market saw this as a possible trigger for an anticipated dovish Fed pivot, which remains the main requisite to get out of the bear market. But in our view, we are not there yet.

On a month-on-month basis, headline CPI was in line with our expectations (0.44% vs forecasts of 0.48%). However, core inflation was weaker than our expectations (0.3% vs our forecasts of 0.49%). The miss in core inflation came from:

- Core services: the weaker than expected increase in core services was related to a significant drop in medical care services inflation, but monthly changes in other components did not show significant declines. The deceleration was in particular due to a one-off drop in costs of medical care services, which related to health insurance costs and may not be repeated.

- Core goods: the stronger than expected decline in core goods was driven by apparel, household furnishing and supplies and drop in used car prices. Core goods momentum is decelerating and proceeding in the right direction but there is still some progress to be made to get back to the pre-covid trends. Here, it is important to watch the dynamics of change in apparel and used car prices.

What does it mean for the inflation outlook?

Over the next few months, we expect firm core inflation momentum, while headline inflation momentum should be weakening due to the drop in gasoline prices.

- Headline: we confirm that headline inflation has now peaked in the US and going ahead, under our main scenario for commodities and oil, there should be a visible deceleration in year over year figures (e.g. Q4 2022 expected at 7.6%).

- Core: core inflation declines may be slower than headline (core is stickier), given that the services inflation momentum, even though slowing, remains quite elevated.

- Risks: we will continue to monitor the drag coming from core goods, which started to materialise in a faster than expected way in some categories, leading to a broad-based softening of core goods momentum and inflation.

How would the Fed respond?

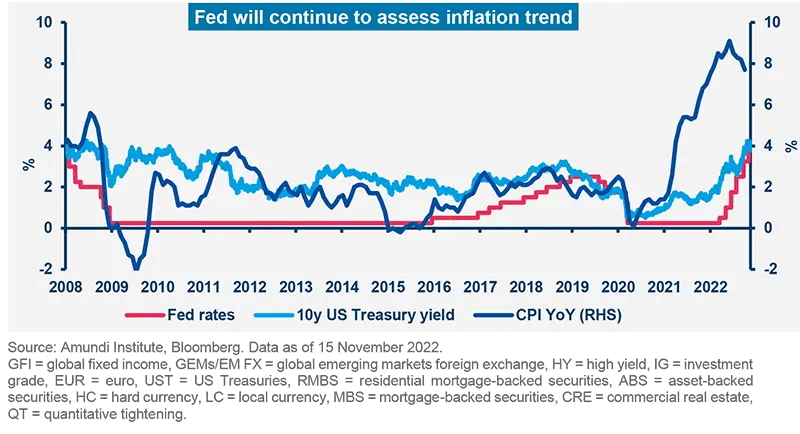

We think there is upward pressure on the terminal rates, given the robust labour markets and the Fed’s resolve to fight inflation. The Fed sees better risk/reward in overtightening its monetary policy so that inflation comes under control now, and then if required later, the central bank may look to support economic activity through the numerous tools at its disposal.

Importantly, the Fed is reactive to the inflation data and is not trying to build a narrative after its last “transitory inflation” view didn’t quite hold well. Instead, it is now focussing on how high to increase interest rates and how long to keep them in the restrictive territory.

What are the investment implications?

Persistent inflation, even though on a decelerating path, underscores the need to maintain a diversified stance that goes beyond the traditional equity/bond asset classes, to include real assets and commodities among others. This would enable investors to focus on inflation adjusted returns, and at the same time, include portfolio protection through gold, USTs. However, given that pressure on yields are prevailing on both sides (slowing growth and high inflation), it is crucial to maintain an active stance overall.

Although US inflation numbers are decelerating, the Fed is likely to maintain its "higher for longer stance" with respect to monetary policy.

Stay well-diversified, explore relative value

|

Francesco SANDRINI |

John O'TOOLE |

Profit recession, tightening central banks (with divergences in forward guidance), and still-high inflation are primary market concerns. US inflation moderating has been a positive lately, but whether that deceleration will be sustained would decide the Fed’s stance, which in turn is a key parameter for us to become constructive on risk assets. For the time being, China’s Covid-related news flow, geopolitical tensions, and earnings fears don’t allow us to alter our cautious conviction. However, we do see some tactical opportunities in equities, mainly via relative value. This approach must be complemented by better diversification and portfolio protection through commodities (oil) and gold on both of which we are constructive for the purpose of enhancing real returns and hedging.

High conviction ideas

On equities, we tactically moved our stance to neutral by becoming less cautious on Europe and exploring relative value in the US, favouring small caps over expensive growth stocks. But we remain vigilant to adjust this view on the cautious side amid the evolving earnings backdrop. The discounts for small caps over large caps are at extreme levels and their relative performances are starting to improve. However, Europe faces higher stagflationary risks, enabling us to keep our preference for the US over Europe, where we are still defensive. In EM, we are neutral on Chinese equities, with a possibility of improvement in outlook in 2023. In fixed income, we asserted our constructive stance on US duration. With markets now pricing in a higher terminal rate and the Fed’s aggressive tightening path increasing the risk of a US hard landing, UST valuations look attractive. The Fed may slow the hiking path to evaluate the effects of the tightening done so far. However, we are monitoring this stance actively to safeguard from yield movements against our expectations. Overall, we look across geographies, including the UK, where we are assessing opportunities arising from the latest budget announcement.

On peripherals, we adjusted our stance on the Italian curve amid the ECB’s dovish guidance. We maintain a slightly positive view on 10Y BTP-Bund spreads, supported by the new Italian govern-ment’s assurance that it will continue on the path of fiscal discipline.

We maintain our marginally optimistic view on US IG. Corporate fundamentals and balance sheets are strong, with high liquidity and good interest coverage, and a low risk of debt refinancing in the near term. Also, we continue to believe EU IG should outperform HY. The latter would be more vulnerable amid a recession, especially in low-quality segments if default rates (under control for now) tick higher. The dollar remains the mainstay of our DM FX strategy, but we are now seeing some vulnerabilities in the USD risk/reward balance. Hence, while staying positive on the greenback, we think investors should diversify towards the JPY and the CHF, but stay cautious on the EUR. We are now defensive on the GBP vs the USD and CHF, due to a weakening UK economy. On the other hand, we maintain our USD/EUR and NOK/CAD stances as cyclical economies and their respective FX should remain under pressure in the near term. In EM, we are no longer positive on the IDR/CNH, as ambiguity around reopening from lockdowns in China could create volatility. In LatAm, we keep our constructive view on the BRL vs the USD. Markets have priced in a lot of uncertainty over Brazil’s new government at a time when the country should benefit from its improving macro-economic picture.

Risks and hedging

Hedging and diversification are key pillars of our cross asset strategy. We are now positive on oil, owing to supply side issues and a potential EU ban on Russian crude. In addition, gold could offer robust portfolio protection, given its safe-haven qualities and as a hedge against inflation. Separately, investors should maintain protection on HY and US equities.

With limited forward visibility, we remain well diversified and confirmed our positive duration stance, along with some tactical adjustments.

Play the “bonds are back” theme with quality

|

Amaury D'ORSAY |

Yerlan SYZDYKOV Global Head of Emerging Markets |

Kenneth J. TAUBES CIO of US Investment Management |

The Fed’s policy stance will centre on concrete signs of inflation moderating, rather than a one-off indication of inflation cooling down. This requires a tightening trajectory (even if the Fed decided to go slow on rate hikes) and increases the risks of recession heading into next year. Hence, forward guidance from the Fed and ECB is becoming increasingly important for inflation expectations and risk assets. On the last issue, if rates stay in restrictive territory, and the economic situation deteriorates, we could see spread volatility, notwithstanding the recent tightening. Thus, investors should refrain from increasing risks and play opportunities in resilient segments in US IG and EM HC through careful bottom-up selection. Regarding this, we are monitoring liquidity and the default outlook across credit markets.

Global and European fixed income

We reduced our slightly cautious stance on duration, where we hold defensive positions in Europe, the UK and Japan. However, given that the ECB is taking a ‘meeting-by-meeting’ approach, we stay flexible in adjusting this and look for opportunities across curves. Chinese debt continues to offer diversification advantages. On breakevens, although we are positive on the US and Europe, we reduced this stance marginally in the US. Credit spreads tightened recently, but investors should stay neutral/marginally posi-tive because spread volatility may increase if monetary policy and earnings turn unfavourable. This is particularly true for companies with excessive leverage. We continue to prefer high quality (IG), short maturity credits that have strong liquidity buffers. We like the auto sector but are monitoring how rising rates could affect the real estate sector.

US fixed income

While recent market movements indicate exuberance after inflation data and Fed statements, we think even if the Fed slows its rate hikes, this does not mean loosening of monetary policy or financial conditions. On the other hand, the consumption environment is becoming weak, as seen from consumer surveys and credit card delinquencies. Thus, we keep our duration stance neutral/slightly constructive under an active approach and a positive bias to upgrade if UST yields rise. Investors should not ignore liquidity and refinancing risks in corporate credit. Thus, we recommend maintaining a stable risk exposure, with a preference for higher-quality IG credit over HY. Within IG, we like financials over non-financials, given relative spread valuations and supportive regulatory capital levels. Securitised markets are backed by still good consumer earnings, but we are selective because volatility remains high and liquidity is low. We put special emphasis on collateral to help minimise our risks in MBS.

EM bonds

We stay slightly defensive on duration but are mindful of a potential stabilisation in US rates. We favour HC bonds, as their spreads offer good carry, but in LC, we are highly selective amid regional inflation divergences. At a country level, Indonesia and Brazil (declining inflation trend) appear attractive. We are also constructive on oil-exporting countries.

FX

Our strategic views favouring the dollar and caution on the EUR and GBP remain unchanged. However, we see opportunities in BRL to play any improvement in risk-on sentiment or a potential change in the USD trend. In addition, we are positive on MXN and CLP but cautious on EUR.

We believe instead of a one-off deceleration in inflation, the Fed is likely to assess inflation trend, labour markets and overall consumption environment before altering its course of action.

A high dispersion backdrop can offer opportunities

|

Kasper ELMGREEN |

Yerlan SYZDYKOV Global Head of Emerging Markets |

Kenneth J. TAUBES |

Overall assessment

Rising rates and decelerating growth are creating pressure on corporate earnings. The bulk of Q3 earnings have been released, with earnings generally showing some resilience, but the picture for 2023 doesn’t look rosy. We expect the downward trend in forecasts to continue and this is already priced into many companies’ valuations, but dispersion is high, favouring stock pickers. Separately, supply constraints, which earlier created shortages, are now manifesting on the consumer front. For instance, in the UK, higher energy prices are affecting discretionary spending. Hence, we are prioritising fundamental analysis, with a preference for value, quality, and dividend-oriented businesses.

European equities

We maintain our balanced approach with defensive consumer staples, on the one hand, and quality cyclicals on the other. We continue to focus on companies with resilient balance sheets, pricing power and ability to generate free cash flows. Ability to weather the deteriorating economic situation and inflationary headwinds will be key. There are opportunities across defensives as well as cyclicals with this in focus. We like retail banks, as unlike some other cyclicals, their net interest margins and earnings will benefit from higher rates. In addition, at current prices, their implied expectations are very low. In contrast, we are relatively cautious on utilities, given the regulatory risk, and the technology sector as valuations are excessive, given the current macroeconomic backdrop. Overall, we remain vigilant in our search for stock specific opportunities across all sectors.

US equities

We are witnessing some cracks emerging in the markets and discrepancies in valuations across sectors, as equal weight indices are outperforming the top-heavy S&P 500. In addition, 2023 earnings guidance is still not weak enough and is inconsistent with our view of a growth slowdown. All this collectively creates an interesting backdrop for stock selection. In particular, we are watchful on expensive unprofitable growth names, but are positive on quality value companies that have corrected and retain the potential to deliver earnings growth. This is complemented with a valuations-driven approach that allows us to be cautious on expensive defensive, staples, utilities, real estate and large cap names. We are also defensive on mega cap names. On the other hand, prices of select beaten-down quality cyclical businesses are turning attractive. At a sector level, we like banks, health care and select consumer names. Banks are showing strong potential for returns, but we remain bottom-up and believe credit risk is an important differentiator in this segment.

EM equities

EM valuations are compelling and earnings expectations are improving, but we stay selective in a fragmented world. Our main convictions at country levels are Brazil (upgrade) and the UAE. In Asia, the Chinese economy should rebound after the re-calibration of the zero-Covid policy and more clarity is needed on this. For the time being, we stay neutral and flexible. At a sector level, we prefer discretionary and real estate, but are cautious on healthcare and China financials.

A shift down the market cap spectrum, might unearth companies where valuations and potential returns are attractive, but we stay very selective.

Amundi asset class views

Definitions & Abbreviations

-

ADR: A security that represents shares of non-US companies that are held by a US depositary bank outside the US. They allow US investors to invest in non-US companies and give non-US companies access to US financial markets.

-

Agency mortgage-backed security: Agency MBS are created by one of three agencies: Government National Mortgage Association, Federal National Mortgage and Federal Home Loan Mortgage Corp. Securities issued by any of these three agencies are referred to as agency MBS.

-

Curve flattening: A flattening yield curve may be a result of long-term interest rates falling more than short-term interest rates or short-term rates increasing more than long-term rates.

-

Curve steepening: A steepening yield curve may be a result of long-term interest rates rising more than short-term interest rates or short-term rates dropping more than long-term rates.

-

Beta: Beta is a risk measure related to market volatility, with 1 being equal to market volatility and less than 1 being less volatile than the market.

-

Breakeven inflation: The difference between the nominal yield on a fixed-rate investment and the real yield on an inflation-linked investment of similar maturity and credit quality.

-

Carry: Carry is the return of holding a bond to maturity by earning yield versus holding cash.

-

Core + is synonymous with ‘growth and income’ in the stock market and is associated with a low-to-moderate risk profile. Core + property owners typically have the ability to increase cash flows through light property improvements, management efficiencies or by increasing the quality of the tenants. Similar to core properties, these properties tend to be of high quality and well occupied.

-

Core strategy is synonymous with ‘income’ in the stock market. Core property investors are conservative investors looking to generate stable income with very low risk. Core properties require very little hand-holding by their owners and are typically acquired and held as an alternative to bonds.

-

Correlation: The degree of association between two or more variables; in finance, it is the degree to which assets or asset class prices have moved in relation to each other. Correlation is expressed by a correlation coefficient that ranges from -1 (always move in opposite direction) through 0 (absolutely independent) to 1 (always move in the same direction).

-

Credit spread: The differential between the yield on a credit bond and the Treasury yield. The option-adjusted spread is a measure of the spread adjusted to take into consideration the possible embedded options.

-

Currency abbreviations: USD – US dollar, BRL – Brazilian real, JPY – Japanese yen, GBP – British pound sterling, EUR – Euro, CAD – Canadian dollar, SEK – Swedish krona, NOK – Norwegian krone, CHF – Swiss Franc, NZD – New Zealand dollar, AUD – Australian dollar, CNY – Chinese Renminbi, CLP – Chilean Peso, MXN – Mexican Peso, IDR – Indonesian Rupiah, RUB – Russian Ruble, ZAR – South African Rand, TRY – Turkish lira, KRW – South Korean Won, THB – Thai Baht, HUF – Hungarian Forint.

-

Cyclical vs. defensive sectors: Cyclical companies are companies whose profit and stock prices are highly correlated with economic fluctuations. Defensive stocks, on the contrary, are less correlated to economic cycles. MSCI GICS cyclical sectors are: consumer discretionary, financial, real estate, industrials, information technology and materials. Defensive sectors are: consumer staples, energy, healthcare, telecommunications services and utilities.

-

Duration: A measure of the sensitivity of the price (the value of principal) of a fixed income investment to a change in interest rates, expressed as a number of years.

-

High growth stocks: A high growth stock is anticipated to grow at a rate significantly above the average growth for the market.

-

Liquidity: The capacity to buy or sell assets quickly enough to prevent or minimise a loss.

-

P/E ratio: The price-to-earnings ratio (P/E ratio) is the ratio for valuing a company that measures its current share price relative to its per-share earnings (EPS).

-

QE: Quantitative easing (QE) is a type of monetary policy used by central banks to stimulate the economy by buying financial assets from commercial banks and other financial institutions.

-

QT: The opposite of QE, quantitative tightening (QT) is a contractionary monetary policy aimed to decrease the liquidity in the economy. It simply means that a CB reduces the pace of reinvestment of proceeds from maturing government bonds. It also means that the CB may increase interest rates as a tool to curb money supply.

-

Quality investing: This means to capture the performance of quality growth stocks by identifying stocks with: 1) A high return on equity (ROE); 2) Stable year-over-year earnings growth; and 3) Low financial leverage.

-

Quantitative tightening (QT): The opposite of QE, QT is a contractionary monetary policy aimed to decrease the liquidity in the economy. It simply means that a CB reduces the pace of reinvestment of proceeds from maturing government bonds. It also means that the CB may increase interest rates as a tool to curb money supply.

-

Rising star: A company that has a low credit rating, but only because it is new to the bond market and is therefore still establishing a track record. It does not yet have the track record and/or the size to earn an investment grade rating from a credit rating agency.

-

TIPS: A Treasury Inflation-Protected Security is a Treasury bond that is indexed to an inflationary gauge to protect investors from a decline in the purchasing power of their money.

-

Value style: This refers to purchasing stocks at relatively low prices, as indicated by low price-to-earnings, price-to-book and price-to-sales ratios, and high dividend yields. Sectors with a dominance of value style: energy, financials, telecom, utilities, real estate.

-

Volatility: A statistical measure of the dispersion of returns for a given security or market index. Usually, the higher the volatility, the riskier the security/market.