Summary

The fiscal lever returns in an uncertain global order

The ambiguity surrounding US tariffs and their implementation is raising fears among businesses and consumers that could weigh on economic growth over the medium to long term, while having a temporary effect on inflation. Combining this uncertainty with the high valuations in US stocks and the fiscal announcements outside the US, has resulted in the divergence in performances between the US, European and Chinese equities. The changing stance in Europe caused a repricing of yields. Looking ahead, in our view fiscal expansion and trade uncertainty will play out as follows:

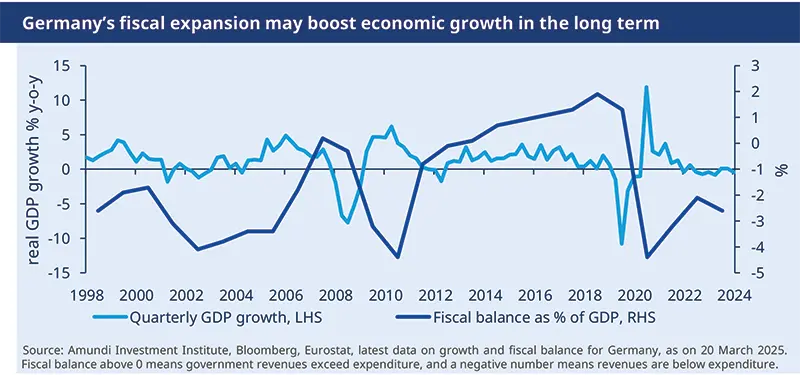

Revival of strategic autonomy in Europe. Trump’s manoeuvres are acting as a wake-up call for Europe. The German fiscal push and the EU defence initiatives could be game changers for the region’s growth, if properly targeted, but they will require time to deliver, and tariff risks also remain. The growth impact of these measures will come after 2025. For now, we are not changing our forecasts.

No recession in the US, but downside risks on the rise. The effect of tariffs on US growth adds concern, at a time of an already moderating economy. This is also evident from the Fed’s recent downgrade of the growth range for this year. We are monitoring how potentially slower growth could affect corporate earnings – the first half will be crucial.

Government stimulus in China, while short of an outright economic revival, has managed to sustain the positive sentiment. We upgrade our GDP growth forecasts from 4.1% to 4.4% (2025) and from 3.6% to 3.9% (2026) on the back of a strong fiscal multiplier.

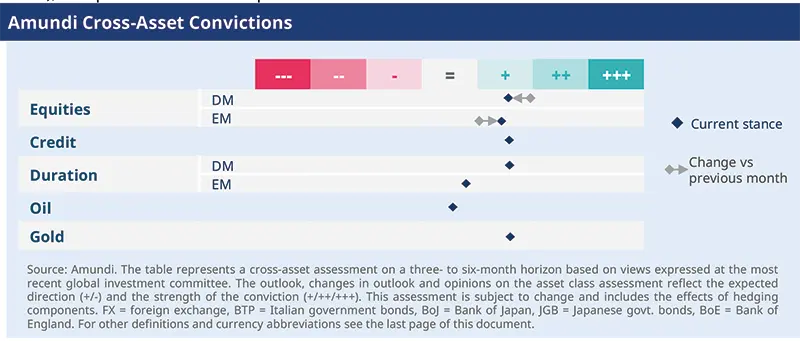

At a time when President Trump is willing to sacrifice short term US growth, Europe is signalling fiscal expansion. This doesn’t call for any risk reduction but rather a furthering of rotation outside of US large caps, and a renewed prioritisation towards areas of good valuations and earnings resilience in equities and credit. We outline our asset class views as follows:

Flexible and a global approach to duration in fixed income. The Fed’s mission on inflation control and the growth uncertainty emerging from tariffs have led to a debate on duration. We think if the Fed is forced to choose, it will likely tilt towards growth. We stay flexible on US Treasuries and prefer the intermediate parts of the curve in the US. In Europe and the UK, we are positive and believe Central Banks will continue cutting rates. Corporate credit is showing reasonable demand for high quality carry. We favour EU IG over HY, and financials over non financials, and in the US, our priority is towards segments where spreads are wide and compensate liquidity risk. We also like leveraged loans over HY.

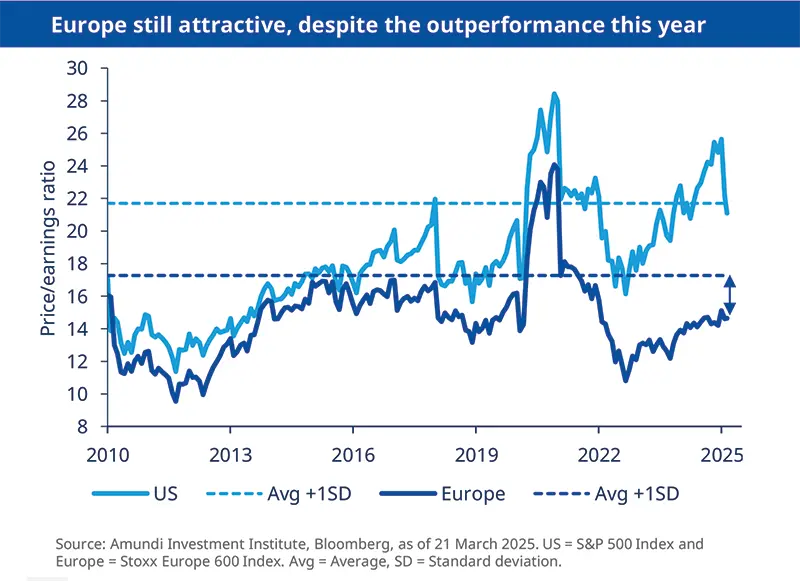

Play rotations and diversify equity exposure. The Trump effect and narrowing earnings gap between large caps and rest of the market have been a catalyst for the shift away from expensive US sectors. Our focus remains on quality, value and defensive. In industrials, we believe valuations are not very attractive, and there could be opportunities in areas that could benefit from a stimulus in Europe (Germany). For European outperformance to continue, earnings resilience will be crucial. Overall, we prioritise pricing power and balance sheet strength.

A weakening of US exceptionalism and robust growth in emerging markets keep us constructive. In hard currency bonds and the corporate sector, we like idiosyncratic stories that show potential for improvement in fundamentals and in equities, we have raised our stance on Emerging Europe.

Cross assets, play opportunities in Asia. We favour taking on good quality risk fixed income and equities and raised our stance on emerging markets stocks through China and India. While the Chinese economy should benefit from the policy boost, Indian valuations are better now, and it remains a long-term story of domestic consumption. We also slightly revised down our US duration stance. Finally, we believe gold and equity hedges are important to withstand volatility.

We maintain a well-diversified stance, with a positive view on European duration. We are also mildly pro-risk and do not see any signs of red flags with respect to liquidity events or potential credit risks.

Three hot questions

1| How do you see the evolution of the US economy amid the tariff backdrop?

We believe import tariffs in the US will be more negative for domestic consumption as they act as a tax on disposable incomes, rather than inflation. If US growth comes in weak in the first and second quarters, it could impact markets’ confidence for growth over the rest of the year. While we acknowledge that fears of a US recession are increasing in the markets, we do not see a recession materializing this year. Fiscal policy is reasonable, the Fed will continue cutting rates this year and oil prices are well-behaved, leading us to believe in a no recession environment.

Investment consequences :

Duration: close to neutral

Equities: cautious on growth and tech, positive on value

2| Do you think US trade policy will affect Fed’s decisions?

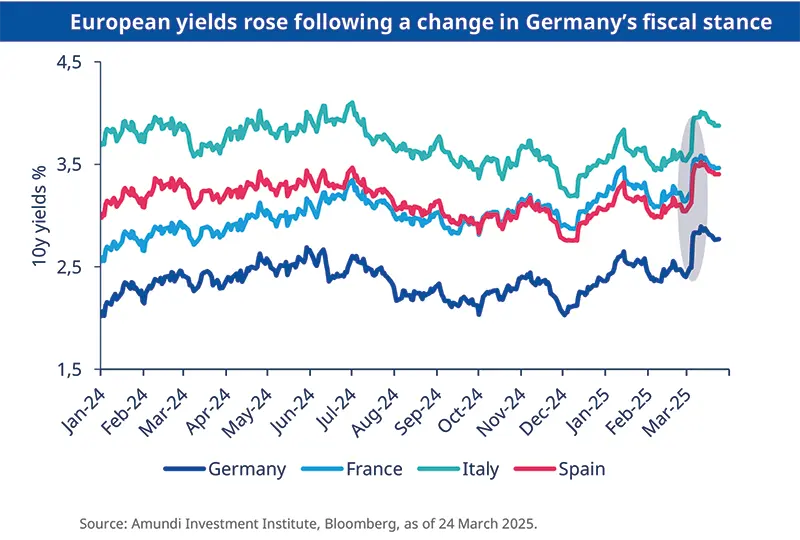

The uncertainty on President Trump’s trade policies has already affected market’s expectations of Fed rate cuts this year. While we maintain our view of three rate cuts by the Fed, we think if policy uncertainty remains high and it dampens economic growth, the Fed will be forced to respond with more easing. For now, the central bank sees the impact of tariffs as transitory and prefers to wait and see, keeping rates steady in its latest meeting. In Europe, expansionary fiscal policy will push bond yields up (narrowing the gap with the US), but we think the ECB still has room to continue on its rate cut path. The bank’s recent downgrade to EZ growth supports the case for continued easing.

Investment consequences :

- Fed: three rate cuts (25 bps each), taking the upper bound rate to 3.75% by year-end.

- ECB: three cuts, with the deposit rate reaching 1.75%.

3| What is the way forward for the USD and the EUR?

We have been saying for some time now that dollar strength is partly a result of exceptionalism in US growth and Fed interest rate policy. Unsurprisingly then, the dollar’s weakness this year has been caused by growth worries and uncertainties over Trump’s policies (something the market is not used to). At the same time, the changing fiscal stance in Europe pushed the euro up. As the region continues in this direction the currency will benefit. A convergence of growth between the US and other parts implies that US exceptionalism reflected in the USD will be challenged going forward.

Investment consequences :

- Our price target for the EUR/USD is 1.13 by year-end

US equities are seen as overvalued, with increasing concerns about the impact of tariffs on the economy. However, investors can find opportunities at the sector and stock levels within the US market and should consider diversifying into less expensive equity markets.

MULTI-ASSET

Recalibrate and make room for EM

| Francesco SANDRINI Head of Multi-Asset Strategies | John O'TOOLE Head of Multi-Asset Investment Solutions |

In a continuation of rally-broadening outside the US, we have raised our stance in emerging market equities and stay well-diversified overall.

Deteriorating economic data in the US, without a recession, indicates President Trump’s willingness to sacrifice short term US economic growth and that will keep the Fed on the look out for any signs of pain. This is happening at a time when China is showing clear signs of fiscal support and leaders in Europe are realising the need for fiscal push to become self-reliant and build defence and infrastructure capabilities. This doesn’t call for any risk reduction but instead a furthering of rotation outside US large caps, and a renewed focus on Europe and Asia. At the same time, we prefer keeping a diversified stance through bonds, gold to better cope with any market volatility, and maintain enough safeguards to reduce volatility.

On equities, in an overall active approach, we remain positive through EZ and the UK, which offers diversification within the broader European region. We are also constructive on the US, despite some expensive segments, with some protection to safeguard from short term volatility. In EM, we raised our stance on China’s domestic markets amid a more supportive government. We also turned slightly positive on India in light of attractive valuations (than last year), robust growth, which is relatively insulated from tariff concerns.

In bonds, we adjusted our US duration and curve-steepening stances, staying positive on the 5Y part but are no longer cautious on 30Y. A slowdown in quantitative tightening by the Fed, signs of containment of fiscal expenses and a weakening of growth could put downward pressure on yields. We are optimistic on duration in core Europe and the UK, and also on relative value stance towards Italian BTPs vs Bunds. In Asia, we are cautious on Japanese bonds. Credit remains attractive and in particular we maintain our tilt towards EU investment grade. In EM bonds, though, we are neutral.

Our FX views reflect a positive stance on USD/CHF and JPY/CHF but we are cautious on the trade weighted EUR vs. JPY and NOK on valuations concerns. We also believe investors should maintain adequate safeguards in the form of gold (geopolitics and potential inflation risks), and protections on US equities.

FIXED-INCOME

Sharp adjustments in yields call for agility on duration

| Amaury D'ORSAY Head of Fixed Income | Yerlan SYZDYKOV Global Head of Emerging Markets |

The growth optimism that was reflected in US bond yields when Trump’s election victory gained ground has now turned into a growth scare coming from the uncertainty on his tariff policies. In contrast, Germany’s fiscal push and a realisation across the EU that it should invest more have caused an upward shift in yields across large European economies. The main question remains how soon the benefits of this plan can percolate through to the real economy, and whether other European countries can afford higher yields. Long term, European growth will likely get a boost from more spending but near term implementation risks on fiscal spending remain. Hence, we maintain a flexible stance on duration, and explore quality segments in corporate credit.

- EU and German fiscal plans could be a game-changer in the long term and has caused an upward shift in Europe. EU duration is attractive, and we stay agile. UK duration is also appealing, but we are cautious on Japan due to high inflation which could affect the BoJ’s policy.

- Amid strong corporate fundamentals, we stay positive on corporate credit, especially on EU IG. We favour financials over non-financials.

- We have a neutral stance on EU HY and prefer subordinated debt.

- We are closely monitoring the Fed’s actions and believe it is worried more about growth than inflation. US Treasuries provide good diversification. We stay active on duration, with a preference for intermediate maturities (5-10y).

- We’ve raised our quality bias in corporate credit, and continue to favour IG over HY, and financials over industrials.

- Securitised credit offers good value, particularly agency MBS but we are active in light of current market fluctuations.

- Uncertainty around US trade policies and geopolitics, along with volatility on DM yields, keep us neutral and vigilant on EM duration.

- However, we are positive on hard currency debt where yields are attractive. Selection is key for us.

- In local currency, we like LatAm markets such as Brazil and Mexico. We are also evaluating the situation in Turkey and remain vigilant.

- On corporate credit, our positive stance is maintained but we keep an eye on valuations in the high yield segment.

EQUITIES

In global equity, stay well diversified

| Barry GLAVIN Head of Equity Platform | Yerlan SYZDYKOV Global Head of Emerging Markets |

President Trump’s policy gyrations are hurting market sentiment at a time when US valuations are still high. The uncertainty emanating from such policies make corporate investment decisions difficult and also cloud the earnings outlook. Hence, it is important to diversify away from the concentration risks in the US, and benefit from this rotation, with a focus on earnings resilience. For instance, in Europe and in China, while the rotation out of the US has been positive so far, the next leg of performance would depend on earnings. As a result, it is crucial to prioritise areas that show further potential for robust earnings (pricing power, supply chain strength, differentiated products) in the US, Europe and emerging markets.

- Fiscal stimulus in Germany and in the EU could potentially support corporate profits over the medium term. Even the fiscal boost in China may be good for some European companies.

- With this in mind, we stay balanced, and positive on defensives as well as cyclical industrial stocks.

- At a sector level, we are slightly more positive on consumer staples, discretionary and health care names. On the other hand, we turned more cautious on communication services and technology businesses.

- We see downside economic growth risks and believe corporate forward guidance will give more clarity on the impact of tariffs. We avoid expensive growth segments amid a narrowing earnings gap between large cap names and the rest of the market.

- On the other hand, we like value names, and businesses in the banking and materials sectors. Valuations in some tech names are becoming attractive (AI-related tech).

- In general, our focus is on quality and businesses that can reward through dividends and buybacks.

- Growth risks in the US and potentially weaker dollar along with robust growth in EM are positive factors for the asset class. However, US tariff uncertainty and geopolitics do not allow us to form large country views. We are close to neutral on China, with a tilt towards technology names.

- On India, we are constructive as the country is relatively insulated from the global trade uncertainty and is seeing a positive turnaround in corporate earnings.

- Regionally, we like emerging Europe and the UAE, with an overall selective approach.

VIEWS

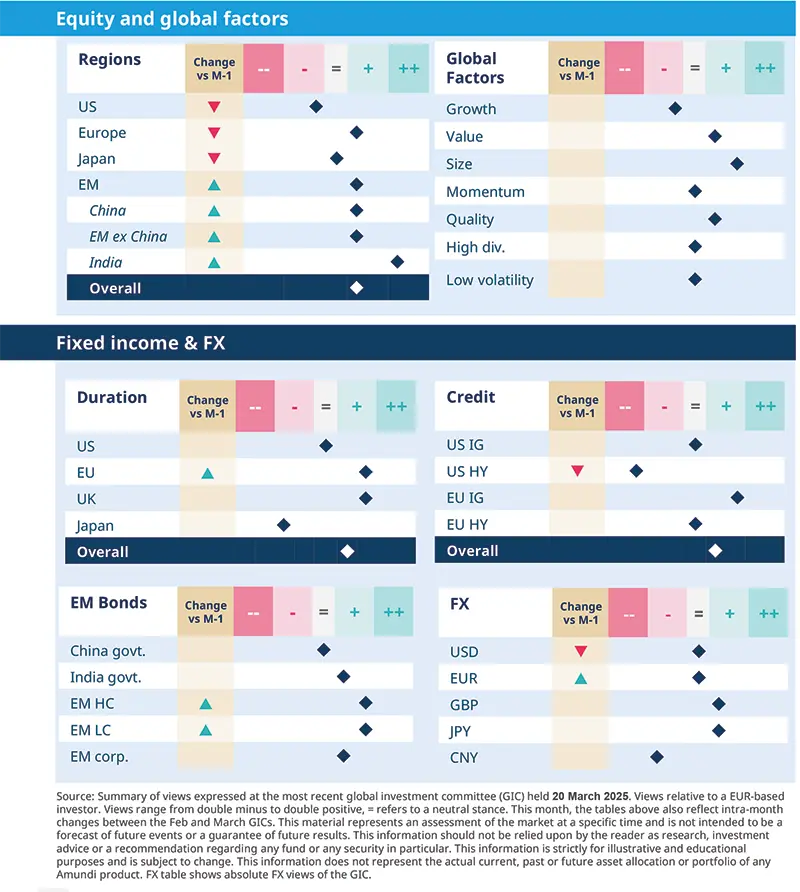

Amundi asset class views

Positive stance on equities: Our view on equities is slightly constructive, with an increasing tilt towards emerging markets. We see improving sentiment in China and better valuations in India as encouraging signs. In developed markets, we are optimistic on Europe and believe rising incomes, lower ECB rates, and strong household savings should support economic activity.

Definitions & Abbreviations

Currency abbreviations:

Currency abbreviations: USD – US dollar, BRL – Brazilian real, JPY – Japanese yen, GBP – British pound sterling, EUR – Euro, CAD – Canadian dollar, SEK – Swedish krona, NOK – Norwegian krone, CHF – Swiss Franc, NZD – New Zealand dollar, AUD – Australian dollar, CNY – Chinese Renminbi, CLP – Chilean Peso, MXN – Mexican Peso, IDR – Indonesian Rupiah, RUB – Russian Ruble, ZAR – South African Rand, TRY – Turkish lira, KRW – South Korean Won, THB – Thai Baht, HUF – Hungarian Forint, INR – Indian Rupee.

Authors