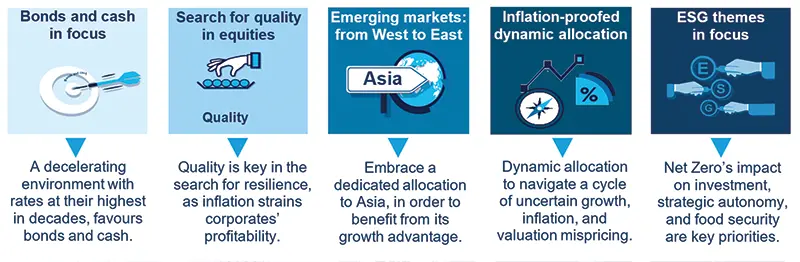

Opportunities lie beyond precarious path to growth

The lagged effects of monetary tightening on the real economy are changing global growth prospects, with divergences across regions. Emerging markets should remain more resilient in the second half of the year. The widening growth gap with developed markets is likely to generate opportunities for investors.